Tooze and Klein on Chinese Growth Miracles, Hyperinflation, and Napoleonic Authoritarians

Plus! Wheelbarrows of cash, and how to push against a productivity undershoot

How much credit can the CCP claim post-1949 for the higher level of human development relative to the level of visible capital in China?

In the 175th ChinaTalk podcast episode published this morning, Adam Tooze and Matt Klein talked development economics and the growth of China’s economy in the 20th century. We go back to the oft-forgotten hyperinflation of the 1940s to why in the 80s the World Bank believed a little bit of policy tinkering would lead China’s economy to skyrocket.

The following is an abridged transcript of the conversation. For the full episode, do check out the podcast!

I enjoy putting ChinaTalk together. I hope you find it interesting and am delighted that it goes out free to seven thousand readers.

But, assembling all this material takes a lot of work, and I pay my contributors and editor. Right now, less than 1% of its readers support ChinaTalk financially.

If you appreciate the content and are interested in an ad-free feed of the podcast, please consider signing up for a paying subscription!

This conversation was transcribed by Raphael Wolf, with editing by Callan Quinn.

China in the 80s

Jordan Schneider: So Adam, I hear you've been listening to some old ChinaTalk episodes, and you mentioned that you had some issues with something that my boss (Dan Rosen) said a few episodes back.

Adam Tooze: Dan was giving an account of how the China narrative is run, and his basic schtick was, “The Communist Party had screwed everything up so badly by the early 1980s that all they had to do was stand back and let things run, because at that point Chinese GDP per capita was lower than Nicaragua.”

Obviously you can see the force of that point, but I happened to have been reading that day the first report on China done by the World Bank in 1983, which sets the stage for their incredibly harmonious relationship over the following decade.

So harmonious that it’s suspicious to some people, but nevertheless it’s a serious outside agency that comes in, spends some time trying to actually get a baseline on where China is starting from with its reform program.

And it’s absolutely fascinating reading, because this group of experienced World Bank economists take a look at China—a sustained and serious look at China—and conclude that it is in a vastly more favorable place than any other low-income developing country they had looked at up to that point.

The key metrics for them are human development: China had much higher levels of elementary education and basic public health provision (a middle-income-country level both), as well as literacy.

But they didn’t just look at these soft-tissue, human-development-index metrics. It was also the state of Chinese agriculture at that point, which on key metrics of agricultural modernization, like the deployment of artificial fertilizer, was again way ahead of any of its competitors.

The obvious comparison is of course with India, which is in a completely different league of underdevelopment on all of these metrics: decades less in terms of life expectancy, vastly higher infant mortality, much more primitive education system, about half the level of literacy of China.

So at that point, from the point of view of the World Bank, it seemed that the Communist regime—for all of the violence and the tens of millions of people whose lives they’d claimed—nevertheless laid the foundation for what looked like rapid growth.

Contrary to the argument that there was nothing there and the Communist regime needed to stand back, the argument of the World Bank was, this is a growth miracle waiting to happen. They need to tinker with policy here or there and then we expect over the next couple of decades China to leap forward to an unprecedented degree. That was their assessment in 1983.

Human Capital vs. Visible Capital, and Impediments to Both

Matt Klein: The reason I have a lot of sympathy for Dan’s point is that if you look at the level of Chinese GDP relative to the United States, it was unusually depressed.

It’s not because there were these human capital issues you might have seen in other poor countries, but because you have a 140-plus year period of more or less constant violence, either externally or internally. That led to significant underinvestment in visible capital.

Even if you had a lot of the fundamental social human capital elements that would have led to a successful society, there was never was a chance to deploy it because of underinvestment. From that perspective, and this is where I think Dan gets at something important, once that stops—you stop having imperialist invasion, you stop having Japanese invasion, you stop having a civil war, you stop having the upheaval of Mao—that's where things come into play.

Then the question is, to what extent was it thanks to the Communists after 1949 that you have the higher level of human development relative to the level of visible capital?

