Yes, Transformers Are a Problem...

But so are converters, inverters, and MMCs!

Dana Golden is an economist at Argonne National Labs.

The views and opinions expressed in this article are solely those of the author in her personal capacity and do not represent, reflect, or imply the official positions, policies, or viewpoints of her employer, Argonne National Laboratory. This article was completed and submitted in April 2026, prior to the author’s employment with Argonne, and any analysis, conclusions, or statements contained herein were developed independently and outside the scope of her current role.

I want to offer you a thought experiment. A genie has agreed to conjure an infinite supply of transformers for integration into US power systems. We’ve heard plenty about the transformer shortage. They’re vital to data centers, construction projects, and grid expansion. With one rub of the lamp, that bottleneck vanishes. Do our power supply chain problems disappear? Can we build all the data centers we want?

Let’s go further. The genie also supplies limitless gas turbines. If you’ve been following the data center energy discourse, this feels like a double whammy — the two big bottlenecks, gone. Throw in a third wish for streamlined permitting. Is the grid supply chain fixed? Can we build out data centers like railroads in 1872?

The answer is clearly no.

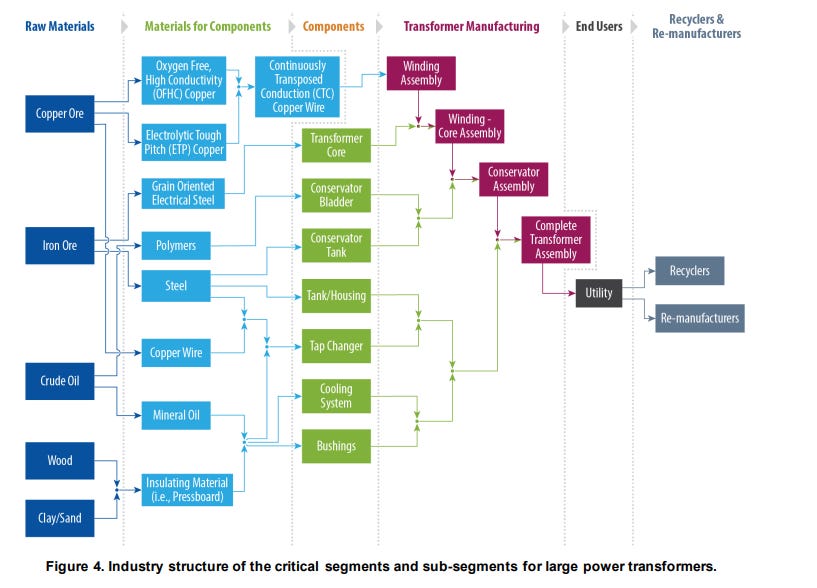

Grid supply chain problems go far deeper than transformers and gas turbines. Grid modernization requires many other components with equal or greater supply chain challenges. The DOE’s supply chain mapping for large power transformers alone reveals many inputs with significant interdependencies throughout the power electronics supply chain. If these inputs threaten transformer supply chains, they equally create headaches for the supply chains of other important power electronics.

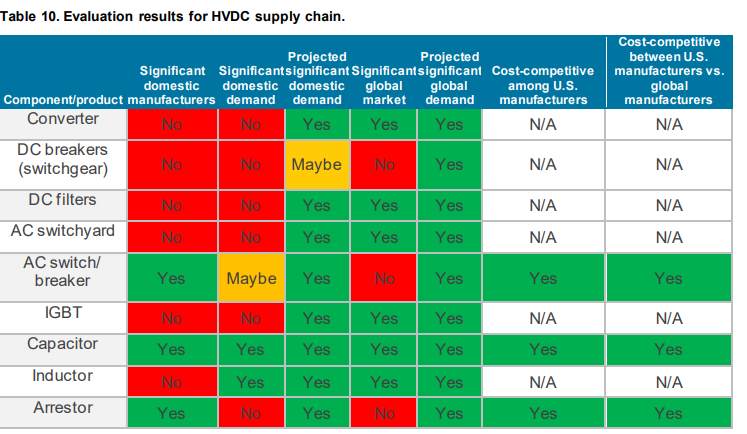

Go further into the DOE’s work, and you find that the HVDC supply chain lacks significant domestic manufacturing capacity throughout, with components like converters (circuits that help change between voltage levels) and DC filters (devices to suppress electromagnetic interference) not even generating enough domestic demand to encourage new capacity entry.

The economic security community spent years learning the semiconductor supply chain map for compute. We all read Chip War and learned of ASML’s EUV monopoly, TSMC’s fabrication dominance, the handful of firms producing photoresists and etch gases… Not nearly the same attention has been paid to power electronics. It’s time for that to change.

Separating the Gallium from the Copper

I have another thought experiment for you. It’s 2027, and China has carrier groups in the South China Sea headed for Taiwan. The current US administration has chosen to escalate. Maybe the escalation looks like sanctions. Maybe this is a full-scale military fight. Either way, the Shanghai Metals Exchange is closed for business to the West. Suddenly, analysts get on TV shouting about our dependence on Beijing for rare earth elements and — of course — critical minerals! So critical. Important minerals.

Talking heads from MSNBC to Fox cannot agree on whether we should be defending the ROC against the PRC, but everyone seems to agree that we are effectively up shit’s creek without a paddle. We have brought a shovel to a drill fight and cannot wage war without the ability to purchase critical minerals. Suddenly, prices from copper to lithium to ytterbium shoot to the moon. Weeks later, prices for almost all metals have come back down. We discover that only a small subset of metals could not be procured in the medium run without trade with the Middle Kingdom. Turns out our vulnerabilities in this space are almost entirely restricted to a few elements — some notable rare earths, and importantly, gallium.

In our 2027 scenario, the majority of the metals crisis was fixed almost immediately. What could have happened? Simple. The President got the heads of Trafigura (Singapore-based multinational commodities trading and logistics company), Vitol (Dutch energy and commodity trading company), and Glencore (Anglo-Swiss Metals and Mining Trading Company) in a room at the White House and dropped a curtain to reveal a gigantic pile of cash to go to ‘the beautiful America-loving firm that can win in getting me metals.’ Suddenly, ships magically stop in place and move towards the US coasts. Boats bound from the port of Shenzhen suddenly fall off ship-tracking systems, reappear under Dutch banners and, as though pulled out of a hat by an illusionist, find their way to Los Angeles. Resolution Copper gets built, and with economic incentives, fracking-bros decide to apply their chemistry expertise to mining in Mountain Pass. Turns out, it was never all that hard to procure most critical minerals. We lacked an economic incentive.

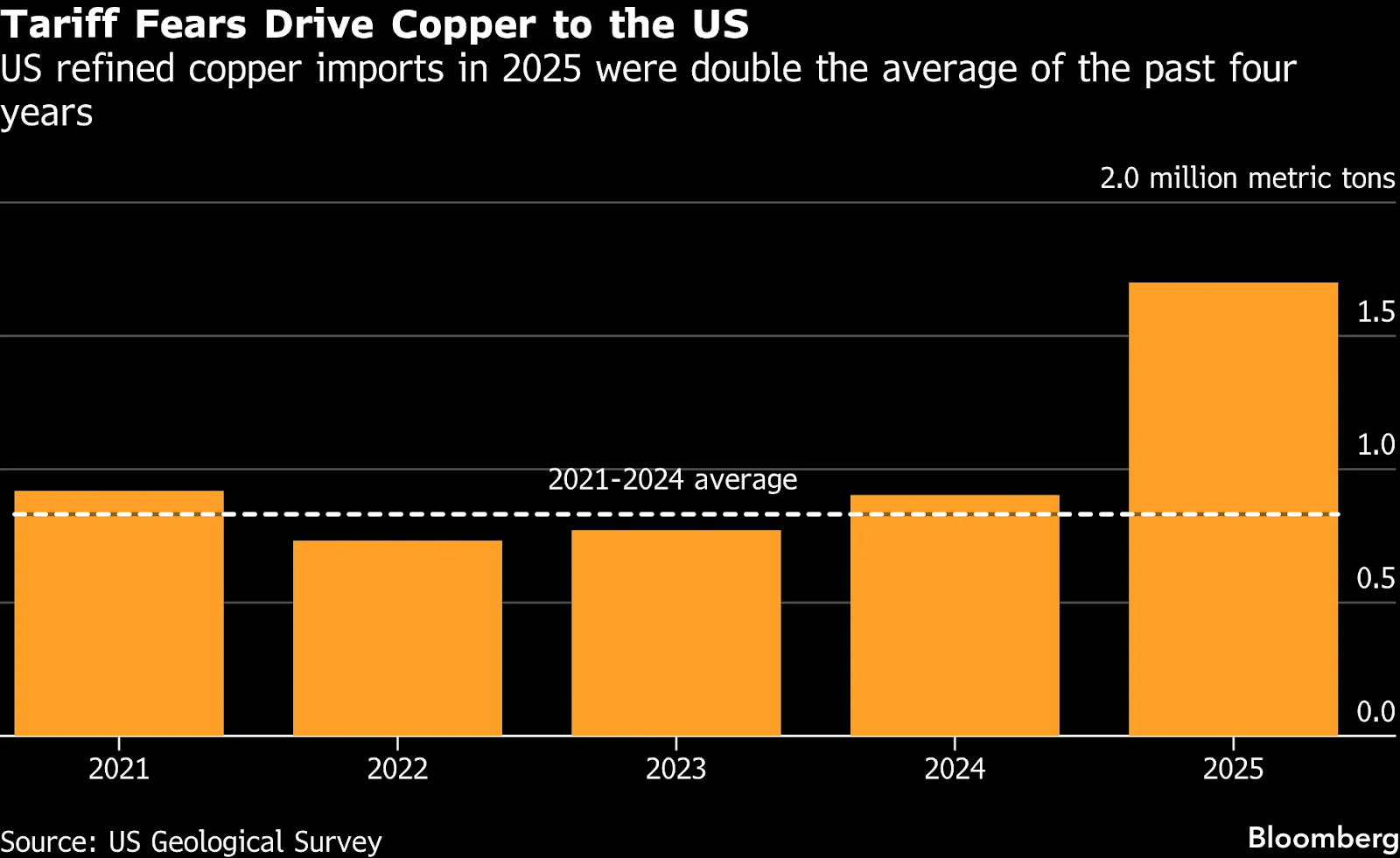

This may sound like exaggeration, but this is almost exactly what happened to copper in 2025. Relative prices went up, and the metals followed the markets, will of America’s adversaries be damned.

