The Robots Are Here

Why Unitree Matters

Robots are here, and they’re going to change the world, with Unitree currently in pole position. Joining me to discuss are Niko Ciminelli, longtime SemiAnalysis advisor, robot kid, venture investor, and Western New York native — go Bills! — along with Reyk Knuhtsen, robotics lead at SemiAnalysis. Lily Ottinger is co-hosting.

Our conversation covers:

Why robots are the real general-purpose technology because, for the first time in history, we can decouple capital from human labor.

How everyone keeps underestimating Unitree: the DJI and BYD playbooks, the danger of dismissing “robot dogs,” and why iteration speed matters more than dancing demos.

China’s edge: vertical integration, actuator manufacturing, and supply chains that make Chinese humanoids much cheaper than American ones.

Why you can’t AI your way out of a hardware problem or from a supply chain that makes your robot far more expensive to build.

What America should do next: allied supply chains, special economic zones, and industrial policy.

Why We Should Care About Robots Now

Jordan Schneider: Niko, let me start with you. Why should people care about robots now?

Niko Ciminelli: We’re in a world where everyone’s excited about digital AI — Claude Code, Codex, ChatGPT, etc. These tools are boosting productivity in white-collar cognitive work, but today they remain very much complements to people. Whether that stays true remains to be seen.

Robots are different. They’re a true general-purpose technology, the same way you’d think about AGI. For any subset of tasks where you can deploy a robot, you’re absolutely replacing someone you’d otherwise have needed. These jobs are usually fairly harsh, not well paid, and increasingly scarce in the West.

What’s interesting is that this is the first time in the physical world where a general-purpose robot — at the level of dexterity and capability we’ve written about — lets you fully decouple capital from labor in a profound way. Your production capacity becomes deeply tied to how many robots you can make. In a future where you want to spin up a small business or a manufacturing company, or where the US has a strong prerogative to make X, Y, and Z, robust robot capacity lets you do things you couldn’t previously imagine or resource. This is the first real general-purpose technology we’ve seen in the physical world in probably a hundred years, and that’s why it’s going to be as profound as digital AI in the limit.

Much of the data we want these magical AI returns from is scarce and physical-world oriented. If we want to build the Dyson sphere, build robots that build robots, build all these unique technologies, we need general-purpose robots. In pragmatic terms — to fix the labor shortage, to raise quality of life, and to do the things the West has veered away from — national-security-oriented, sure, but really the ability to improve citizens’ quality of life — that’s a very real possibility.

Jordan Schneider: Let’s level-set. It’s late June 2026 — how far are we from these things being genuinely economically productive? There’s this wondrous sci-fi vision, but you don’t get there until there’s a market for the crappy version: something just barely better than a human at some economically useful activity, enough that it’s worth scaling from making 1,000 to 10,000 to 100,000 units. Where would you put these humanoids today?

Niko Ciminelli: I’d take a slightly different perspective, because this gets really hard. Part of my motivation for helping SemiAnalysis cover this space is that we tend to view industrial automation through two lenses: bespoke technologies or sci-fi technologies.

Our first article was “Levels of Autonomy,” focused broadly on general-purpose robotics. In many ways, these systems have improved at a gradual rate that tracks progress in AI. A few things are different about robots: the data is harder to get, the unit economics differ, and the deployment constraints differ — how performant do you actually have to be before you can deploy in the real world?

This year isn’t one where we won’t see many deployments — we absolutely will, just for a very specific subset of tasks. You could argue that over the last year or two, pick-and-place saw enormous improvements, and we’re still watching those capabilities speed up and deploy across different parts of the world.

I caution people against framing this as a binary ChatGPT moment, because frankly I don’t believe in it. Certain results over the last six to nine months could be coined that way, but the label becomes uninteresting, because there have been multiple inflection points showing that certain approaches are scalable. Over the next two to three years, these will make a large swath of coarse manipulation tasks deployable at a scalable level. Within two to four years, we do see coarse manipulation with mobile manipulators becoming available to everybody.