Or was it a whole long train of things that preceded that for hundreds of years? Probably a mix of both, but I think that’s where we can reconcile these stories and why a lot of the growth that we’ve seen since the late 1970s and early 1980s is thanks to decisions made by the Communist Party, including the turbocharge of fiscal investment. But a lot of that you would have expected—just the arrival of peace, domestically and internationally—to have a really big positive change.

Adam Tooze: A lot of Matt’s points seem entirely convincing, and clearly the end of violence, whether externally driven or internally driven through revolutionary upheaval, is a crucial precondition. But the story isn’t unique to China.

If you look across Eastern Europe, or the Soviet Union itself, one thing the state-socialist communist party regimes did in all of those places is transform societies with very low levels of human capital (even as late as 1950) into societies with much higher human capital. This is true for Bulgaria, Romania, the territory of the Soviet Union itself.

And it’s not even surprising, because it was their declared intention and they actually delivered on it. That’s just not true for countries like India, which may have had declarations like this at the time of independence but failed on those basic preconditions all the way down to the present day.

The argument is not of course that China doesn’t have that history of retardation that begins in the 18th and 19th century, or that the gap isn’t at its largest. I wholly agree—because of the sustained growth in the West, the gap numerically is going to be largest by the 1970s. This is true for the then–Third World in general.

But by 1983 there is this huge difference between China and other countries which in 1945 looked quite similar to China. That isn't accidental.

And the World Bank doesn't think it’s accidental. One shouldn't discount the modernizing ambition of the nationalist regime before 1945.

Education expenditure, China versus India [Source]

In a sense this goes rather well with a previous guest that Jordan had on, Scott Rozelle, the development economist from Stanford, who was making the very apt point that China now suffers from problems associated with those structures and investments that marked it as very different from your average, low-income developing country in the early 1980s; they in a sense continued on for decades, or in some cases actually deteriorated from their condition in the early 1980s.

I think there was a story there about healthcare and its deterioration through to the early 2000s that, now that it’s reached middle-income status, potentially jeopardizes China’s further growth.

So in a sense, it’s an issue of growth rate—at one point he says China just grew too fast. What I took that to mean is it outgrew the structures of education and healthcare, the basic human capital formation mechanisms that enabled that dramatic leap into low-scale manufacturing in the 1990s, 2000s, and 2010s.

Now the regime faces a huge challenge. The question is does it have the capacity to mobilize anymore? Can it actually reach down deep into Chinese society to create that base?

Because I thought his points were very powerful about that being the central question. If this is a supposedly long-lived authoritarian regime with a long time horizon, you’d expect them to be particularly good at investing in what we all know to be the high-payoff investments: early childhood education.

Everyone knows that’s where you get the biggest bang for your buck. They ought to be able to assimilate that logic. But for all the reasons he mentioned, that's actually quite difficult for China as well.

Jordan Schneider: And it's difficult for the United States also.

Adam Tooze: This is always the assumed contrast!

The really glaring failure is obviously a massively more affluent society, which critically underspends on early childhood education. There's no mystery as to why America is as unequal as it is—it's not even hiding, it’s just there in plain sight.

Matthew Klein: I think that despite the stereotypes that people have about authoritarian regimes having a long time horizon, I'm sure there’s also reason to be skeptical of how that plays out in practice.

In the Chinese case, the growth model that was so successful in the past forty years created a set of entrenched political and economic interests that benefit from the emphasis on investment in physical capital rather than human capital.

Those people then become an impediment to the transition that everyone—including the top leadership of the CCP—says they want to do. This was not a controversial point when Michael Pettis and I wrote it: it’s in the 2013 plenum that there should be more focus on raising living standards, improving healthcare quality, and things of that nature.

Yet it doesn't happen, which I think is a very interesting and revealing fact about how the actual political economy works, even if we don't necessarily see all the mechanisms that make it work, as you can in a place like the United States where it's more transparent. Clearly you look at the end results and that tells you something really important.

