Should the US Buy from CXMT?

or is it exactly what America needs??

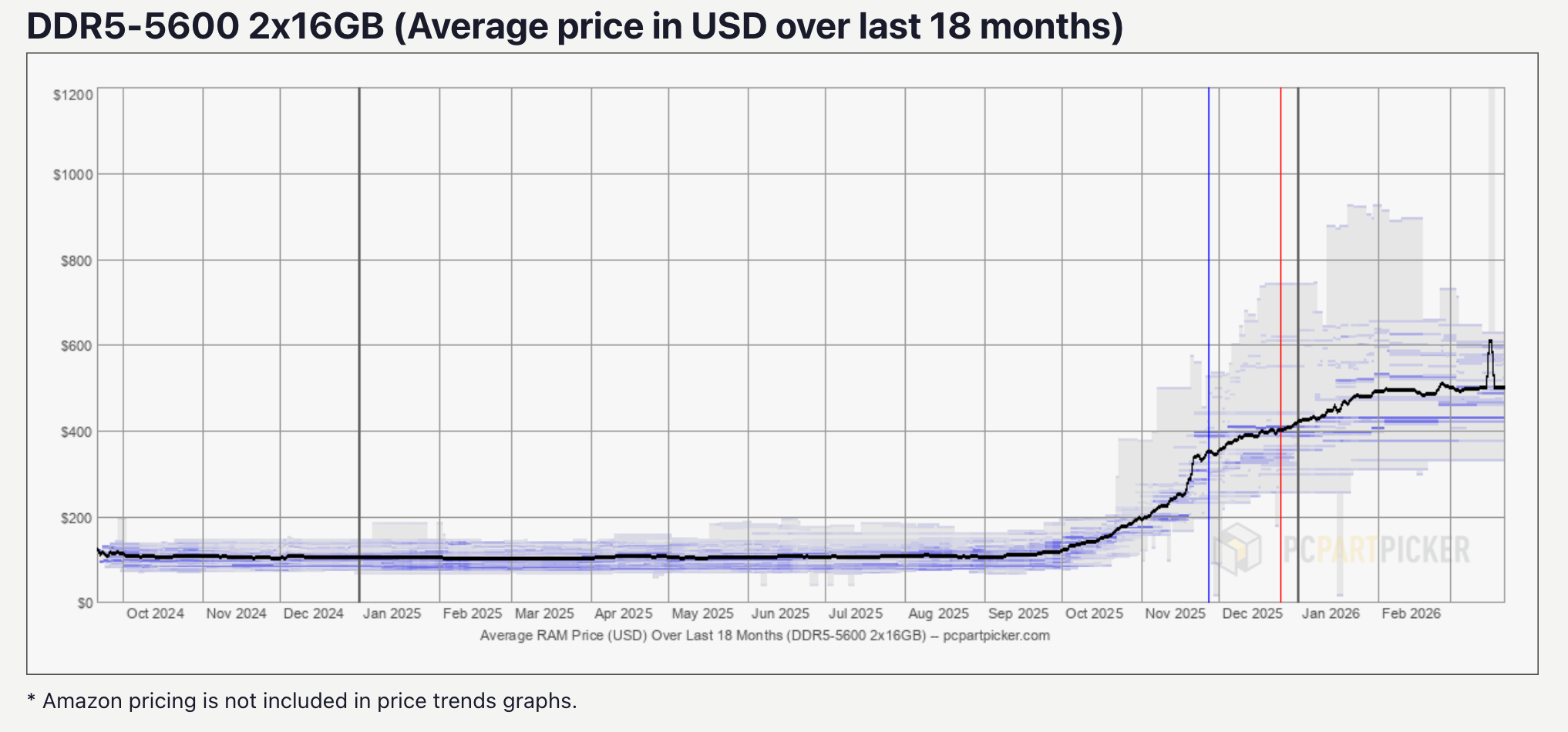

The “RAMageddon” is here. Tears roll down gamers’ cheeks as AI ruins DDR5 prices. People are even giving RAM as wedding presents. Why is memory going to the moon, and what are the geopolitical implications?