Unitree and the DJI Playbook

Jordan Schneider: Let’s talk about the DJI analogy — going from making a drone that people actually wanted to buy, even though it couldn’t do everything you wanted, to being good enough to get the flywheel running, so that today we have this giant commercial drone ecosystem. Tell that story.

Reyk Knuhtsen: The DJI story is quite a tale to look back on when you examine what’s happening with Unitree right now.

People look at the drone market today and say DJI owns it — roughly 70% market share. Everyone you know who uses a drone probably uses a DJI; every filmmaker does. It seems ubiquitous now, and most people take it for granted without knowing how it got there.

Before the first Phantom, back around 2013, the consumer drone market basically didn’t exist. A competent drone cost around $20,000. Otherwise you’d buy the components and build one yourself for a couple thousand dollars, attach your own camera, and end up with something unstable, with poor flight time, that would crash. It was a mess and expensive all around.

Then DJI shipped a moderately better drone. It wasn’t exceptional — no 4K camera, still not very stable, flight time as short as ten minutes — but it was a fraction of the price, and that was enough to get people buying. It worked well enough to film something, to do things people couldn’t do before. That was enough to jump the company from about $4 million in revenue to roughly $130 million when the Phantom 1 came out in 2013. That’s the creation of the consumer drone market in real time. Suddenly there’s a whole market that didn’t exist before, one nobody had considered because it wasn’t on the table — and now it’s there for the taking. DJI took the money they made and kept scaling it into their drones: better stabilizers, longer flight times, better cameras, easier to use, cheaper as production scaled. Those economies of scale compounded, and now most people know what a DJI drone is and acknowledge it’s just the drone to buy. But there’s a huge, fascinating gap in how that came to be — the drone market was created out of thin air because DJI made something good enough that people would buy it and fund the market’s creation.

Lily Ottinger: Unitree’s IPO prospectus indicates that a growing section of their customer base is now commercial users — and it seems most of those are deploying the robot to dance in an entertainment setting. That’s not exactly what you’d imagine robots doing in the techno-optimist future. Is that going to be enough to set off this flywheel effect? Is this the birth of the consumer robotics market?

Niko Ciminelli: It’s unclear whether the current form factors are that. When Reyk and I looked back at how we so often get surprised by China’s manufacturing capacity, we found it comes in waves — not one complete unlock. Unitree’s revenue is very analogous in this regard.

Yes, this trajectory will continue, but it’s been heavily research-driven; they started in research. I wouldn’t call this the commercial moment where everyone buys something for their home for fun — these robots aren’t at the cost or quality level to make you feel safe doing that. But Unitree has the R1, which is about as cheap as a decent computer. That’s the mind-boggling part: it’s not actually a high-quality robot, but if you have decent spending power as an upper-middle-class white-collar worker, it’s within reach. That doesn’t mean one goes in everybody’s house — maybe they’re not there yet.

But first, it’s impressive they got there. Second, small businesses may use them for the things Reyk described. It becomes a bit of a meme, a small amount of usefulness, a novelty. This kind of thing captures the public eye.

Reyk Knuhtsen: To expand on Niko’s point, more and more people are going to buy them — for entertainment, for research, or, in the case of the very few, deploying them in industrial settings for actual job-based tasks.

The fact is they’re selling more, and they’re slowly eking into actual job-like settings. This can keep happening incrementally. The question, as Niko said, is whether this is the right form factor, whether we’ve found the right task, and whether the AI is there. But as long as this continues, the robot will get better, get cheaper, and become more accessible, which might improve it in other ways — making it more useful for specific tasks, unlocking new tasks, or fueling a research flywheel that makes the AI unlocks easier and the robots more competent generally.