The conventional wisdom in DC right now seems to be that critical minerals is an exhaustive list of elements crucial to American security. We have to secure the supplies! The US has turned its back on mining and on metals while China has become a metals superpower. China is a rare-earths super power. In the words of Deng Xiaoping, “The Middle East has its oil, China has rare earths.” China controls much of rest of the power electronics supply chain as well and has increased share through strategic investments. The West hasn’t made the same investments.

However, there is a massively important distinction between the words “can’t” and “haven’t.” The United States hasn’t built many mines or refineries in recent memory due to a combination of low metals prices (which makes production uneconomical), difficult permitting processes, and a lack of urgency due to easy access to metals from elsewhere. While prices of the most common base metals rose significantly with the China shock in the 2000s, they fell pretty significantly in the 2010s before rising again in recent years. With an industry like mining requiring long-term high profits to justify investments, prices have not yet reached levels that make mining in the US economical for the most part if all costs are considered.

A similar trend plays out in rare earths where prices have, until recently, not risen enough to make it worthwhile to mine or refine pretty much anywhere from China. Dumping concerns aside, the West is not incapable of producing most-rare earths given the proper incentives.

Commodity markets may be highly financialized, but don’t pretend for a second that seasoned Rio Tinto and Glencore traders are not able to move mountains when the price is right. Just a reminder that Marc Rich, founder of Glencore and maybe the most famous commodity trader of all time, literally fled to Switzerland to avoid prosecution for trading precious metals with Apartheid South Africa. The commodity market is littered with daring stories of creative circumvention in times of profit from oil deals with Libyan rebels to shiptracking avoidance to skirt Russian sanctions.

The critical distinction: while lithium, copper, and even most rare earths are obtainable with proper incentives, some elements are not. Gallium and certain rare earths necessary for power electronics top this list. The power electronics supply chain is a case study in an industry where no amount of money will fix a shortage caused by conflict with China in the medium term. We need to move beyond conversations about general bottlenecks to ones that separate the gallium from the copper.

Power Electronics, HVDC, and the Future of the Grid

To understand the bottlenecks to the electric supply chain, it is instructive to start by understanding power electronics. Power electronics, the semiconductor devices that convert, control, and condition electrical power, are reshaping grid architecture. At the center are wide-bandgap (WBG) semiconductors: silicon carbide (SiC) and gallium nitride (GaN). Both offer fundamental advantages over conventional silicon including higher voltage handling, better thermal performance, and faster switching speeds. SiC has emerged as the enabling technology for high-power grid equipment like converters and solid-state transformers. GaN dominates lower-voltage applications: data center power supplies, fast chargers, and 48V rack-level distribution. Both remain more expensive than silicon, but total system costs often favor WBG devices once you account for smaller passive components, reduced cooling, and lower energy losses over time.

Why does this matter for the grid? Four primary applications stand out:

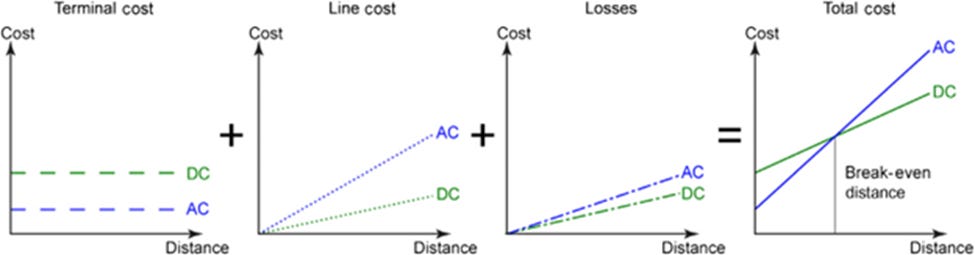

HVDC transmission is the most capital-intensive application. AC power is rectified to DC at a converter station, sent long distances, and inverted back to AC at the receiving end. HVDC has higher terminal costs but lower per-kilometer costs and losses than conventional AC. For overhead lines, the breakeven distance is typically 400-800 km; for submarine cables, it drops to 25-70 km because AC cables suffer from capacitive charging currents that scale with distance. Modern HVDC systems use voltage source converters based on modular multilevel converters (MMCs). MMCs are built from hundreds or thousands of submodules, each containing power semiconductor switches and capacitors. These are prime candidates for SiC adoption.

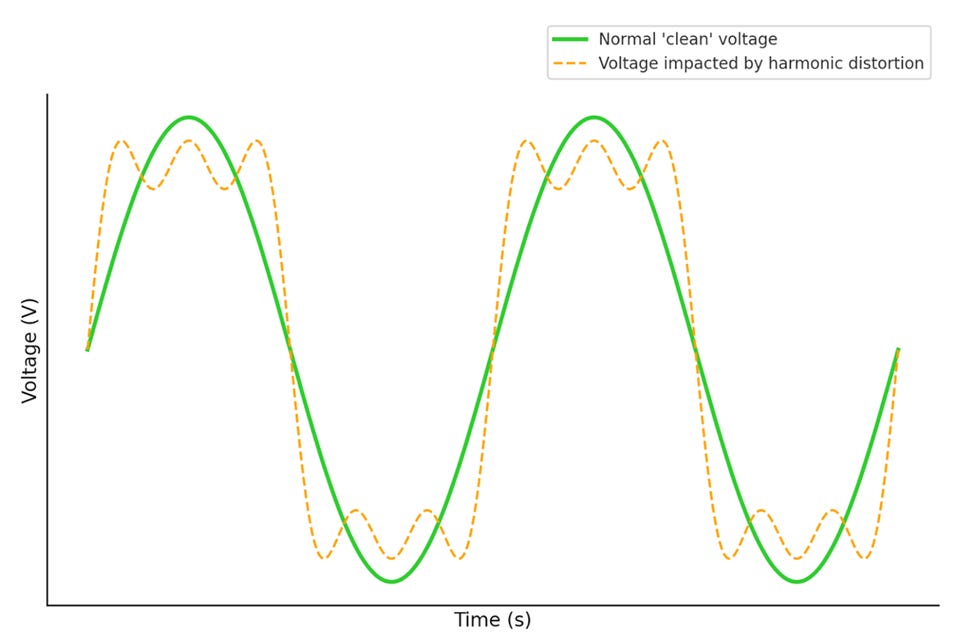

Solid-state grid protection is increasingly critical. Traditional mechanical circuit breakers respond in tens of milliseconds. Solid-state circuit breakers (SSCBs) using SiC or GaN transistors can interrupt fault currents orders of magnitude faster. SSCBs are essential for preventing the cascading failures that become more likely as renewable penetration reduces system inertia. Because they switch electronically rather than mechanically, SSCBs eliminate electrical arcing and contact degradation, reducing maintenance and improving lifetimes. They prevent voltage frequency distortions like the one shown here.

Grid-forming inverters and FACTS devices provide the rapid voltage and frequency control that grids need as synchronous generators. FACTS naturally resist frequency deviations through rotational inertia and give way to inverter-based renewables. A STATCOM based on MMC technology can inject or absorb reactive power within milliseconds, and newer designs integrating battery or supercapacitor storage can emulate the inertial response of synchronous machines.

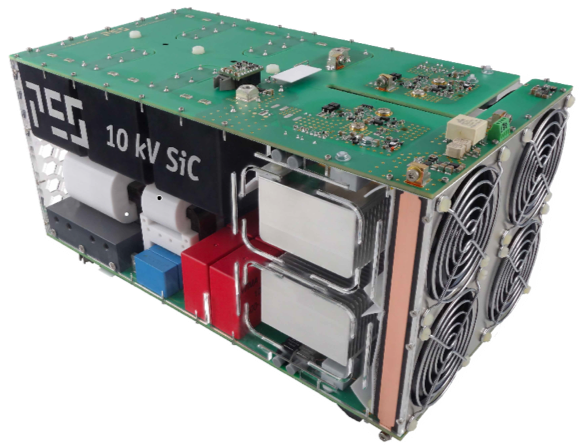

Solid-State Transformers (SSTs) are emerging as a disruptive technology to traditional transformers. It’s the classic story of silicon replacing iron as technology gets more complicated. A conventional power transformer is fundamentally a passive device: copper windings, a steel core, and insulating oil. Transformers traditionally step voltage up or down through electromagnetic induction, unchanged in expensive basic design for over a century.