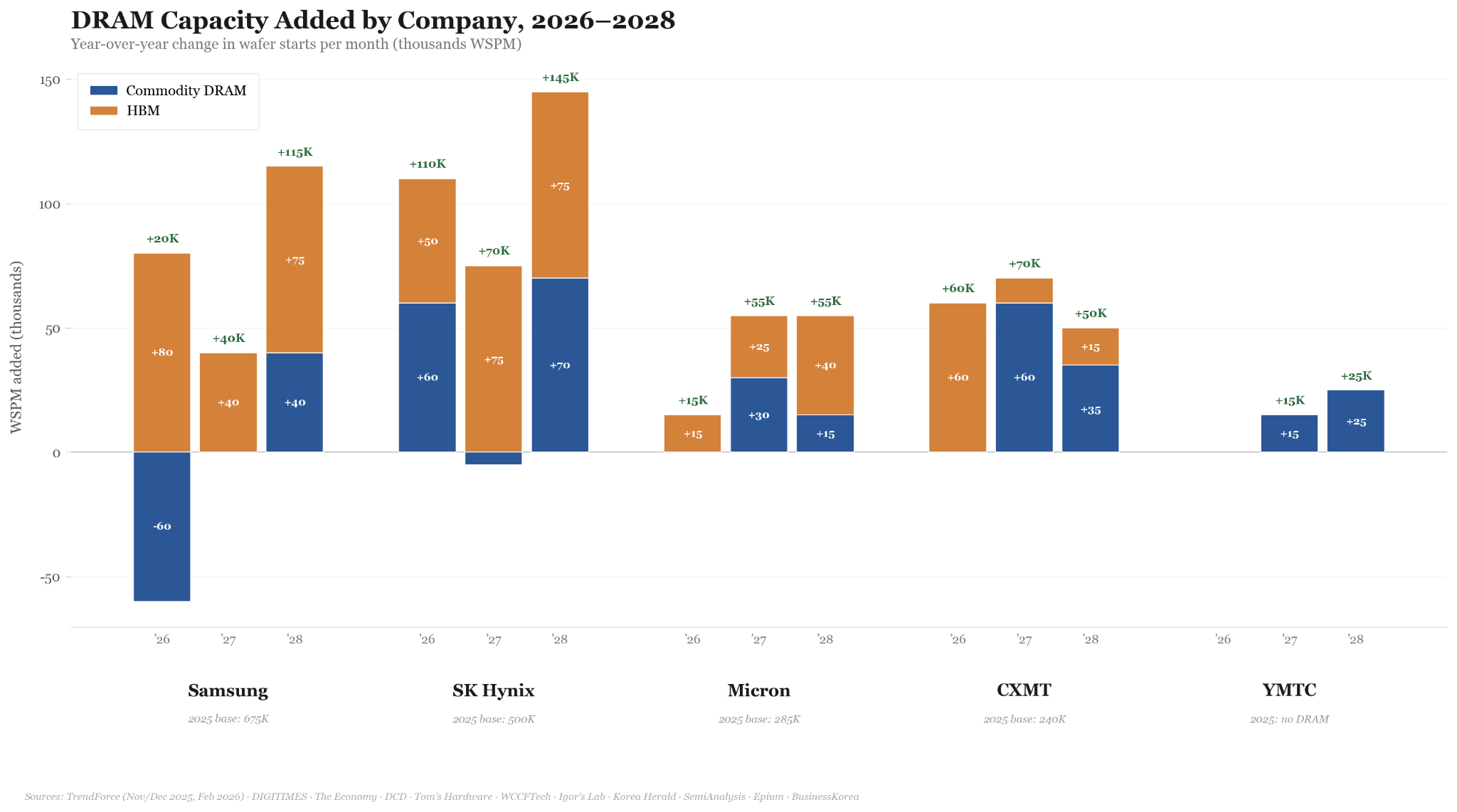

The Big Three memory makers — SK Hynix, Samsung, and Micron — have dedicated increasing capacity to memory for AI, or HBM. High-bandwidth memory (HBM) is a product that stacks multiple DRAM dies for AI memory. The increased allocation toward high-margin HBM means that not enough capacity is reserved for memory chips for consumer products. Thus, products like phones, laptops, gaming consoles, routers, tractors, and hospital equipment may experience price increases and shortages, perhaps as late as 2028. Adding memory capacity is a years-long operation, and in the meantime, the people will suffer.

As a result, there is murmuring amongst everyone, from the Pentagon to Apple and to individual gamers: perhaps the U.S. ought to turn to Chinese memory for consumer products. China’s leading DRAM company, CXMT, offers a compelling additional supply source. But the thought may scare conventional wisdom in D.C. Haven’t we been trying to decrease reliance on China? Why would we now open the floodgates on Chinese memory? In that case, perhaps the U.S. should instead ban or limit Chinese memory before the market creates unwanted dependencies.

Which is the right answer? Should Chinese memory be welcomed or restricted? This piece tries to answer the question by presenting both the case for and against Chinese memory. Ultimately, after balancing the impacts on the economy and national security, this piece believes that the U.S. should welcome Chinese memory — for products destined to the Chinese market. If customers can qualify CXMT for DRAM, then this would also lead to lower prices for American companies and consumers. The second-order benefits would be myriad, while the potential risks for market dependence and national security would be mitigated. Some risks, including assisting CXMT’s technological advances, are real but not sufficiently compelling.

The Case for Chinese Memory

Market Function

The most straightforward argument for allowing Chinese memory is to let the markets do what they will. Allowing Chinese DRAM from CXMT to compete with the Big Three will drive down prices for all. A naive calculation suggests that allowing CXMT unfettered access to American markets could increase global commodity DRAM supply by over 25%.1

However, the American markets will not be flooded with Chinese DRAM. First, CXMT’s capacity is already fully utilized by orders from Chinese customers like Xiaomi, Lenovo, and Alibaba Cloud. Although U.S. customers may be able to outbid other customers for limited capacity, this would likely be constrained in effect. Some Chinese customers have ongoing long-term contracts, and others would likely retain a preference for customer relations and governmental reasons. Thus, American customers would likely only be able to secure capacity for products destined for the Chinese market; for example, Apple is considering qualifying CXMT for iPhones only for Chinese consumers.