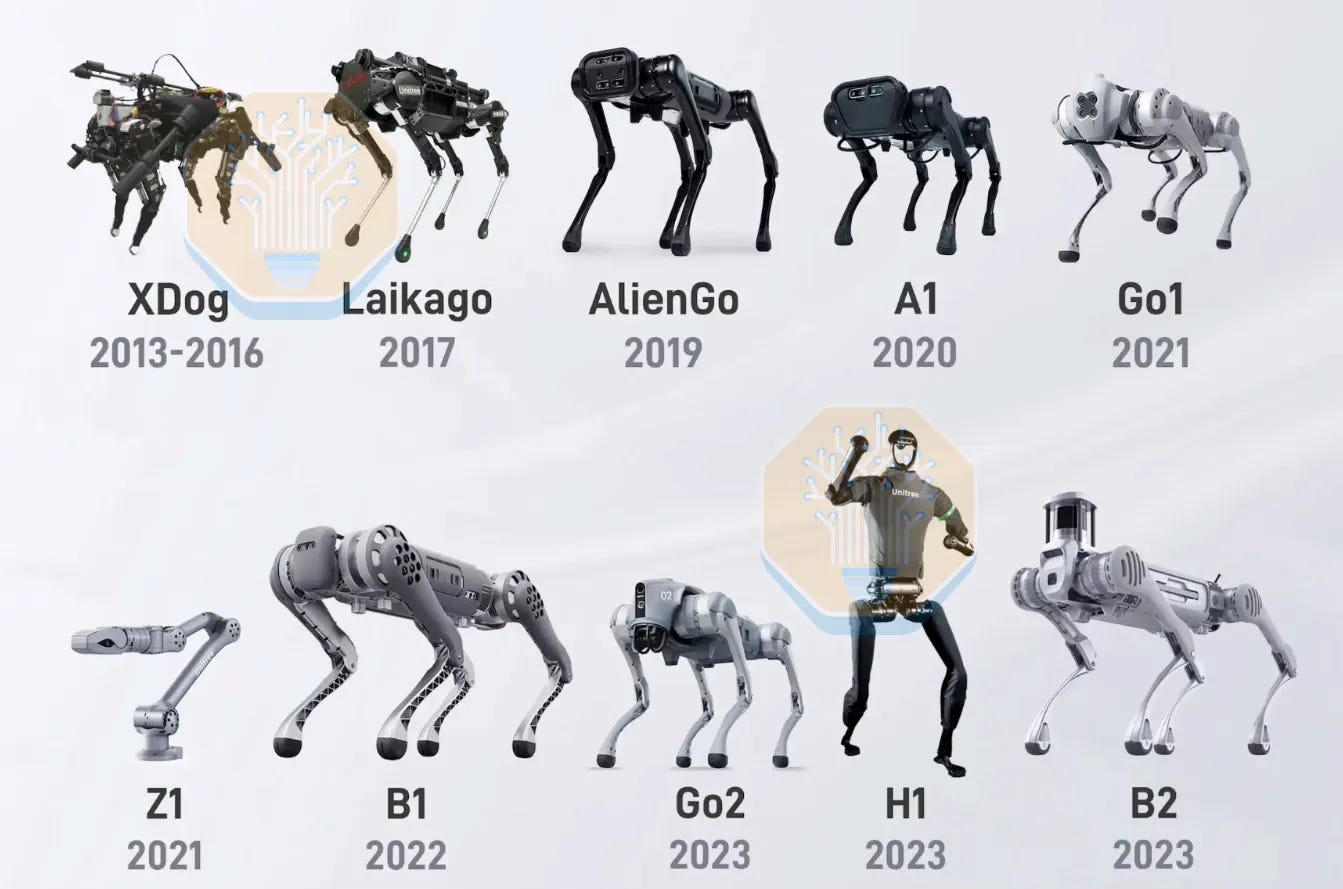

Niko Ciminelli: The core kernel of our last paper — not to harp on gradual change — is simply that Unitree was a quadruped company no more than a handful of years ago. People don’t tend to remember; our memories are short. So much is going on in the political economy, in AI, in everything, that people forget Unitree was just a robot-dog company. And I mean “just” the way it was used — almost pejoratively, as if that isn’t a market in itself.