Adam Tooze: It’s really fascinating to learn about the decentralization of education spending and health spending in China. That's just a recipe for cumulative causation in this respect: “poor places stay poor because they can't raise the funds to invest.” That structural logic is operating very powerfully in the United States, and also clearly very powerfully in China.

The Great US Undershoot since 2006

Jordan Schneider: Matt, I hear you have some news.

Matt Klein: Yes! I recently launched a subscription newsletter called “The Overshoot.” It started about two weeks ago and I'm very excited about it.

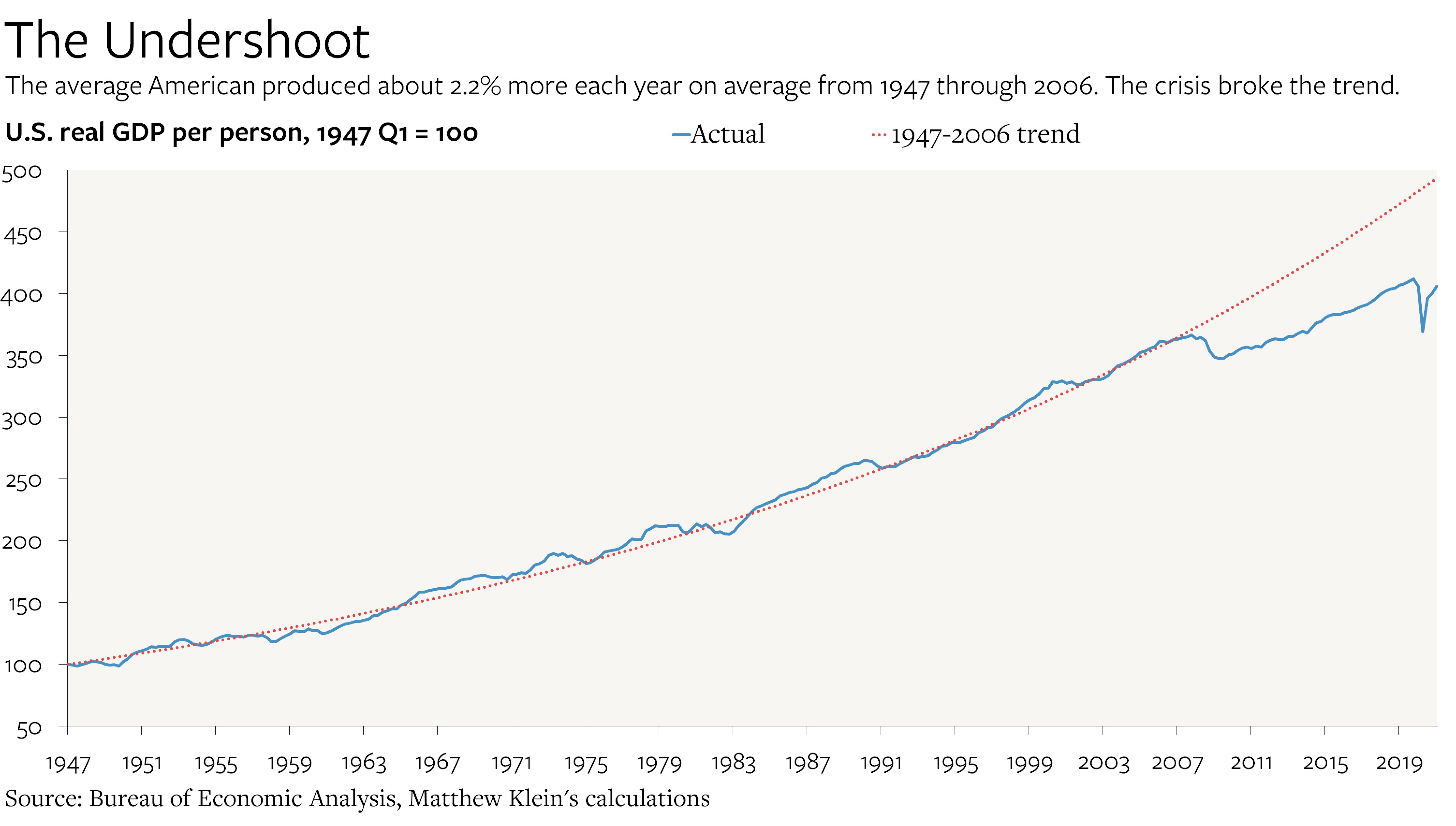

Adam Tooze: It’s ironic that it’s called “The Overshoot,” because your striking opening graph is actually all about the undershoot. You immediately got the nerd juices flowing. It shows American GDP per capita and the really shocking deviation from the post–World War II trend in growth of GDP per capita. It’s Substack with a mission!

America’s sluggish recovery from the crisis. [Source]

Matt Klein: The chart that I have in that first piece that Adam is describing shows how much the average American produced each year from 1947 until now. And what’s really striking is that from 1947 until 2006, you see this very steady increase of about 2.2 percent each year.

There’s of course variation around that, with business cycles, recessions, booms, and so forth. But it’s a remarkably stable trend until you get to 2006, when you have the financial crisis.

First, you see a pretty severe downturn, although not an unprecedented one.

What’s really striking is next you have this incredibly sluggish recovery, and that persisted all the way until the eve of the pandemic.

What ended up happening was that relative to this long-term, remarkably stable trend (stable in the face of a lot of different shifts in productivity and demographics and so forth) you have a 14 percent gap between where Americans would have been and where they actually were by the eve of the pandemic.

That is the big undershoot. It's a phenomenon we’ve seen globally—you see it in Europe, you see it for the world as a whole—but the oldest data we have for this is for the United States. I think it would be really nice to try to maybe not continue on this path. Maybe we can instead try not just to get back to the trend line, but see what happens if we go beyond it.