The real purpose of permitting CXMT is to offer bargaining power to customers in the immediate term. The advantage is not in securing orders, but in possessing the ability to secure orders. By qualifying CXMT DRAM, customers present a viable alternative and threat to the Big Three. The credibility of that threat is again uncertain, but it is likely credible enough for the Big Three to partially trim margins on commodity DRAM for customers.

The Big Three have moved away from fixed-price long-term agreements (LTAs) for DRAM and instead use post-settlement deals where suppliers can adjust the price after the orders have been delivered; this pricing structure benefits memory suppliers, but the inclusion of CXMT as a possible supplier could potentially promote a reversion to fixed-price LTAs or at least lessen the costs of post-settlement prices. This already seems to be the philosophy of leading PC makers and Apple. In this event, we would still be living through a shortage, but one that does not harm retail consumers as much.

The exact extent of price moderation in a world with CXMT memory is impossible to pin down — rough estimates must do. The extent would depend entirely on negotiated prices between customers and their memory suppliers, which would vary depending on the customer. The LTA Apple would get would be very different from the spot-price deal a small-time OEM would. Savings could also decrease if CXMT skyrockets DRAM price to align strategy with its market competitors, furthering the memory oligopoly. However, by adding more usable bits to the market, the price increases of memory in the coming months could decrease from anywhere from 5% to 15%.

Regardless of the exact number, these are real savings that pass on to the rest of the consumer economy. The RAM shortage is making the bill of materials for common products like smartphones and routers balloon, and allowing CXMT as a competitor will depressurize the market. Families needing laptops for school, offices needing PCs for workers, businesses needing cloud computing for operations — they all benefit in this world.