That traditional transformers face major bottlenecks is almost a meme as discussed at the top of the piece. On the manufacturing side, transformers are made-to-order, not mass-produced. Transformer manufacturing involves highly specialized steps like precision winding, drying, and insulation layering that can only be done by specialists and at a limited number of factories worldwide. Transformers are hard to build, difficult to scale and have long manufacturing times.

On the input side, a main driver of the transformer shortage is the long lead times for Grain-Oriented Electrical Steel (GOES). GOES minimizes hysteresis losses and is highly magnetically permeable in one direction, making it ideal as a material for transformers. Other major metals inputs to traditional transformers include copper and aluminum.

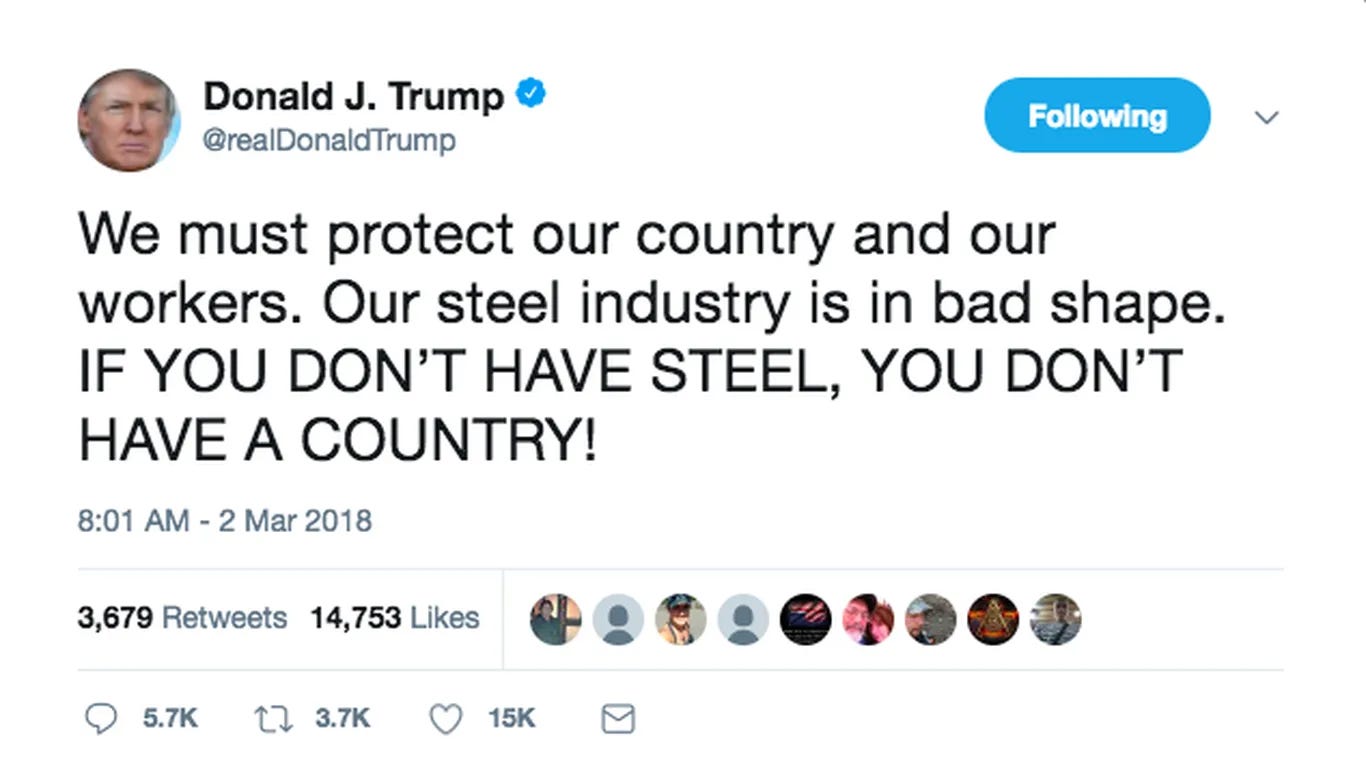

The creation of GOES is highly specialized and concentrated with only a few producers worldwide, such as Baowu Group, Nippon Steel, and POSCO. China alone produces 56% of GOES. Currently, the US produces only 12.5% of global GOES, with major declines in a once-dominant industry due to underinvestment and foreign subsidization. Cleveland-Cliffs in Ohio is the only producer of GOES in North America, with production capacity for only 240 thousand tons compared to estimated North American consumption of 489 thousand tonnes. The perpetual lack of domestic supply comes despite over a decade of handwringing over the need for US steel. As President Trump said back in 2018, “if you don’t have steel, you almost don’t have much of a country…” Policymakers promise to bring back US steel, David Riccardo be damned.

Solid-state transformers replace iron-and-copper blocks with fast power converters and medium- or high-frequency transformers, collapsing multiple pieces of grid equipment into a single unit. SSTs are transformers, rectifiers, inverters, and voltage regulators all in one. The result can be up to 14 times smaller and roughly 40 times lighter than the equipment it replaces. More importantly, an SST is an active, controllable device: it can regulate voltage in real time, enable bidirectional power flow between AC and DC systems, and provide grid-support functions that a passive transformer simply cannot.

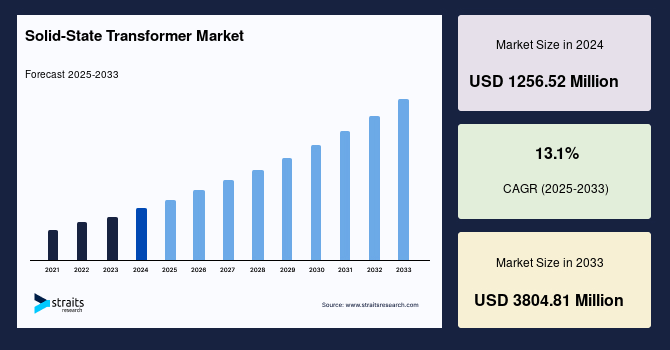

SSTs are still in the process of broader adoption, but they are no longer science experiments. The market for SSTs is expected to more than triple by 2033, according to forecasts from Straits Research.

SSTs also differ significantly from traditional transformers in terms of components. SSTs trade iron for silicon and gallium and thus contain almost no GOES. SSTs are thus thankfully less exposed to the challenges imposed by steelmaking and the difficulty of establishing a US GOES industry. Unfortunately, SSTs are significantly more sensitive to the supply chain for Gallium and advanced magnets. China leads in both and produces over 85% of the types of advanced magnets needed for SSTs. While not ideal, SiC can substitute for GaN if needed. Even with this substitution, there is still significant exposure. It would be ironic to fix the long maligned transformer shortage and associated chokepoint by switching to a technology that has similar dependencies and no plan for independent production.

Amperesand, a startup founded by veterans of ABB, GE, Siemens, and Vestas, raised $80 million in late 2025 and is delivering its first commercial units in 2026, targeting hyperscaler data centers, megawatt EV charging, and utility customers. DG Matrix raised $60 million in a Series A and has partnered with PowerSecure, a Southern Company subsidiary, to deploy SST-based power infrastructure for AI data centers.

SSTs also have significant potential for utilization in the electrification of transportation. WattEV has developed an SST for megawatt-class heavy-duty truck charging, with production-ready units expected in 2026.

SSTs are built on Wide-bandgap (WBG) semiconductors. These are primarily SiC for the high-voltage stages. Every SST deployed provides demand for SiC devices and substrates that grid-scale HVDC converters need. One of the most promising applications is converting medium-voltage AC from the grid directly to 800 VDC for AI data centers, bypassing the conventional transformer entirely and sidestepping the interconnection queues that have become a major bottleneck for new datacenter capacity. SSTs could modernize and transform the grid, but they could also significantly increase total WBG semiconductor demand, further straining critical supply chains. This does not necessarily have to be bad, as SSTs could also incentivize new investments in power electronic ecosystems with enough adoption.

The combined effect is a restructuring of grid economics: HVDC expands markets for remote renewables, FACTS devices reduce ancillary service costs, solid-state protection contains faults faster, WBG power conversion reduces the energy overhead of running data centers, and SSTs make the grid more compact and transformers more efficient.

In data centers specifically, SiC-based uninterruptible power supplies achieve efficiencies up to 98 percent in double-conversion mode, compared to 94-96 percent for silicon designs. At the scale of a hyperscaler consuming hundreds of megawatts, those percentage points translate into serious money. The pace of WBG cost reduction, which is driven by the shift from 6-inch to 8-inch SiC wafers and rising GaN production volumes, will significantly determine how quickly these transitions unfold.

Not just a grid technology anymore: Data Centers

While most grid policy discussions treat HVDC as a long-distance transmission play, the most immediate source of demand growth for SiC and GaN power electronics may be happening inside data centers. NVIDIA is leading a transition to 800 VDC power distribution within AI data centers, replacing the traditional 54-volt in-rack architecture that has been standard for years. The shift is driven by physics: as AI racks scale from tens of kilowatts to hundreds of kilowatts and eventually to one megawatt per rack, the old architecture breaks down.

At megawatt scale, 54-volt distribution would require copper busbars weighing over 200 kilograms per rack and power shelves consuming most of the available rack space, leaving no room for compute. An 800 VDC architecture converts medium-voltage AC from the grid to 800 volts DC at the facility perimeter and distributes it directly to racks, eliminating multiple conversion stages. NVIDIA expects this to improve end-to-end power efficiency by up to 5 percent, reduce maintenance costs by up to 70 percent, and cut total cost of ownership by up to 30 percent. Full-scale production is planned to coincide with NVIDIA’s Kyber rack architecture in 2027, which will house 576 Rubin Ultra GPUs.