In that rapid pace of progress, they reached something like the H2, a far more performant robot in payload capacity. They clearly have deeper ambitions — the cheaper consumer robot is within their sights, and they’ll also compete on robots that do economically valuable work. The G1 is an in-between robot I’d call a research robot; it’s used for entertainment, but we’ll see much better entertainment robots as they expand. The H2 is okay, but impressive that they got there so quickly — and there’s no reason to believe they’ll stop.

Some people point to their entertainment strategy a lot these days, but their iteration speed is what people should focus on.

Reyk Knuhtsen: The trajectory is what we were mainly trying to highlight. We don’t have to argue that the G1s are the ones you put in the factory right now, that they’ll be it, that they’ll do everything. No — these bots didn’t really matter before; they were research tools or toys. Now people are trying them out, taking them seriously, and trying to deploy them, and the pace at which that happened is remarkable. Then the H2 comes — a more performant bot. If this trajectory continues, it’s exciting.

How Much Better Are the Robots Now?

Jordan Schneider: Can you talk about the dimensions on which these robots have gotten, and will keep getting, better? How long they can run without a human fixing them up, how long they can hold something at ten pounds without overheating or tiring out — what do you need, besides more kung-fu moves, to start filling in for an actual human currently doing the job?

Reyk Knuhtsen: On overheating: look at the original G1s from a year or two ago, used in research tasks where they could carry a box of a couple kilograms for maybe five minutes at most.

Then it would overheat, and you’d have to let it sit in the corner for 30 minutes — sometimes a full hour — before doing another five minutes. They’ve clearly iterated on this. As we showed in our paper and heard from people, you can now get around five minutes of work with ten minutes of rest, even up to ten minutes of work with ten to fifteen minutes of rest. It varies by task, but it’s a vector they’ve clearly improved.

Other dimensions are interesting. Right now, admittedly — and we point this out in the paper — a lot of what we’re discussing is specific to one task: you pick up a box and move it from A to B. We’re not doing tactile manipulation, nothing that requires an understanding of force, like plugging something in. It’s just moving a box. In that regard, you could see battery life improving, stability improving, general controls improving so it functions better in the environment and is safer around people and objects. But moving beyond that task raises different questions depending on which task you look at.

Jordan Schneider: Let’s talk about hands. How do we get my data-center electrician?

Niko Ciminelli: The framing is that you have two main axes to improve. Hardware has to improve — cooling, more performant actuators, internal tracking, and, as Reyk mentioned, battery life. Those are specific to Unitree; every robot involves different design trade-offs. On the AI side, we’re not yet at the data scale to get very dexterous tasks unless you build more custom models.

On hands and data centers: for hands, we have companies like Wuji and Sharpa, and a few in the US — Tesla is doing interesting things. We’re making a lot of progress. But the important question is whether hands matter for the data-center electrician, and I’d argue no. A handful of startups, and quite a few non-startup projects, are increasingly interested in data centers. The cost of data centers is rising super-nonlinearly, especially as the buildout continues. You can make a custom end effector and a custom model that executes this well.

Also, you can’t teleoperate when the data center isn’t fully brought up. Even a gen-AI data center may be air-gapped — they often are — so you can’t always use teleoperation. We will get robots doing electrician work, at least cabling, as early as this year, deployed more materially over the next few years.