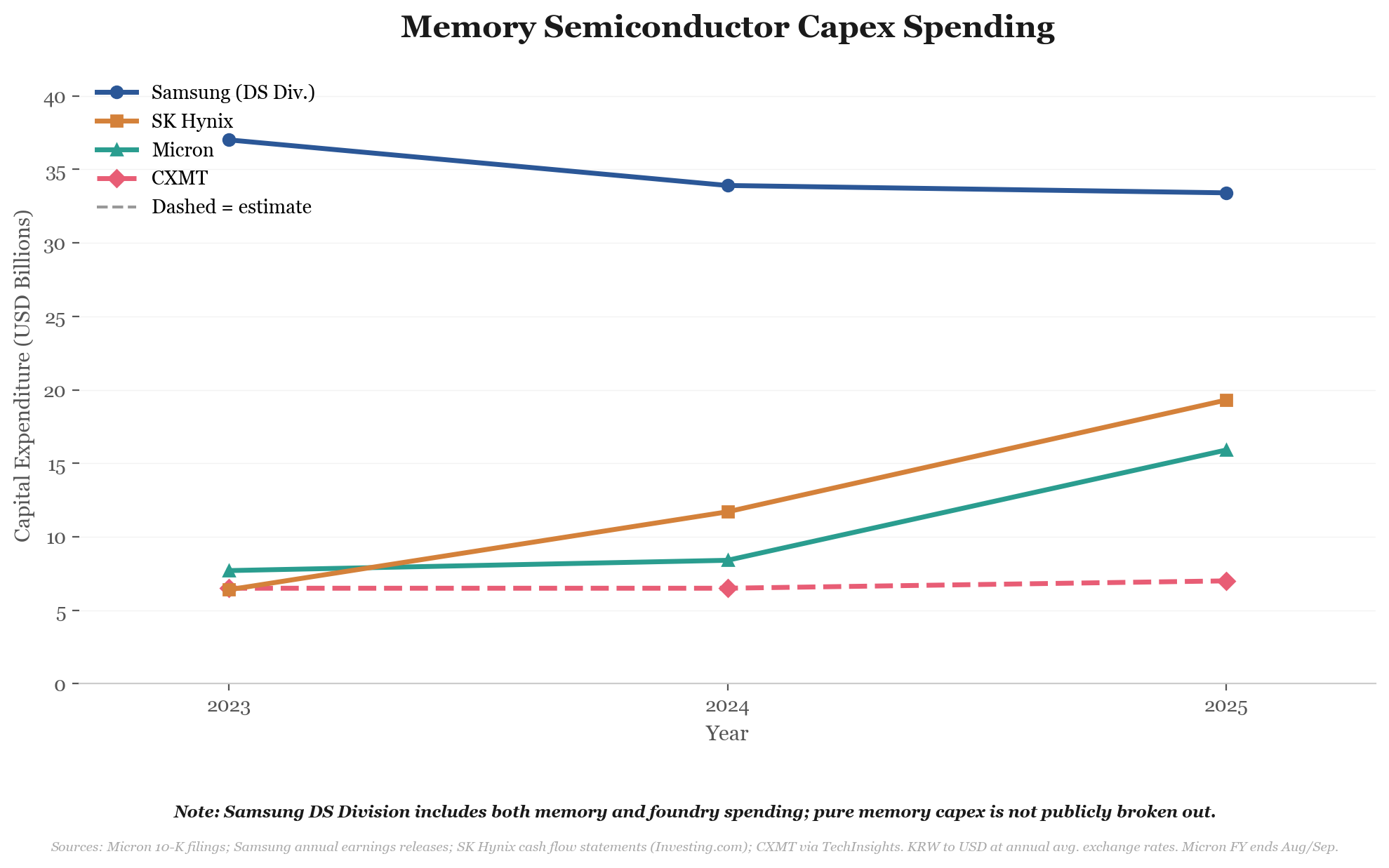

The persistence of the memory shortage also supports the need for alternatives outside of the Big Three (at least until H2 2027). Although everyone is currently spending heavily to expand capacity, fabs take years to come online. Further, as demonstrated below, the demand exceeds supply for HBM too. The capacity that the Big Three is building is for HBM, not for commodity DRAM. So while we wait for the Big Three to have the capacity and incentives to supply both HBM and commodity DRAM, CXMT can fill in the gap.

This situation is not hypothetical. Samsung’s planned memory expansions in its P4 fab and greenfield P5 fab are destined for HBM, not commodity DRAM, so such expansions will likely not alleviate the memory crunch. The story is similar for SK Hynix and Micron. Further, much of what “commodity” DRAM is manufactured by the Big Three may actually go toward AI applications, given server DDR5’s usage in the prefill phase for AI inference. By contrast, CXMT’s ramping production in its Shanghai megafab will be predominantly focused on commodity DRAM, not HBM or products for AI applications.

It is worth noting that the Big Three’s capacity allocation and expansion can play out in one of two ways: either they largely stick to their planned HBM roadmap, or they pivot to shift more allocation toward commodity DRAM. In the former situation, CXMT plays a helpful role moderating the market, pacifying the consumer economy until the Big Three have enough capacity in 2028. This scenario opens up greater risks of market dependency, which are explored in the case against Chinese memory below.

The latter scenario, while possible, is unlikely. Shifting allocation from HBM to commodity DRAM is not at all difficult; one just needs to swap out the masks in front-end fabrication, but all the equipment is the same. Shifting from normal DRAM to HBM is the more difficult transition, though, given HBM’s unique back-end processes. In this light, it makes sense that the Big Three’s expansions are all nominally targeted for HBM, as doing so gives them flexibility. However, shifting from HBM to commodity DRAM carries its own risks. By switching to commodity, fabs would effectively be losing money by underutilizing the tools that should have been used for HBM’s back-end processes. For semiconductor fabrication, where unit economics is king, downtime on tools is a cardinal sin.

However, some commodity DRAM products’ profit margins are superior to HBM3E, so perhaps more companies will dedicate more capacity as their HBM contracts are fulfilled. But anyone who says they know how the allocation will shake out is lying. Companies have some incentive to persist in HBM production even in the face of better commodity margins, as AI demand is more stable than the cyclical commodity market. Over the long-run, HBM yields better profit margins, even if DRAM booms cause the balance to shift temporarily. But perhaps a company will miss out on some HBM contracts or have process issues, making the allocation to commodity DRAM a better route. This is a dynamic process, involving variables ranging from the fate of the global economy, AI progress and developments, contract agreements, and individual business decisions. But if companies allocate more toward commodity DRAM than originally perceived, then the need for CXMT declines, circumventing potential concerns of market dependency.

After 2028, the crisis will likely have passed, and we can return to normal. At this point, the other fabs will have introduced enough capacity to render CXMT obsolete. Projects like SK Hynix’s Yongin megafab and Micron’s Boise and Tongluo fabs will be able to alleviate more of the demand. Further, commodity memory is notorious for being a glut-to-drought cyclical industry. By 2028, no one should be surprised if demand for commodity DRAM or even HBM dries up, causing a crash in prices instead of a continued surge. This is partially why memory makers are so reluctant to invest in commodity DRAM. (The emergence of LTAs and now so-called strategic customer agreements with five-year contracts is intended to lessen this risk, but we will see how much of an impact they have.)

Such cycles are dependent on consumer demand — a fickle variable tied to the global economy — and how important and memory-hungry AI will continue to be. The answer to the latter has been debated ad nauseam, and this piece largely follows Derek Thompson’s assessment of AI: nobody knows anything. Regardless, the odds are that by 2028, customers will not want to turn to CXMT for memory anymore.

Geopolitical Advantages

Another line of reasoning suggests that allowing Chinese memory into the American market may actually further our national security interests. By giving CXMT access to a lucrative market for their DRAM, they may be less incentivized to invest in HBM. After all, HBM would be a high-risk venture with certainly low yields (and thus, lower margins) in its early days.