Grid-scale HVDC moves power hundreds of kilometers from a wind farm to a city. Datacenter HVDC moves power tens of meters from the building’s perimeter to the GPU. Both require the same underlying power electronics, including converters, rectifiers, and switching devices. Further, both consume SiC and GaN devices at volume; however, the vendor landscapes are quite different.

Grid-scale HVDC converter stations are built by the four companies discussed later in this article — Hitachi Energy, Siemens Energy, GE Vernova, and Mitsubishi Electric. The 800 VDC datacenter ecosystem, however, has a broader and different set of players. The companies building the power racks, sidecars, and distribution systems for 800 VDC data centers are firms like Delta, Eaton, Schneider Electric, Vertiv, Flex, and LiteOn. The silicon going into these systems comes from a wide range of WBG semiconductor vendors, including Infineon, Navitas, onsemi, ROHM, STMicroelectronics, and Innoscience. CoreWeave, Lambda, and Together AI are among the companies already designing for 800-volt data centers.

The supply chain implications cut both ways. On one hand, datacenter 800 VDC creates enormous new demand for the same WBG semiconductors that the grid needs, potentially accelerating cost reductions through volume. Datacenter VDC also creates a market for domestic VDC and encourages innovation in the products. However, threats to transmission and grid modernization are also threats to AI infrastructure and the rise of compute. The power grid supply chain and the AI supply chain are converging, and policymakers have not caught up. We need to update our playbook to treat power electronics as seriously from a supply chain risk perspective for AI as GPUs. We are highly exposed… and it has already been demonstrated to us.

China Already Pulled the Trigger on Gallium

Modern grid-scale power electronics run on either SiC or GaN. This creates a rift in the semiconductor market that the economic security community has largely overlooked. While most supply chain discussions have focused on chips for computing, power semiconductors actually dwarf computational semiconductors as a demand source for silicon.

A stable power electronics supply chain is becoming as important to economic security as the GPU supply chain. Power electronics are key to building a grid that can tolerate failures without widespread contagion. One need only look to last year’s blackouts on the Iberian Peninsula to be reminded that renewable-intensive grids are susceptible to cascading failures due to lower inertia.

Arguably one of the most concerning risks for the development of AI right now is the potential for political backlash. If we look back to the hardy response to the blackouts in the mid-1990s, including the formation of NERC, it becomes clear that systemwide grid challenges will result in major public backlash. This could halt AI right in its tracks. Thus, a more reliable grid is crucial not just to developing AI but to maintaining long-term public support for AI development.

So why SiC and GaN? These materials offer higher efficiency, better thermal performance, and faster switching speeds. All of these matter enormously at grid scale. The SiC power semiconductor market was valued at roughly $2.1 billion in 2024 and is projected to reach over $21 billion by 2034.

GaN devices require gallium. Gallium is a soft, silvery metal with atomic number 31. It is best known for its unusually low melting point of 86 degrees Fahrenheit (30 degrees Celcius) just below human body temperature.

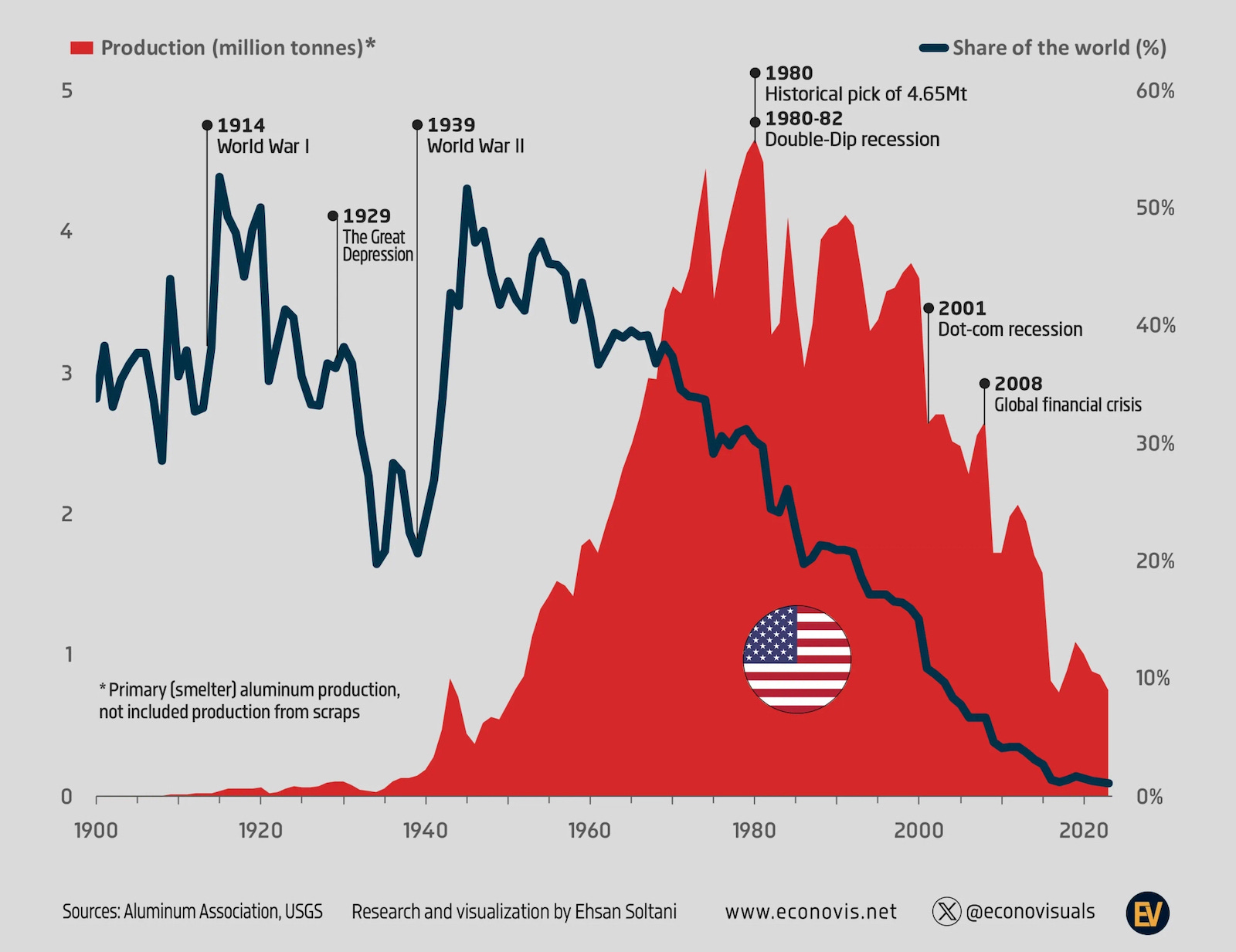

Gallium is not primarily mined alone. In the same way that the silver market is structurally linked to the copper market, Gallium is closely linked in production to aluminum. Gallium does not occur in concentrated ore deposits; nearly all production is recovered as a byproduct of processing bauxite for aluminum. This feature of the market structurally ties gallium supply to aluminum production decisions. The US has gone from the leading producer of aluminum to a bit player. Aluminum market share peaked at over 50% of global production in both World War periods, while US production peaked at 4.65 million tonnes per year with 40 smelters in 1980. As of 2023, the United States produced .75 million tonnes or just 1.1% of global aluminum production. The fall of aluminum production in the US is highly tied to the increasing dependence on China for gallium, with the last major US producer at Apex Mine in Utah closing in 1988 as production was offshored.

While pictures of metal melting in a human hand are cool, gallium’s strategic importance comes from its technological value as it has unique properties that enable Gallium Nitride semiconductors. GaN’s bandgap is roughly three times larger than silicon’s, allowing GaN devices to handle higher voltages, operate at higher temperatures, and switch on and off much faster. These features are made even more impressive by the lower energy losses. GaN devices are thus well-suited for power conversion applications like inverters and chargers, where efficiency and compactness matter. Every GaN device requires gallium as a fundamental input, tying the growth of wide-bandgap power electronics directly to the security of gallium supply chains.

China controls approximately 99 percent of global low-purity gallium production according to the United States Geological Survey. In December 2024, Beijing banned all exports of gallium to the United States as part of the tit-for-tat tech trade war. By May 2025, the Rotterdam price had surged to $687 per kilogram. This was up over 150 percent from pre-restriction levels. Prices inside China actually fell due to domestic oversupply. This is the classic Chinese playbook, and it significantly preceded the more publicized bans on rare earth exports.

Unlike many other elements where US production is merely uneconomical, gallium has negligible domestic production and minuscule output among US allies.

Diversification timelines are measured in years, and it’s unclear that gallium can be fully diversified away from Chinese sources on any reasonable timeline, given Chinese dominance of both reserves and the full supply chain. In November 2025, the DoD used the Defense Production Act to provide approximately $30 million for gallium recovery in Louisiana. Notably, this was only for recovery from waste, not original mining.

A Greek metals group, Metlen, plans to produce 50 tons annually by 2027 as part of an EU strategic project. Korea Zinc, which recently received a Pentagon cash infusion, has committed to development of a smelter in Tennessee and is considering gallium expansion, but the economics remain unconvincing even with policy support. In November 2025, China temporarily suspended its export restrictions for one year as part of a broader diplomatic détente; however, the leverage isn’t going away.