One of the things we’ve learned during the pandemic, including Adam’s work on mobilization economies, is that the limit of what an economy can produce is not some static fixed thing. There are hard limits in terms of the number of people and so forth, but there's a lot of flexibility—a lot depends on the ingenuity and adaptability on the part of businesses and workers, and we never get a chance to see what that is unless we really push that limit. That is where the name “The Overshoot” comes from.

How to Push Against the Undershoot? Aim High

Adam Tooze: It’s Verdoorn’s law, isn't it? This idea is that rates of productivity growth are causally related to rates of growth. So if you manage to grow faster and push the envelope, the dynamics will begin to go in the right direction.

People often quote economies like the Danish economy as models of this; whether or not you can extrapolate from a country the size of Denmark to big continental economies like the United States is open to question. I guess you could see that kind of logic operating at least in regional economies in the United States. High growth areas drive high productivity growth in a kind of virtuous circle.

Matt Klein: There’s the productivity and there's also the extent to which there’s so much extant capacity I think we didn't necessarily appreciate.

One of the things that I found really striking looking at the pandemic is that we've seen US consumer demand for durable goods up 40 percent in real terms since the start of the pandemic, which is remarkable.

There are stories of various supply bottlenecks and delivery slowdowns and some price increases, but on the whole, considering we’re talking about a 40 percent increase in the span of a year and a half, there’s been remarkably little disruption. That’s really striking. And it gives you a sense of how much other latent potential there is that we have yet to explore.

In the 1930s and 1940s, which I studied in my previous job and which of course Adam has worked on a lot, people were looking at how close to maximum the US economy was running on the eve of World War II.

That turned out to be a vast underestimate. The United States admittedly had an exceptional experience.

But still, it's very striking that when you get to the 1940s people thought they were about as recovered as they could be, and then you have economic output double in the years after that.

Maybe that was exceptional, but I think it's also really interesting to imagine to what extent have we not really tried to do that sort of thing. Let’s make the future different. It might not be necessarily perfect, but at least it’ll be different, and maybe there will be some real improvements we can have compared to the past fifteen years.