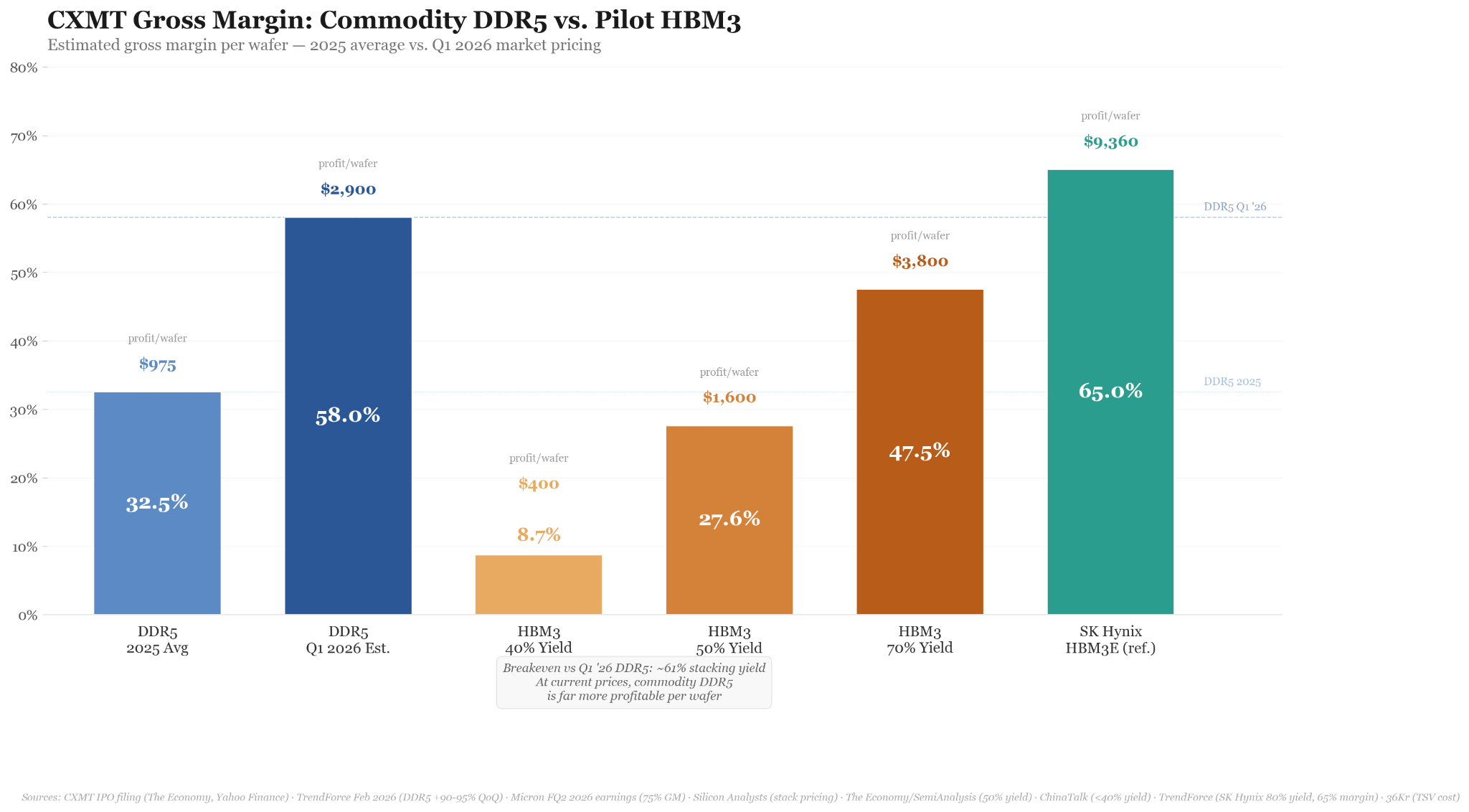

CXMT is expected to dedicate 20% of its increasing capacity to producing HBM3 this year, but perhaps it can be incentivized to move away from the AI market. Already, commodity DDR5 margins are exceeding profits from HBM3E among the Big Three. Considering that HBM3E is already achieving mature yields, imagine the incredible profit comparison for CXMT’s DDR5 versus a pilot HBM3 it has yet to start. Rough estimates indicate that a TSV yield of near 60% is the inflection point where HBM becomes more profitable than commodity DRAM, and a yield of upwards of 70% is required for the margin percentage to be better. However, given some estimates that CXMT won’t break 40% until the end of 2026, CXMT seems to be a far cry from reaching that inflection point.2

Given the importance of AI to Chinese customers and governmental actors, it is ludicrous to think that CXMT will give up HBM altogether; after all, the company may be able to realize a better profit on HBM over the long run if it increases yield and finds a way to keep progressing (an uncertain prospect). This is the same logic the Big Three are currently following. However, in the short run, bales of cash may induce CXMT to temporarily prefer commodity DRAM over its HBM ambitions. CXMT is not exactly like other Chinese chip companies (like Innoscience) that can run large deficits without care for revenue. Building DRAM and HBM is expensive on orders of magnitude greater than that of compound semiconductors or mature-node chips. Capital matters, and CXMT knows it. Thus, instead of a 20% allocation to HBM, CXMT could be tempted to lower that number to something like 15%. That would be a win.