What about silicon carbide? A reminder: SiC is chemically similar to industrial diamond. China dominates production with over 60 percent of global output. North American production of silicon carbide at the abrasive level has collapsed from 160 kilotons per year in the 1970s to roughly 40 kilotons today. The US maintains a lead in the more specialized segment of SiC substrate manufacturing. Wolfspeed is the world’s largest producer and is building a new facility with up to $750 million in CHIPS Act funding. It should be noted, though, that substrate manufacturing is only one node in a longer chain.

The graph above shows the current state of the industry with GaN dominating lower-voltage, high-frequency applications and SiC serving higher-power use cases. The boundary is shifting though. Many analysts, including Navitas Semiconductor, Infineon Technologies, and Aixtron, have begun pushing for higher-power GaN applications. Ongoing improvements in reliability and cost are challenging the current landscape of segmentation.

Then, there are rare earths. Rare earths is really a misnomer as the elements are distributed throughout the earth’s crust and are not necessarily rare. They are, however, often found in small concentrations that make them uneconomical to mine. Mountain Pass has significant supplies of lighter rare earths, but heavier elements like dysprosium and terbium remain difficult to produce domestically.

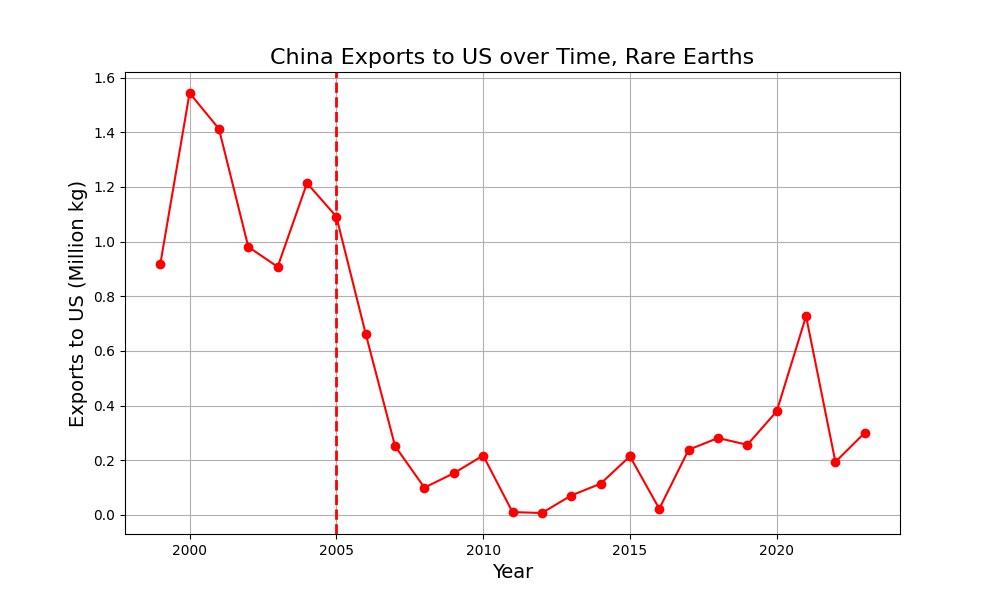

Permanent magnets containing neodymium, praseodymium, and dysprosium are essential for power electronics packaging. China’s rare earth export restrictions aren’t new — exports to the US peaked in 2000 and have been restricted in various forms for almost two decades. In April 2025, China imposed controls on seven additional elements. The 2025 USGS Critical Minerals List identified rare earth elements as posing the highest economic risk from supply disruption. The US lost its position to the higher cost of mining in the United States and the inability to fulfill environmental standards at a reasonable cost.

Rare-earths mining is highly extractive and dirty, which created an environmental backlash that made mining in the US nearly impossible. The United States is a beautiful country, and protecting it from mining is admirable stewardship of the environment. However, shifting the burden to countries with low state capacity and appalling records for human rights and environmental protection actually make environmental harm worse. Just because a glory hole is not in your backyard, doesn’t mean it doesn’t exist. It is important to push for common standards across the supply chain both to prevent coerced labor and environmental degradation and to keep US suppliers competitive. These tradeoffs further the inherent supply chain risks. To truly understand where the risks come from though, we must analyze and understand the layers of the supply chain network.

The Supply Chain for Power Electronics

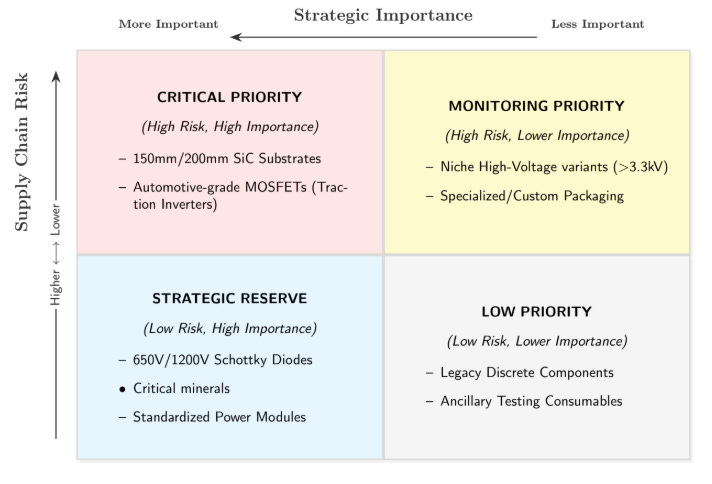

As with any supply chain analysis, we begin with the two canonical frameworks: a two-by-two matrix and a multi-echelon flow diagram. When thinking about supply chain risk, one axis captures risk or controllability while the other captures strategic importance.

For SiC semiconductors, MOSFETs (voltage-controlled devices for switching and amplifying signals), gallium, and SiC substrates sit in the high-risk, high-importance quadrant. These supply chains are difficult to diversify. Most other critical grid minerals are important but less risky. The power electronics supply chain discussion often fails to make this distinction, conflating easily obtainable materials with goods that are essentially impossible to procure without dedicated resources.

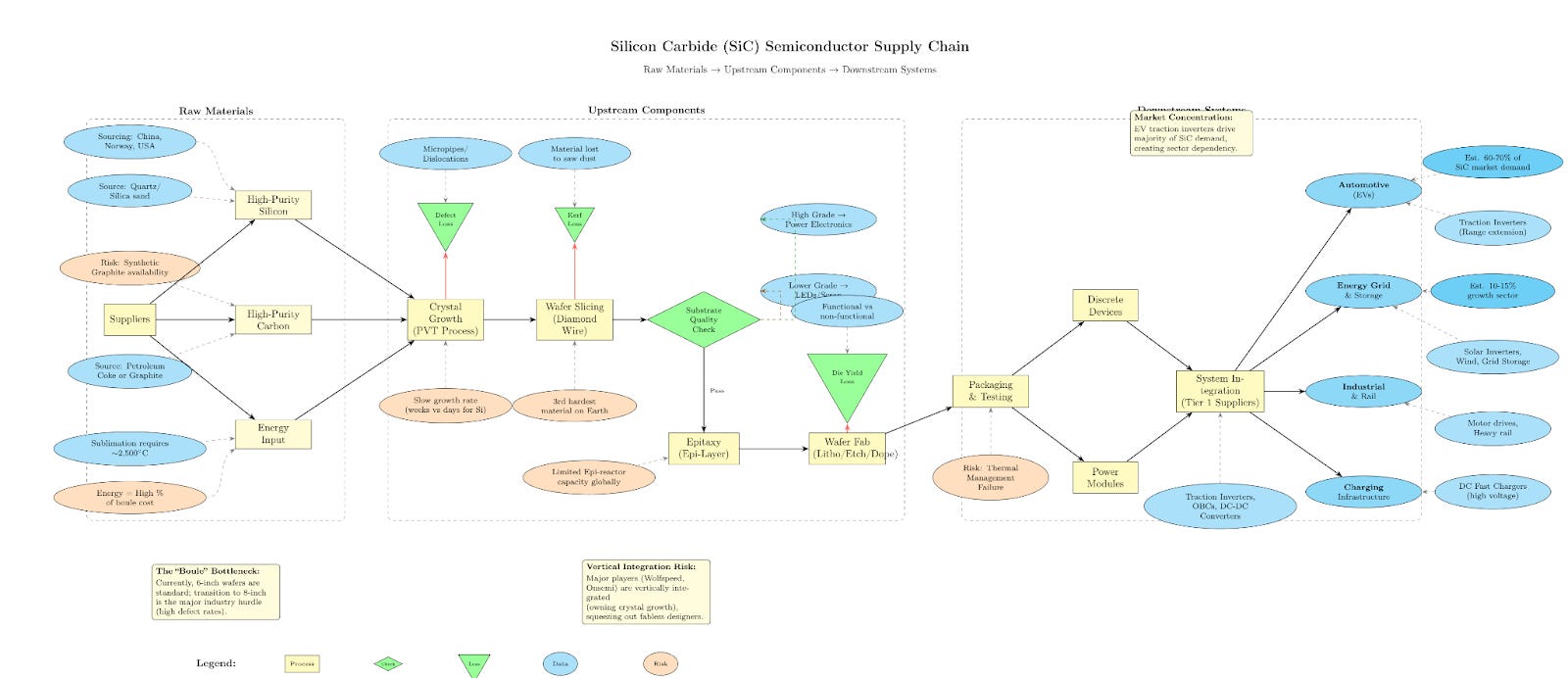

Below is the promised flow diagram. It is an illustration of the supply chain specifically for SiC semiconductors. Flowing from raw materials to upstream components to downstream systems. Risks are labelled in rust-colored red with losses and checks in green, and processes in beige.