Adam Tooze: I was going to add the social justice dimension to this, which is really manifest in the American case. When we talk about the slack that we don't know exists, what we're actually talking about is the labor of those most precarious and most disadvantaged in the labor market.

Of course one of the really striking things about the US war economy and World War II was that it integrated women into the workforce at a really dramatic rate. That's where a lot of that extra capacity came from on the workforce side.

It also accelerated the migration of Black families out of the south into the new hubs of production in the north and in California. It changes the social structure as well, that pattern of accelerated growth.

What’s Limiting Large-Scale Rethink and Reinvestment?

Jordan Schneider: It’s kind of like the economy adheres to these bounds that you don’t even realize exist until you hit a crisis, and then you're like, “Oh wait, why are we doing this?”

You quoted Paul Krugman saying, “If we knew martians were going to be here in three years, we would have full employment in two weeks because there wouldn't be any qualms about freaking out about inflation.”

Adam, you’ve been making this argument in podcasts about how investment in science is the least painful way to go about potentially bending that productivity curve. But the fact is the size of investments—even when we're finally talking about it with the Endless-Frontier-turned-Competition-Act—really could be orders of magnitude higher.

It is striking to me that even in this post-Covid moment of being scared of China, we’re still not seeing the level of rethink which I think is necessary to do the kinds of investments that are going to fill that 15 percent Klein gap.

Adam Tooze: Absolutely. The ecomodernist side of my persona just doesn’t think we are gambling as heavily as we appear to be gambling on the science and technology necessary to provide us with the silver bullets to deal with the sorts of environmental anthropocentric challenges that lie ahead.

The comparable example from 2020 was these miraculous vaccine production programs. You'd think things would be happening differently if we were serious about climate. Further, I do take the failure of shutdown measures in general to be a pretty reliable sign of things to come with regard to climate. We desperately need these technical solutions.

It's also bipartisan, so you’d think if we’re serious about it we'd be spending ten times as much as we currently are.

I always come back to the pet food test: Americans spend $35 billion a year on pet food and treats. We don't come close to that kind of spending on adventurous energy research. That seems crazy.

Matt Klein: We’re talking about two related but slightly different things, which are the supply side of the economy and the demand side. These are clearly linked. As Adam was saying, the more you push demand the more you can expect to generate productivity increases in response.

A lot of what we saw in terms of why the US economy and the global economy underperformed is a demand-side phenomenon.

Sometimes people attribute it to productivity because this distinguishes the differences of inflation and inflation seems to always be 2 percent regardless. But I think it’s these two important things.

There’s a great line that’s attributed to George Eastman which is, “To spend money you have to spend money.” This is to say, if you want to really support a lot of demand, you need to make sure you invest in the capacity to produce the things so that you don’t have inflation.

I think that ties into what you guys are saying—that it's really important to have that research and that capital expenditure.

The Overlooked Hyperinflation Event: China in the 1940s

Jordan Schneider: Adam, between 1937 and the collapse of the nationalist regime in the spring of 1949, China experienced an inflationary surge that is among the worst ever recorded. Tell me more.

Adam Tooze: If you look at the list of great hyperinflations, one tends to think of Weimar, Zimbabwe, Venezuela. But if you're interested in hyperinflation intensity, the Chinese hyperinflation is among the worst ever, and it transpired basically as a result of the impact of the prolonged (and often in the West underrated) struggle between the Nationalist Regime in China and the Japanese, which destabilized the very, very fragile Chinese Republican state by 1945.

Then as the Nationalists tumbled forward after 1946 into the civil war with the Communists, things completely break down.

By 1948, you have Weimar-style scenes of people carting wheelbarrow loads of banknotes through the streets of Shanghai.

A girl in Shanghai holds up a $10 bill and its equivalent in Yuan (about 440,000), 1947. [Source]

If my memory serves it’s 123x10^12 ... so 123 trillion-fold inflation of the 1937 price level. I believe the Weimar one is 1 trillionfold. In any case, you could say at this point there's not much difference how far you're wiped out, you’re getting very close to zero in either case.