It would be truly a difficult decision for CXMT to make. CXMT DRAM would be a competitive product internationally, allowing the company to grow more rapidly and have greater market penetration. HBM, while deemed a critical product, would have no global market; the rest of the world is already on HBM4E, whereas CXMT is stuck two generations behind. CXMT’s HBM would be for domestic markets only, and CXMT would have to perform a balancing act between domestic mandates and international growth.

This argument is not certain, however, and prompts objections that CXMT earning more in commodity DRAM can actually support their HBM ambitions; more cash translates to more resources for HBM development and process perfection. This argument is explored in the succeeding sections.

Splitting capacity between American and Chinese customers also causes negative externalities for other parts of China’s AI industry, such as SMIC and consumer-facing companies. Every chip going to an American customer is one not going to a Chinese customer. China’s leading chipmaker SMIC has already announced that its own orders are lagging; because customers don’t think they can secure enough memory chips for a finished product, they don’t bother ordering with SMIC for the logic chip. Further capacity allocated to American industry exacerbates this trend for the Chinese industry. If one believes that the U.S. buying CXMT DRAM supports their HBM ambitions, then by this logic, it would also hurt SMIC’s advanced node ambitions. With fewer orders, they would have fewer resources to develop past 5 nm.

Although a slowdown in the Chinese economy is not inherently an advantage for the U.S., the fewer dollars dedicated to SMIC’s advanced-node developments and Huawei’s AI processors are in America’s interest. Of course, it is again unclear how much capacity American customers would receive, and the Chinese government would certainly clamp down on attempts to leave Chinese companies empty-handed while American companies receive whatever they want. However, the allocation would likely be greater than zero, and the increased tension between the company and the government can only serve American interests.

The Case Against Chinese Memory

Market Dependency

The leading argument against allowing unfettered Chinese memory is predicated on real concerns of market dependency. The U.S. has taken pains to reduce its economic dependence on China for critical industries like rare earths, semiconductors, telecommunication infrastructure, etc. Why would we now allow that dependence to again fester in the form of memory chips?

Even if CXMT does not dominate the American market in the beginning, the company’s foothold in the American market has the potential to skyrocket. No one can serve demand right now, and everyone is attempting to expand capacity. As demonstrated in the previous sections, CXMT will be the first to significantly expand capacity for commodity DRAM. Could this not lead to a long-term, increasing dependence on CXMT? Although the immediate term may lead to helpful bargaining power without real allocation, the future may lead to real allocation that causes genuine entanglement.

It is possible that the Big Three become increasingly “HBM-first” companies, allowing CXMT (and later, YMTC) to take up a bigger share of the commodity market. The trends in wafer allocation could support this claim. The revenue that CXMT generates from this increased market share could be reinvested into R&D, capacity expansion, and even advancement in HBM.

However, it is highly unlikely that Chinese memory companies will play a role larger than end uses constrained to low-performance applications and/or in foreign markets. First, the Big Three will always make commodity DRAM. Large-scale production of DRAM dies helps the companies improve their yield for newer nodes, which are to be used later for HBM. The commodity DRAM is always the first step of the HBM process; they cannot be separated.

Second, customers will always want commodity DRAM from the Big Three, such that the economics will always tilt toward the Big Three maintaining some amount of commodity DRAM production. The Big Three’s DRAM nodes and performance are leagues ahead of CXMT’s. The Big Three are perfecting their 1c/1γ nodes while CXMT is still on 1y/1z, at least three generations behind. Even significantly cheaper CXMT DRAM is not so attractive given the use cases for memory in consumer products. Apple does not release a new generation iPhone with worse memory, even if it is much cheaper. The same goes for XBOXs and PCs; while some focus on the lower-cost market, the bifurcation of markets for low-cost and high-cost products can only serve consumer interest.

Betting on CXMT not to catch up or plateau is not a bet against Chinese innovation (a poor bet indeed), but rather a bet that export controls on EUV lithography and equipment required for DRAM advancements are effective. China’s domestic EUV capabilities will likely not be realized until 2030 at the earliest, and restrictions on EUV lithography have been an enduring American policy throughout both Republican and Democratic administrations. The $400 million machines are colossal and monopolized by ASML, meaning smuggling is not as serious an issue as it may be for individual chips.

Export controls condemn CXMT to only applications that do not require cutting-edge memory. That is an important market segment, but nothing near an impending monopoly or concerning supply chain risk. And even in these segments, other companies like Taiwan’s Winbond and Nanya will have room to compete and prevent a Chinese monopoly.