The supply chain begins with two common raw materials: silica sand and petroleum coke, combined at extreme temperatures to form silicon carbide powder. While these starting materials are globally available, China dominates this initial processing step, accounting for over 60 percent of worldwide SiC powder production. This domination is a reflection of lower energy costs and less stringent environmental regulations for the energy-intensive furnace operations required.

The powder must then be transformed into large, nearly perfect single crystals through a process that takes one to two weeks per crystal and requires extraordinary precision. This crystal growth stage is a key chokepoint where the United States maintains a stronger position. Wolfspeed is building the world’s largest SiC substrate facility in North Carolina. But Chinese producers are rapidly expanding, and the slow, technically demanding nature of crystal growth limits how quickly any country can scale.

Beyond silicon carbide, the supply chain depends on materials with even more severe concentration risks. Gallium is almost entirely controlled by China at 98 percent of global supply. It’s not mined directly but recovered as a byproduct of aluminum production, and China has already demonstrated willingness to restrict exports. Rare earth elements used in power electronics packaging flow predominantly through Chinese processing facilities, which handle over 80 percent of global refining despite other countries possessing substantial ore deposits.

Downstream manufacturing presents different vulnerabilities. Semiconductor packaging and assembly are heavily concentrated in East Asia, including Taiwan, South Korea, Malaysia, and China. A crisis in the Taiwan Strait would simultaneously threaten multiple supply chain nodes, as Taiwan hosts critical packaging capacity alongside its dominant position in advanced logic chip manufacturing.

How the US Lost the Power Electronics Supply Chain

Like most skill-intensive manufacturing industries, power electronics did not start as China’s domain. Photovoltaic solar panels, the original grid semiconductors, got their start in the United States. Starting at the upstream of the supply chain, it should be noted that Chinese firms have outpaced Western firms from mining to components to manufacturing, creating not just a lead in power electronics but the ecosystem to support it.

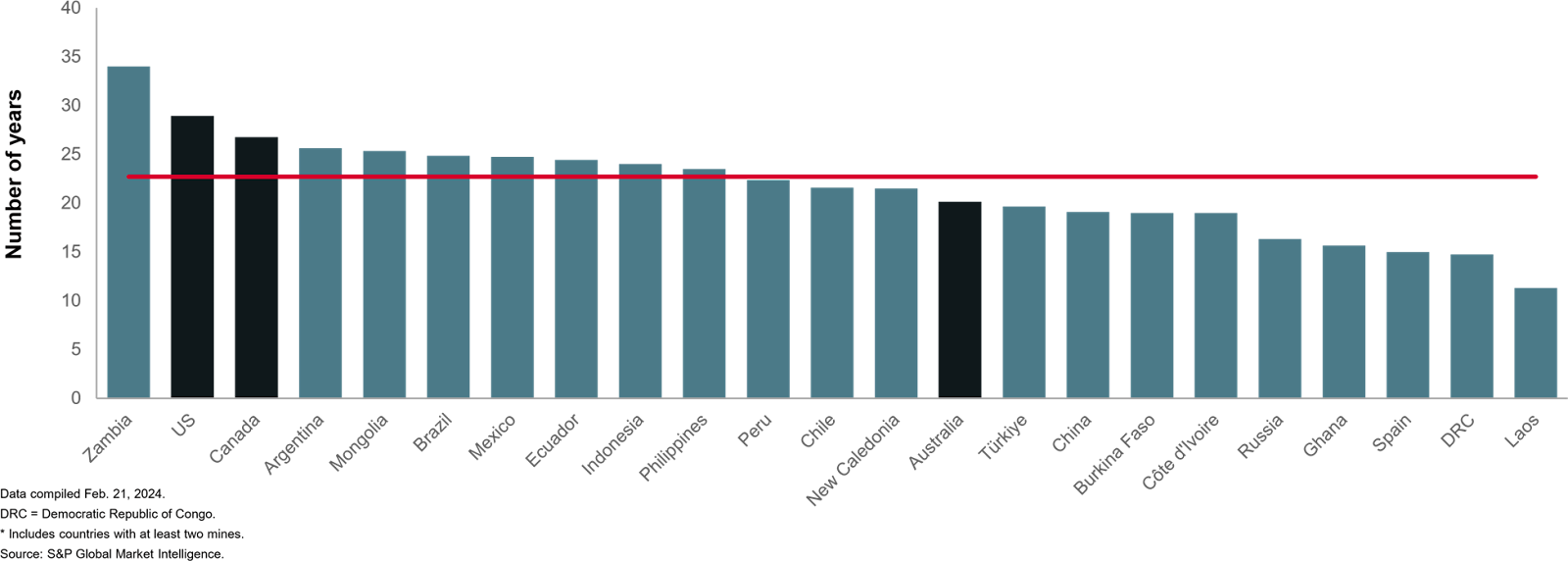

Even if Western majors were ready to pull the trigger on mining in America, it would take over two decades for the mines to materialize. As the following chart shows, the US has one of the longest lead times for new mines at over 25 years on average. This lag persists despite recent efforts at reform.

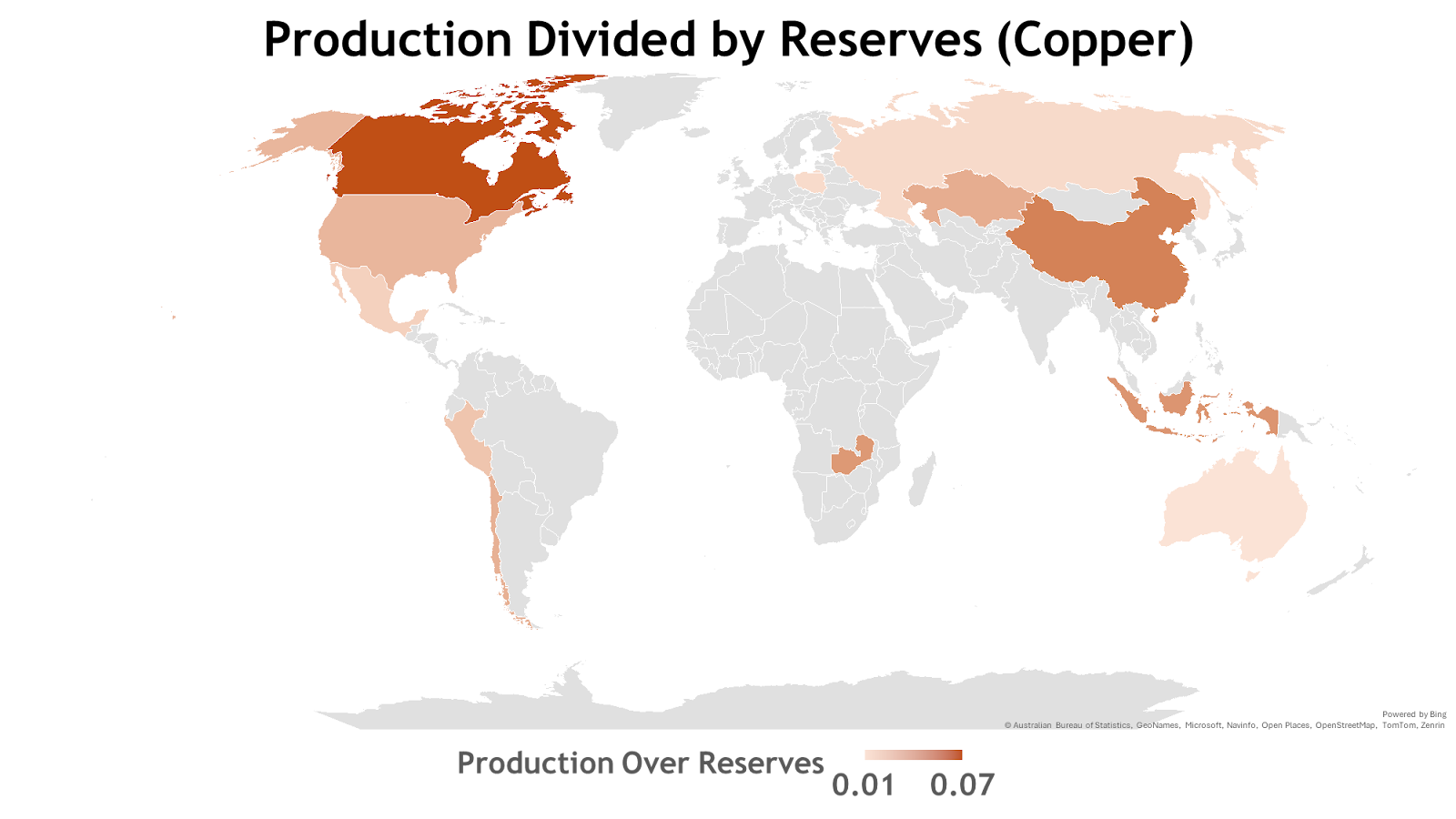

It should be noted that nothing is stopping the US from building mines quickly for most ’critical minerals’ if the political will materializes. The following graph highlights that the US has one of the lowest production-to-reserves ratios for copper in the world, with other major metals like lithium having similar maps.