But it's extremely severe, and significantly absent from the historical imagination in the West. So reading Isabella Weber’s new book on the politics of price control in China in the 1980s, she refers to this example which piqued my interest.

I edited the Cambridge History of World War II with Michael Geyer a few years back, and we had a great contribution from a historian at Oxford called Gregg Huff that dealt with the broader monetary politics of World War II in Asia. He had alerted me to this problem as well.

One of the amazing things is that Life magazine sent Henri Cartier-Bresson to Shanghai in the fall of 1948. So we have these truly iconic images of hyperinflation shot by one of the greats. There are images of this in the MoMA. As an economic historian who loves art history, it's great to discover that link every once in a while.

Matt Klein: That episode is really interesting because it does fit into the broader theme of these hyperinflations as a consequence of broader social breakdown, often in the context of war or revolution. Losing a war in particular.

So it may not be part of the broader historical imagination, but along with the other less-well-known ones like Hungary in 1919 or North Korea in the 1990s, these are situations that don’t get much attention but do fit this common theme.

Adam Tooze: On the other hand, it also makes clear that talk about hyperinflation in any other context really is bonkers. We’ve got 99 problems, but that isn't one. The prospect of us suddenly sliding into a hyperinflationary situation is just completely unreal. It should be an acid test of somebody’s seriousness.

Fiat money is no doubt disconcerting, but the extraordinary thing about it is that almost all the time, except in situations of absolutely massive societal stress, we don't go anywhere near hyperinflation.

Matt Klein: There was some debate recently whether the term Fiat money is helpful or not, and I actually think this is a good example of how it is a good term. You think about what Fiat refers to, you’re talking about the law and the power of the state. This is exactly why, as long as you think that is basically holding, you can actually have pretty good confidence in your money.

On the other hand, if the power of the state breaks down then money breaks down too. People use it as a pejorative, but I actually find it pretty useful.

Adam Tooze: Try having money without it would be my recommendation! Money with no Fiat is pretty disconcerting too. I've often tried to issue Tooze coins to undergraduates and I've never found any takers.

Jordan Schneider: It’s because you were doing it before 2021!

Matt Klein: If you do it before you give them a grade, maybe that goes against some ethics things, but it would be a good demonstration of how it works.

Adam Tooze: Thank you, Matt. I’ll try this sadistic exercise on another occasion.

But more seriously, in the Chinese case as well it’s very fascinating to see how halting it is, right? This is true of the Weimar Republic as well. Milton Friedman might not be wrong that inflation is always and everywhere a monetary phenomenon, but it's also true that not all monetary phenomena are inflationary.

Even in a situation where you have a massively escalating monetary issuance by a highly stressed state, you don't necessarily get a smooth straight line of escalation in prices.

Early on in the inflation, you can make a bet the other way, right? If you actually trust in the government in the long run, you buy it cheap and sell it high. In fact, in the Weimar inflation as well as the Chinese one, there are moments where people are hoarding the currency in the expectation of a future stabilization.

This actually sustains the Nationalists in the first phase of the war against China, where there's a big patriotic rally and people will hold the Nationalist currency through to about 1939/40.

This is where we then get into conversations with the MMT crowd, because it gets interesting to know what are the shocks that destabilized that confident consensus.

Take something like a harvest failure, which is what happened during the Nationalist regime’s control in the 1940s. To a clean-minded macroeconomist, that can't be a driver of inflation, right? Because how could a single commodity’s price variation drive a general change in prices? If what it does is unleash a panic, it can very well have that effect.

That’s what we saw in 1940 in the Nationalist era: a harvest failure, a simultaneous effort of mobilization by the regime in preparation of an impending long war, and then the news of the terrifying Japanese advances over the winter of 1941/42. That’s where the inflation clearly begins to rise.