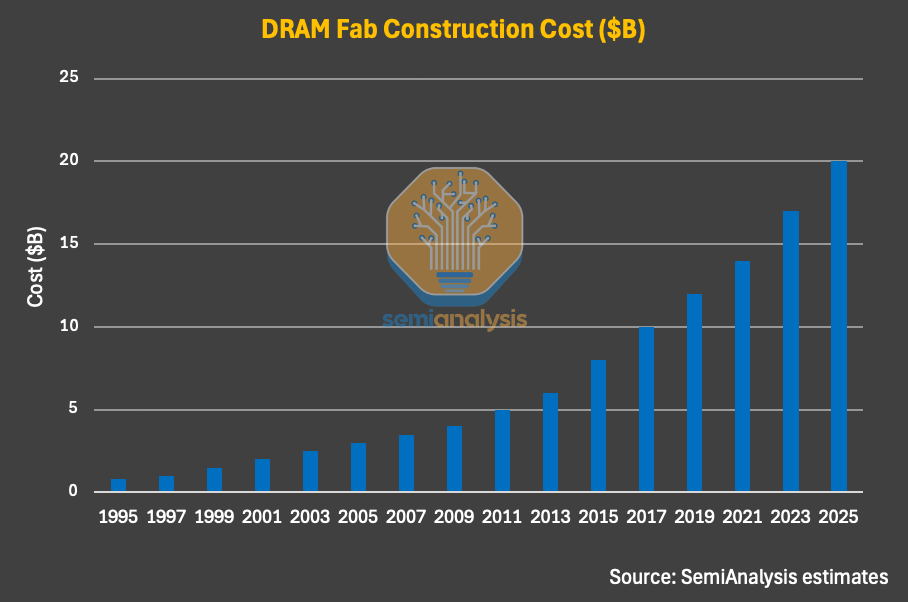

Lastly, this world would cause CXMT to constantly be tugged away from allocating more capacity toward HBM. Although revenue generated from the commodity segment may help CXMT build more and research better, they will be faced with tough decisions in wafer allocation. The market disincentivizes companies from building enough capacity to perfectly satisfy both commodity and HBM demand, as no one wants to be left holding the bag on a $20 billion fab once the cycle declines or if the AI bubble bursts.

Cautious expansion is the philosophy for everyone in the chipmaking space, for reasons well explained by Asianometry with respect to TSMC, the bullwhip effect, and the beer game. In brief, small variations in demand from retail consumers or AI players cause the greatest volatility for the suppliers at the end of the chain. If everyone in the world starts buying one more candy bar from the gas station, the gas stations feel it slightly, but the candy bar factory gets slammed the most with orders. If everyone starts buying one fewer candy bar, then the gas station barely feels it, but the candy bar factory can go broke. When the memory industry inevitably experiences a demand downturn — no matter how small — the memory makers will suffer the brunt of the fallout.3

Geopolitical Disadvantages

The stronger argument against Chinese memory is a geopolitical one. Every dollar going to CXMT and YMTC, regardless of how it benefits the American economy, would also be benefiting companies widely considered national security risks.

Although American policymakers have a tendency to think that Chinese companies have open checkbooks from the Chinese government, they need a great deal of supplemental funding to support their ambitions. CXMT’s recent IPO (and YMTC’s impending one) demonstrates the need for billions of dollars more capital to fund capacity expansions and R&D. American companies giving CXMT money for DRAM, thus, is America funding China’s HBM ambitions.

One of the Big Three’s biggest advantages currently is their ability to spend on capex in a way that CXMT cannot. These dollar amounts go toward node migration and capacity expansion — the reasons we’re ahead right now. Perhaps allowing CXMT to proliferate in the market will reverse this advantage.

Another concern is the reality that American customers would be helping to perfect CXMT’s processes by qualifying them as a supplier. For example, if Apple desires to qualify CXMT for its LPDDR5X in iPhones, then Apple will work with CXMT to make its processes more reliable and better performing. Apple engineers would literally assist CXMT’s products to outperform the JEDEC standard and meet rigorous requirements for metrics like thermal performance and consistency. Do we want American engineers helping Chinese companies in this way? It’s a hard pill to swallow. These technological advancements directly translate into CXMT building better HBM for AI demand.

And once qualified, ecosystem stickiness poses a problem. Even if the Big Three have capacity available once again, companies will have already gone through the trouble of qualifying CXMT as a supplier. Why not stick with them as a significant supplier, specifically for low-cost applications or in markets where price matters more than performance? How this plays out is again impossible to predict, but believing that CXMT will remain a major player beyond this memory crisis is a real possibility.

Aqib’s Verdict

Ultimately, the risks associated with permitting CXMT market access are grounded in more exaggerated doomsday scenarios rather than rigorous analysis. Giving CXMT money and qualifying it sounds scary, but the downsides seem to pale in comparison to the benefits. We shouldn’t care more about making sure China stays inside a box than the welfare of American citizens.

The fear of CXMT represents a prevailing American paranoia of anything associated with the five-star red flag. China is an adversary, but each decision should be predicated on rigorous cost-benefit analysis, not blanket anathema. Buying from CXMT will certainly help them in some way, with increased funding and a level of technological progress, but this is a far cry from China catching up or posing a threat.