So we’ll have a very jagged frontier. Even though cabling is dexterous and has catastrophic failure modes, clever engineering — harnesses, safety backstops, extra code surrounding the model, the same way you’d approach gen AI — gets you a lot further than you’d think. Think of it like tool use in AI: a few clever application-layer companies are 3D-printing tools to surround a specific object — a spoon, or something a two-finger end effector can’t hold easily — which lets you jump the dexterity scale massively. That’s why these deployments will be jagged and gradual: there are many ways to get much further than the general model gives you naturally. In a bespoke domain, custom data and distribution data are really all that matters. That doesn’t mean the general models won’t come and unlock massive value, but robots will get deployed by many means over the next half-decade.

Jordan Schneider: Speaking of custom data — I just got served an ad offering to clean my house in New York City for free, because the cleaner wears a headband with a GoPro on it, and apparently that’s data. How is that economical?

Niko Ciminelli: I don’t know. These startups exist, and some have more interesting unit economics than others. But we’re all going to be collecting data and doing a lot of this pretty soon. This is the beginning, not the end.

Reyk Knuhtsen: We’re soon to be all data labelers. It’ll be a really good time when we have all the robots taking everything for us.

The BYD Warning

Jordan Schneider: Let’s come back to the Unitree arc and the BYD analogy. How are they running the playbook of internalizing more and more of their bill of materials, so they don’t rely as much on outside suppliers?

Niko Ciminelli: The most important thing to note is that BYD is a proof point. It was an underrated company in the West for a long time. We didn’t examine their quality at all. We use them because it’s a more intelligible example than what China has also done in cobots.

China’s arms were long considered low quality. BYD’s cars were considered low quality for a very long time. These things sneak up on you because of extreme economies of scale — and because you can close the loop tightly while still in R&D.

Right now, the vast majority of robots in China are still hand-assembled. They’re not at scale; this is still very high-mix manufacturing. One reason Unitree benefits so much from in-housing actuator production is that the designs aren’t set. That early decision — not to go to contract manufacturers until you have a high-volume, settled design — matters. They have used CMs before; I believe the G1 now uses one for specific parts.

If you don’t control every level of the stack, you don’t get the internal feedback loop or see all the tiny details. They go from rare-earth materials to a full robot at full pace, with suppliers down the street. That iteration loop is what let them improve so fast.

Typically, once you reach some revenue scale, the West demarcates you as one thing. They labeled Unitree a quadruped company; now they’re labeling it an entertainment-robot company. It’s a warning sign — we’ve seen this before. Look at BYD. We spent a decade saying China makes crappy cars. Now they’re extraordinarily cost-competitive at higher quality than many Western vehicles. They do this through extreme verticalization within a very dense external ecosystem. That’s the core kernel.

Jordan Schneider: Actuators — what are they, and why do they matter?

Reyk Knuhtsen: Simply put, the actuator is the part of the robot that generates motion. It’s easy to overlook as something simple, but you have to figure out how fast to move an arm, how to move it appropriately, how much torque to apply. If it hits something, should it stop? How does it stop — do you reverse everything at once? There are many configurations for designing an actuator, but the point is to generate motion accordingly.

Jordan Schneider: Why is everyone freaking out that we don’t make good ones in America?

Reyk Knuhtsen: The actuator generates motion, but it’s also the largest part of the robot’s bill of materials. We’ve done internal BOM costing for a number of humanoids — the G1 is the one we published — and the actuators run around 50 to 70% of the BOM. Without them, your robot doesn’t generate motion and doesn’t function.

If you source them externally, you pay all the extra costs on top: shipping, other people’s margins, some value-based pricing. So a robot built in the US — where manufacturing actuators is challenging — ends up structurally more expensive than one built on the same supply chain a Unitree or many Chinese robots use. You’re stuck. To compete on cost, you have to compete on the same actuator supply chain, which is extremely difficult. Our first paper covered this a lot — the many components involved, how hard they are to manufacture, and how they’re just not really made in the US.