In the end, it's bonkers. The regime in 1948 is so desperate that they decide to introduce a new currency. Very Bitcoin-y. They only issue 200 million, gold-backed. And they just blow it two weeks later. They're issuing three times as much and it’s off to the races again.

In the meantime, they’d used the very terrifying secret police of the Nationalist regime in Shanghai to drum up about $170 million worth of hard currency in gold, because you’re going to back a currency like that with forced conversion of everyone's private gold and foreign currency holdings into the national reserve.

Henri Cartier-Bresson, exchanging silver on the black market, Beijing, December 1948. [Source]

Of course those people ended up just having been expropriated, because they handed over their private assets at the nominal exchange rate in August, and by November it's dead.

So that's the background to these Cartier-Bresson images of people who've just effectively been expropriated to the tune of $170 million, which is a lot of money at that point in Shanghai.

How Authoritarian Regimes Maintain Confidence in Fiat Systems

Matt Klein: That point about confidence reminds me of stuff that I've read about in the context of the US Civil War, where the value of Union greenbacks fluctuated depending on how people thought the war was going.

I’d be curious what was going on in Japan over the same period, because that probably would be an interesting story, though probably not a hyperinflation.

Adam Tooze: I don't actually know about the Japanese side of this, but on the German side you see exactly that kind of trajectory. During World War II the willingness to make bank deposits depends quite critically on people's assumptions about the future of the regime, unsurprisingly.

Certainly from the summer of 1944 onward, when you have this cataclysmic escalation of bad news, the silent financing mechanism begins to break down because more people are realizing the game is up, and they’re turning their cash into hard values and sticking whatever else under the pillow.

But even in the Chinese case, people on Twitter were really helpful in suggesting new lines of argument here.

We think of the early Nationalist folks as sort of like Chiang Kai-shek—feckless, corrupt. But that isn’t how the Nationalist regime understood itself at all.

It understood itself as a modernizing nationalist state-building regime. They were coming off a major effort to centralize the Chinese monetary system, which culminates in 1935 with not just the creation of a Central Bank, but the consolidation of a silver-backed currency issued by three banks: the Central Bank, the Bank of China, and the Communications Bank.

They actually celebrate the early phases of monetary financing as a testimony to the success of their modernization of the Chinese financial system. For them, that move into an elastic Fiat money regime was a sign of how modern they were, not a sign of a slippery slope to disaster.

Matt Klein: They just had the misfortune of then being invaded.

Adam Tooze: The misfortune of losing rather badly to the Japanese for a long time. I was struck by how modest, in financial terms, the scale of American aid was.

I guess they figured that the National regime couldn’t actually use more than they provided. But compared to what they're pumping into the British war effort, it's trivial, it's peanuts.

Matt Klein: It's an interesting counterfactual to consider what would have happened if the United States had treated the Nationalists the way they treated the British and the Soviets, because presumably that would have affected the civil war outcome.

Jordan Schneider: I’m sure there was a racial component to it.

Adam Tooze: Maybe, but also I don't think the Nationalists fail in the civil war for lack of supplies. The stories I remember are of the peasant Communist Army surrounding the amply equipped armored divisions of the Nationalists, fighting them at close quarters.

I don't think it's a lack of material that makes difference there. That's where I think the inflation story is a key part. The significance of all of this is that in the mindset of the Communist Party ruling class, one of the reasons they think they prevailed is that, as Lenin said, the best way to destroy a bourgeois society is to unleash inflation. (This is apocryphally attributed to Lenin by Keynes.)

In any case, the Chinese Communist Party understands this. Perhaps surprisingly to Western eyes, they think of themselves as a force for monetary stabilization. This is true actually of the Bolsheviks as well, who introduced the gold standard after the chaos of the civil war in the Soviet Union.

That of course has a very enduring significance for the politics and the political economy of the regime through the crises of the late 1980s and then all the way down to the present.

I think a lot of this conversation was triggered by the fact that you see the People’s Bank of China and other spokespeople in China right now positioning themselves as the sort of conservative antidote to quantitative easing, against the corrupt, degenerate financial systems of the West.