First, CXMT’s progress will be more stymied by American export controls than benefited by customer revenue. Cracking future nodes of DRAM is more a technical problem than a financial one. Second, the technological benefits from being qualified by American customers should not be overstated. CXMT is already qualified by major players like Chinese smartphone, PC, and cloud computing companies. These companies already push CXMT to progress beyond industry-required minimums. An Apple partnership will perhaps move the needle a bit, but it is not like the U.S. would be helping them discover fire.

The ecosystem stickiness argument is the most defensible, but this piece does not weigh it as heavily compared to the myriad benefits. The Big Three produce better memory compared to CXMT on a performance basis, mainly due to the yield superiority gained from technological advancement and export controls. By 2028, just like 2026, CXMT will not be in the same league as the Big Three in terms of memory quality. Without advanced tooling, they cannot reach yields or performance specifications like the Big Three can.

The semiconductor industry is unlike electric vehicles or solar panels. Although China may offer cheaper products, the risk of market dependence is not so serious. Export controls and the difficult science of semiconductor manufacturing indicate that CXMT will be behind for years. The current market crunch is not a permanent state of affairs by any evaluation, but rather a temporary pain that requires a temporary solution. The players in the industry are also not engaged in a race to the bottom that China will win, but rather a race to the next node that China will lose.

The options are also not binary. The U.S. can permit CXMT now, when the benefits are attributed more toward bargaining power than to actual capacity allocation, and slam the door later. Other policy options to reap the benefits while managing the downsides exist, including greater tariff impositions, requirements on customer allocation ratios, etc.

Permitting now but slamming the door on Chinese memory later can also have added benefits. If CXMT expands capacity to satisfy American demand now, being shut out later would leave the company holding the debt of underutilized fabs and equipment. Of course, this is a severe oversimplification, and CXMT is not this dumb, but the regulatory uncertainty adds a layer of benefit.

Perhaps the best means of managing the benefits and downsides of permitting Chinese memory is allowing it in limited contexts. If the U.S. permits American companies to qualify CXMT solely for products destined for the Chinese market, then the scope of the “exposed” market is narrowed. For example, only iPhones for the Chinese market could contain Chinese memory, and the overall savings may be distributed throughout the market worldwide. However, this policy option, in my view, is worse than the aforementioned ones.

Banning CXMT is the least defensible policy position right now. The memory crunch is here, but it is not here to stay. Let’s allow the market to do what it will in the interests of our own people. Seeing ghosts in national security threats here discredits real national security threats elsewhere, so let informed policy reign, and let the DRAM flow.

Samsung’s DRAM capacity is between 650,000 to 700,000 wpm. SK Hynix’s is 500,000 wpm. Micron’s is between 340,000 to 500,000 wpm. CXMT’s is 300,000 wpm. After accounting for capacity allocated to HBM (about 40% for Big Three and 20% for CXMT), Big Three have an aggregate of 957,000 wpm for commodity DRAM whereas CXMT has 240,000 wpm. These numbers are estimates and intended to represent the capacity of CXMT compared to the Big Three.

This estimate of 40% should be taken with a grain of salt, as it results from the ever churning semiconductor rumor mill. The estimate also suggests CXMT will use MR-MUF for stacking, which while widely theorized, has not been confirmed.

This also suggests that one way to incentivize the Big Three to expand commodity capacity is via memory customer behavior. If memory customers like Apple form longer-term agreements with memory makers, agreeing to regularly purchase memory for X amount of years, memorymakers will be more incentivized to expand capacity. In this case, they know they won’t be left holding the bill if a drought occurs. This level of LTA is unprecedented in the memory industry, but longer term agreements are emerging. Further, this would result in memory customers holding unusual risk that may collapse firms in the event of a demand drought.

The agent-era framing shifts how to think about CXMT's market fit.

Frontier inference still needs HBM bandwidth from Micron/Samsung/SK Hynix. But yesterday's Kimi K2.6 release showed a different demand pattern: a 13-hour autonomous run using 300 parallel agents doing long-context work over hours. At that scale and duration, the relevant bottleneck shifts from peak HBM bandwidth to sustained memory throughput at reasonable cost per hour.

CXMT sits better for that tier-2 workload. Distillation, fine-tuning, longer-context batch inference, and multi-agent coordination don't need the same bandwidth as single-pass frontier inference. They need cost-effective gigabytes at acceptable latency.

The more interesting question may not be whether the US buys from CXMT but whether Chinese AI labs buy from CXMT. If 300-agent autonomous workflows become the norm, CXMT's domestic TAM could matter more than its export prospects.

More on K2.6's infrastructure implications in today's China AI Dispatch (chinaaidispatch.substack.com/p/300-agents-and-a-price-hike)

The question is less whether the US ‘should’ and more whether the memory cycle makes selective dependence economically irresistible before it becomes politically unacceptable.