Niko Ciminelli: We frankly don’t have the capacity to spin these up easily either; it just doesn’t exist. Many US companies do the winding of their actuators, but all the components come from outside — the aluminum, the magnets. Magnets are rare-earth-based, which isn’t always understood. We have some neodymium capacity, but we don’t process it; the processing goes back to China, and the chemicals for processing are in China. Some of these are multi-decade buildouts serving other industries, giving China a network effect. If we wanted to bring this home, an absurd amount of investment would have to happen today — or earlier — even to be a quarter of the way caught up in a decade.

And it’s not the only place this happens — Malaysia does some processing, Australia has some of these metals, the US produces some. But it’s a very complex, very sparse supply chain outside China, and China is really the only place that can do this at true scale today.

The Need for Production Capacity

Jordan Schneider: Sometimes I hear the argument: we have better software, our robots will be smarter, maybe we pay an extra 20% to build these, but they’ll have an OpenAI GPT-7 brain that your Unitree won’t. Niko’s shaking his head.

Niko Ciminelli: I just don’t know what that means. There’s a lot of obnoxious extrapolation in AI. Yes, progress is fast, but hardware systems integration is a different thing, and hardware production is a different thing.

The West said it didn’t need a manufacturing base — we’d just have good consultants and good banks and do services. That was extraordinarily naive. If you believe in AI progress and that you need production capacity, then deflating the cost of human cognitive labor makes production capacity more vital, because your ability to produce chips, cars, and everything else you need to extract value from intelligence lives in the manufacturing domain. You can discover a drug, but if you can’t manufacture it, you’re out of luck.

Second, what happens when China stops offering its supply chain at all? I don’t know why they would keep offering it. We’re not giving them chips under certain regimes and policies — I don’t know why they wouldn’t negotiate with robots. This is an enormously powerful technology in the limit.

On the AI argument — I don’t know why your robot needs Einstein-level intelligence if it’s 15x cheaper. That may sound like an overclaim, but look at the margins — Unitree can go quite low from where they are today and still make good money. China isn’t known for operating at these margins so early in a company’s life; they’re very willing to run at low margins. We’re not. That’s why people claim their humanoid will cost $100,000. Is that going to hold when Unitree ships a robot at around $30,000 with 80% of the capability? That doesn’t check out. And if they don’t want us to make robots, we can’t make robots.

Jordan Schneider: This is an interesting contrast with “oh, we’ll just ban all Chinese EVs and be fine.” America still gets cars. You don’t need BYD materials to drive around your country, because you already have these hundred-year ecosystems. You pay more, but you’re not leaving an entire vector of economic productivity on the table. If what you’re saying is true and this is an entirely new economic paradigm about to unlock, then you’re missing out on all of it — not just cars that are quieter and a little cheaper.

Niko Ciminelli: The thing constantly left out is memory. Everyone’s excited about the memory story, and it gets even crazier with robots. A lot more memory is going to go on these bots than in the past.

When you get a new AI capability, you find some absurd amount of demand — a shock to supply, a shock to demand; you can model it either way. That may not be fully true, but with a new capability comes extraordinary demand. In semiconductors, you at least had a mature supply chain — not an AI-mature one, but mature. The robot supply chain is extraordinarily nascent.

You might say: we have Nabtesco, we have Harmonic Drive — these things are made. But harmonic drives aren’t made the way quasi-direct-drive actuators are, which is the core thing we keep pointing out about Unitree. One reason people thought they were just a dog company is that they used an actuator considered non-performant. But then their iteration cycles — making it bigger, adding cooling mechanisms, generally better designs — made their robots more performant at lower cost. That’s really why they’ve done so well.

This gets scary because if you don’t invest early, you won’t have it later. We can’t easily catch up to some of China’s electronics ecosystems; for some things it’s simply not economically viable. The belief that we’ll “AI our way out of this” is enormously naive in a way that doesn’t apply the way it did before, like we have FSD — well, now China has FSD too. When are Chinese researchers not good at deep learning?