There was that weird moment last year when yields-chasing bondholders in the West were piling into Chinese sovereign debt because it seemed to offer a great combination of steady positive yields.

Matt Klein: As you're alluding to, one of the things that I found really striking in the book that I wrote with Michael Pettis, one of the things that was happening in the late 1980s in China was that you had these changes in relative prices because of the liberalization of the countryside relative to the city.

That led to 20–30 percent inflation for urban residents. That was pretty dramatic and destabilizing. That I think definitely contributed to both the political unrest and then the violence of the crackdown that followed, because they were afraid of that destabilization.

As you said, it's interesting how the recognition that inflation is destabilizing does carry over to other authoritarian regimes.

I’m sure other people have written about this, but I remember reading in Kotkin’s biography of Stalin that there was a debate in the 1920s about economic policy: There was basically an MMT side, which was arguing we should create money and keep full employment. And there was another hard money side, saying we have to maintain a balance of payments and maintain the gold reserves and balanced budgets.

Stalin sided with this second group. It’s interesting how that plays out. It doesn’t really fit with the narratives we have in the West about economic policy and ideology.

Adam Tooze: Even Napoleon, right? Maybe Napoleon is the archetype for this kind of post-revolutionary stabilizing authoritarianism. He also introduced a stable franc, which basically saw the French bourgeoisie through the 19th century.

That's where the rentier ideology in France is anchored—in the hyperinflation of the revolutionary period, which was one of the first revolutionary experiments with paper money as part of a political program at mobilization. One of Bonaparte’s promises is monetary stabilization in the aftermath.

There’s a fascinating trade-off between, on the one hand, the triumphalist democratic narrative—the Glorious Revolution, the stabilization of currency and financial systems around the representation of bondholders in parliament—which is a very powerful narrative that drives a lot of economic and political thinking from the late seventeenth century all the way down to Niall Ferguson and others in the present.

And on the other hand, the authoritarian version: an authoritarian decision maker with a long time horizon is a better guarantor of monetary and financial stability. You have that playing out very markedly in the 1920s and 1930s. It's quite fascinating.

Matt Klein: The Fiat conversation kind of comes back again, because if you have a really legitimate state that actually voluntarily commands the respect of the people, you can get away with a lot more. And if you don't then you have to pick one of those extremes.

Adam Tooze: Coming back to the Nationalist regime in China, after the Northern expedition in 1928/29 when they’re establishing their grips and setting up the Central Bank, the acid test is can they borrow domestically in their own currency, because that's the bit of borrowing that’s most vulnerable to devaluation.

The answer was they could, and quite successfully. At least until 1932 when they carried out the first bond reorganization, and then in 1935 or 1936 they did another one and that rather unsurprisingly destroyed their credit, so during the war they were never able to launch a significant bond. That is a benchmark of where you stand.

Matt Klein: And between 1920 and 1932 they lose all of Manchuria in two wars, which is pretty significant.

Adam Tooze: But nevertheless, through that first phase there’s still a wave of enthusiasm. That’s an interesting feature of finance in China’s history generally. The politics of debt exists not just at the peak level, but in a broader sense throughout the political class.

Evidently, this class is a tiny fraction of China's immense population (most of whom are illiterate or peasants who don't have access to this), but within the political class in the cities there’s significant support.

This is true of many of the emerging market economies of 1900: Iran, Ottoman Empire, Russia to a certain extent, Egypt.

Debt reorganization is one of the key instruments of imperial rule from the outside, and whether or not you can organize a powerful and rich domestic bond market is critical to sovereignty as understood from the top, but also nationalist commitment from the bottom.

People will subscribe to this stuff out of patriotism so as to free the governments from the constraints of external debts. That’s a very interesting factor. It’s very significant that by 1940, essentially, the Nationalists had expired all of their goodwill. No one in China in their right mind would lend to them anymore.