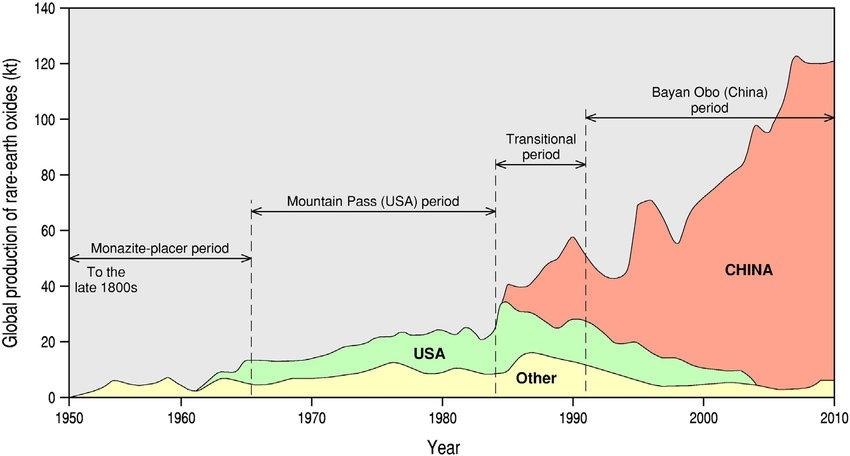

The US has also lost its edge in rare earths. Since the Mountain Pass closure, the US has gone from a leader to a minor player, though rare earth exports have recovered somewhat since the late 2010s.