And we don’t have the industries to do data collection en masse the way they do. Many of our companies doing data collection do it in Southeast Asia, so I don’t always know where these arguments come from. I do think data quality is currently quite a bit lower in China — but again, these things improve rapidly over time. They’ll catch up.

Does America Have a Chance?

Lily Ottinger: Do you think America has a chance? What can be done? Jordan has said before that as soon as China does zero-to-one innovation at the cutting edge, the US will suddenly get really good at process espionage the way China has —

Niko Ciminelli:I love this.

Lily Ottinger: They’re selling these robots, so we can disassemble them and figure out what makes them good. If Unitree has to spend all this money on zero-to-one innovation, is that an edge for US companies that learn to be fast followers? What else can we do to give ourselves a fighting chance? And what happens if we don’t get it together?

Niko Ciminelli: It touches on the same point as last time –- we need to use our allies to build a supply chain, and we need to become much better hardware engineers. We have phenomenal AI research, and we’re very good at deployment, but this is a real gap.

Reyk Knuhtsen: Niko and I have a paper we hope to release soon on what it would actually take — how difficult the US supply chain really is. It’s quite difficult; there are a lot of holes. Look at PCBs: you don’t make copper foil in the US anymore. CNC machines are typically imported. A lot of ordinary industrial machinery nobody wanted to think about, we now can’t make without importing it or depending straight on Chinese product at some point.

Rebuilding this supply chain is far more daunting than most people realize. Say we do a teardown of the G1 and figure out exactly how to build it correctly — great, but who’s going to build it? Who am I going to pay? Most VCs won’t look at a CNC-shop company, because it won’t give them SaaS returns; it’s a hard bet. So you’re left with a strange pocket of businesses that aren’t sexy but are completely necessary, and few people want to fund them.

It’s fun to shout “US reindustrialization” — fun to talk about, fun to hope for, and I do hope it happens. But it’s far more complex than a motto. You’re probably going to need industrial policy to force it, because ordinary capital incentives won’t be enough.

Niko Ciminelli: It’s important to explain what Reyk and I mean by the supply chain. Yes, we don’t make tools in the US. You might say, doesn’t Germany, doesn’t Japan? We have Okuma and DMG Mori for CNCs, and other companies. Let’s pretend those are applicable, which I’d argue they often aren’t, for cost-structure and performance reasons we can get into. We aren’t even good at getting decent yield out of these machines.

We don’t have the tacit knowledge to run these at scale. Manufacturing tacit knowledge is a buzzword now, but it’s deeply true. Take materials processing: you need rare-earth magnets — neodymium, dysprosium, boron, and others. You need to process them, and you need the chemicals to do it. The machines involved are, like CNC machines, very complex, and we lack deep knowledge of making the details work. We talk about this with transformers in AI — the details matter; some layer norm blows up, and the infrastructure doesn’t work at scale for a given configuration. The same is true for these machines.

The hard part for us is the component supply chain. Everyone says we’re funding humanoids, funding robots, funding arms — but these arms and robots aren’t useful without an ecosystem. Venture capital is funding a lot of robotics; there’s enormous excitement. Some things can be vertically integrated — you can wind your actuators. The problem is the second-order companies. When people say “supply chain” and “we build our own actuators,” that’s often not fully true; they do it as best they can.

We likely need economic zones with special environmental policies, favorable tax treatment, and favorable permitting, where you can build quickly and run more experimental attempts. And we need to use Malaysia, Vietnam, Australia, and Japan for what they’re each good at, with trade agreements in place. The only way to do this is with the countries outside China who also worry about their industrial capacity and would bet on benefiting from US commercial strength. The only way up is through: dampen the pain and use other people’s strengths, because getting the tacit knowledge won’t be easy, and getting people to make serious infrastructure investment that isn’t there today won’t be easy either.

Jordan Schneider: The most proximate Washington debate right now is around imports. To what extent should whole Unitree robots, or their components, be allowed to flow into this ecosystem?

Reyk Knuhtsen: On the bots: banning Unitree imports will be challenging in a way people don’t realize. The main driver of US humanoid progress over the past couple of years has been access to Unitrees.

Before, you couldn’t really buy robots that were reasonably priced, reasonably accessible, and not entirely bespoke. Unitrees are fairly standardized — from one G1 to another. If it breaks, you get another at the same price. Back in 2024, you didn’t have many options; Unitree entering the market was a saving grace that created all this humanoid research. No other non-Chinese company has come in to supply these humanoids. There are a few US companies making open-source bots, which are nice, but those typically rely on Chinese parts too if you check the bill of materials. So if you ban these bots, you remove the researchers’ platform of choice and inevitably stall humanoid research.

Niko Ciminelli: Many American companies haven’t been hardware suppliers — the US unit economics and capital markets don’t favor it; it often doesn’t excite investors. Reyk’s point about the researcher’s first choice is definitively true. We’re not thrilled that’s the case, but I agree.

The bigger problem comes next. Yes, we may get our own humanoids soon — Optimus, Figure, Happy Droid, Apptronik, and others, with wildly variable quality and production capacity we won’t get into. But the supply chains and bills of materials are Chinese. We should be careful, because no one here has the cost structure yet. And what happens after a ban? They’ve already put an export control on neodymium, forcing us to buy their full actuator. If we ban their robots, we’re not in a high-leverage position for these negotiations.

You can ban a robot, but that doesn’t mean we can actually do anything. I’m not saying we should have Chinese robots potentially sending data back and handing China a massive advantage — but we need to be more thoughtful about our playbook. Are we doing this just because we think chips pressured them? We have TSMC for that; we have enormous supply chains outside China for chips. But cut off the component supply chain and we don’t have robots. They’ve already threatened this — CNC-machine exports to us are already dropping, and they’ve put export controls on the rare earths this requires. We might make some neodymium, but we can’t process it, and we have no dysprosium or boron — so where’s that coming from? They can cut us off in more places than we can pivot, especially this early. That would cut us off from our own progress. These are complex things to navigate. I don’t have clean answers, but we need to be very conscientious.

Jordan Schneider: On a less dour note — Niko, what are you most excited for these robots to do in the coming years?

Niko Ciminelli: I’m earnestly, wildly optimistic about them doing my laundry and cooking my food. The wondrous part of robotics is that we’ll see the deflation the AGI people promised, but in physical form. You could compress the cost of a lawyer, get affordable legal advice, get primary care — in the universe where that’s true. If a robot can do your yard work or your plumbing, all these severe “taxes” — where people just can’t afford good services — come down. We’ll see a wild quality-of-life increase from personal robots.

We’ll also see US manufacturers operate at healthy margins. With robot labor helping out, there will still be humans, but with robot labor alongside them. There’s a wild revitalization here — both quality of life and manufacturing capacity — where we can do things greener, cheaper, and at higher quality.

I have an investment in a construction-robotics company whose whole goal is that if you bring down the cost of construction, you can make beautiful buildings again — the aesthetics get reborn. These second-order effects of lowering the cost of physical-world labor will expand our capacity to do really amazing things. That’s genuinely exciting. That’s where my head is.

Reyk Knuhtsen: I’m on board with Niko — the cleaning robots will be very nice when that comes to play. Beyond that, I’m excited to see them enter the public sphere generally. It’ll bring more life to scenes with friends if a robot is helping around the house. It could help in an elder-care facility, making the bed or cleaning the kitchen. There are many areas where it could be very helpful.

The driving benefit is that it mitigates the manual-labor shortfall around the globe — from birth rates or whatever you want to point to. You free up, or enable, a lot more capacity for production or other benefits that weren’t available before, letting people do far more than they could.

But personally? It would just be pretty exciting to have a six-foot robot in my house. I think that’d be comical. I think that’s really, really funny.