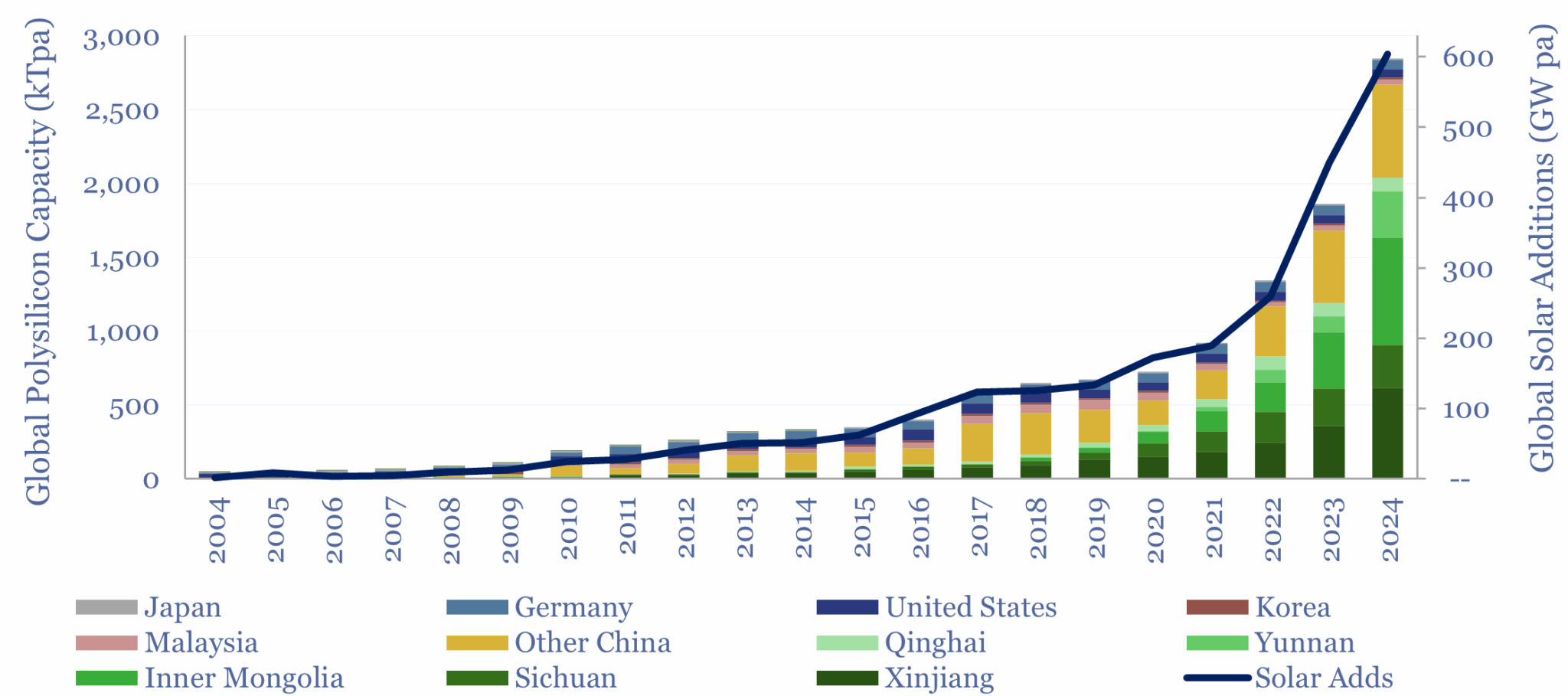

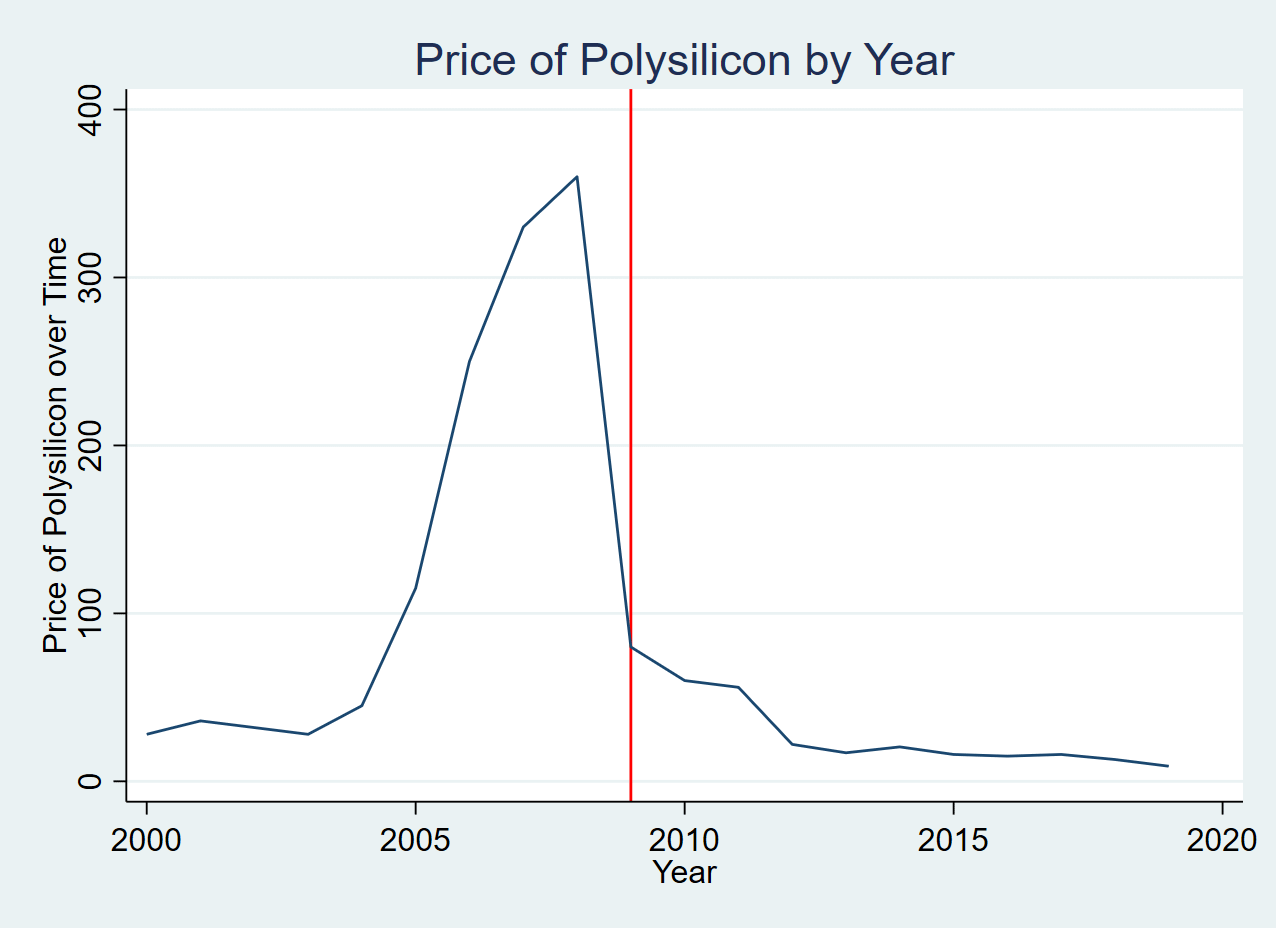

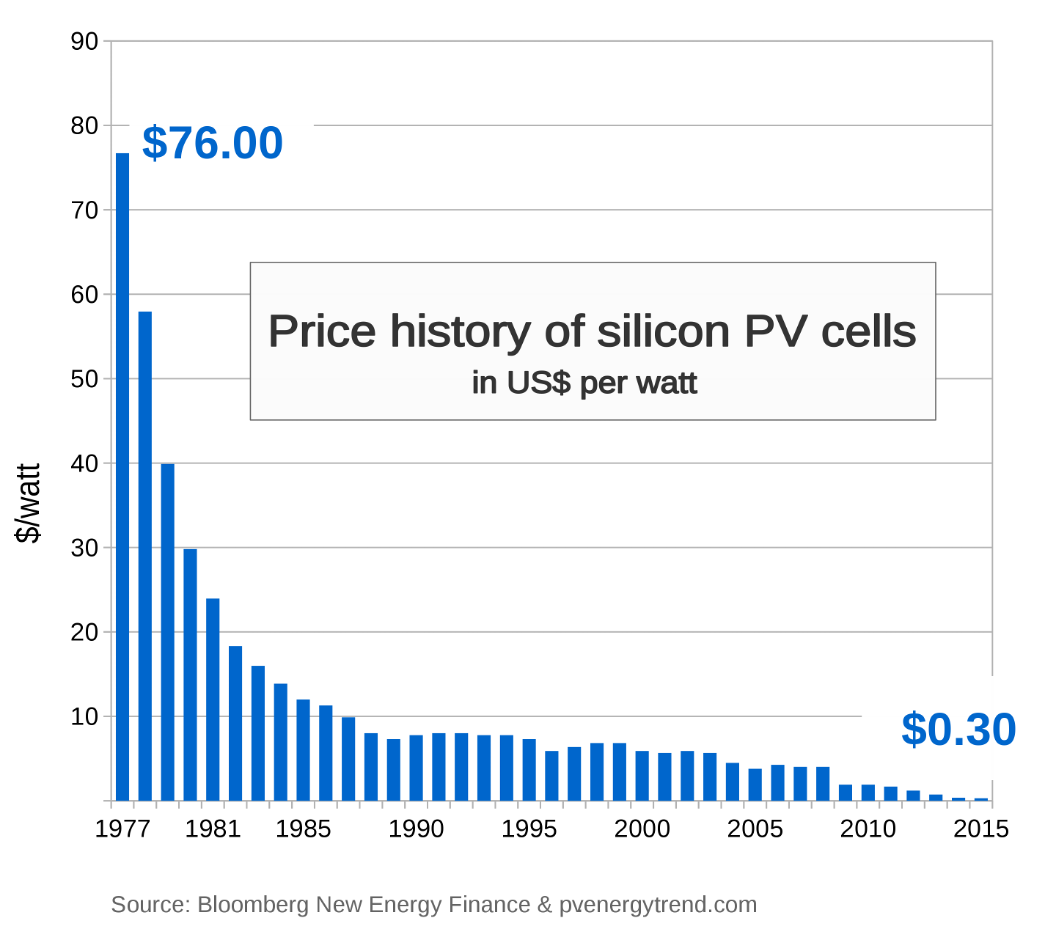

Chinese polysilicon subsidies drove major capacity expansions in both production and refining.

The beginning of Chinese input subsidies and polysilicon “dumping” is visible in price data. In 2009, with China’s Golden Sun program and broader semiconductor push, polysilicon prices fell sharply in the domestic market, becoming relatively cheap compared to the rest of the world.

The upstream investments supercharged downstream effects. These polysilicon subsidies worked with the learning-by-doing inherent in solar manufacturing to fuel a remarkable rise in Chinese solar capacity. China took the lead in photovoltaic modules, power semiconductors, and many parts of the grid power electronics supply chain. Innoscience in China alone supplies nearly 30 percent of global GaN devices, according to Trendforce.

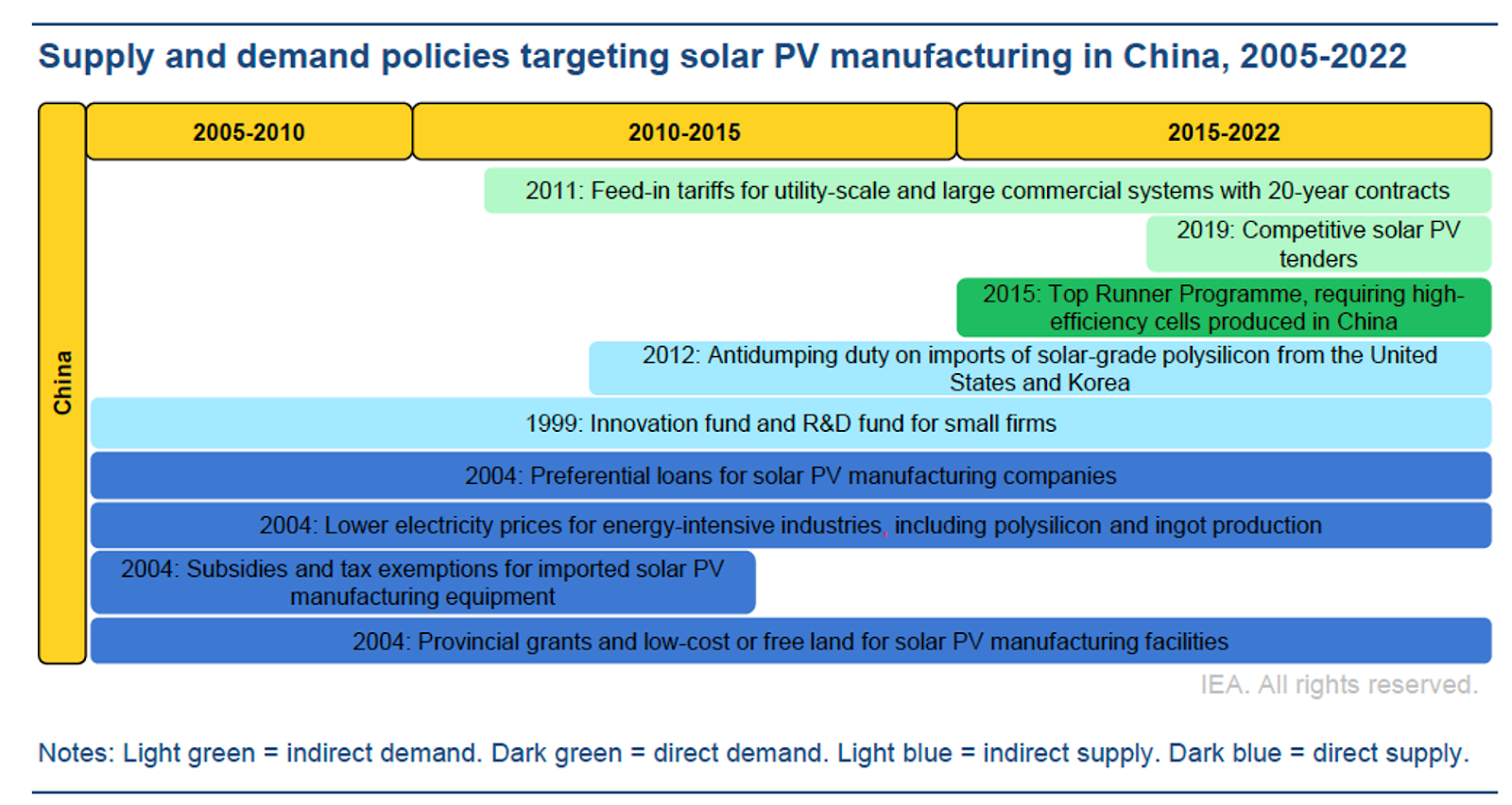

China’s upstream policies didn’t happen in a vacuum. Beijing pursued aggressive subsidies in both photovoltaic and power electronic semiconductors, while its massive buildout of ultra-high-voltage transmission lines provided enormous domestic demand for HVDC systems.

The integration of supply and demand policies throughout electronic supply chains creates a significant boost in the electricity space, majorly benefitting from an ecosystem. PV manufacturing is an example where this has played out quite well.

There are benefits to the West that shouldn’t be overlooked. Photovoltaic panel prices have fallen dramatically, and much of the research and development of HVDC systems has come out of China. Cost reductions were largely driven by found efficiencies and deployment-driven reductions from solar’s steep learning curve; however, China’s subsidies undoubtedly played a role in the development of industry leadership. With those low prices comes exposure that the US should work to reduce.

What’s Actually Inside an HVDC System

To understand why these dependencies matter, you need to understand what modern HVDC actually looks like. These systems are far more complex than most people realize, and they demonstrate the challenges facing the broader grid supply chain.

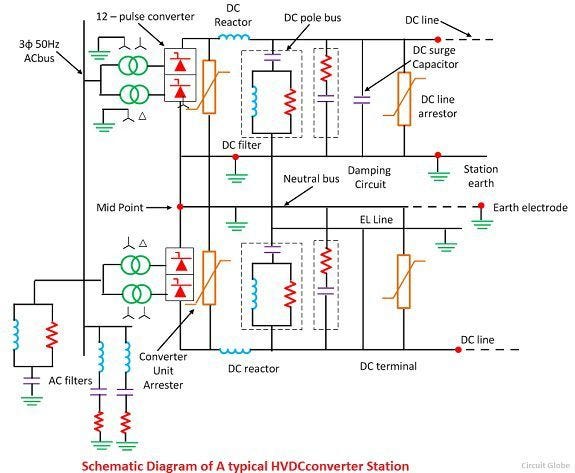

HVDC has existed since the 1950s, but the technology has changed radically. Modern systems predominantly use voltage source converters based on modular multilevel converters. An MMC is built from hundreds or thousands of individual submodules. Each submodule contains power semiconductor switches and capacitors connected in series to synthesize high-voltage waveforms. A large power transformer is essentially a precisely wound electromagnetic device: copper, steel, and insulating oil. An MMC converter station is closer to a semiconductor fab in miniature.

The global HVDC market is projected to grow from roughly $15.6 billion in 2025 to over $22 billion by 2030. Asia Pacific dominates with over 50 percent of installed capacity, driven by China’s massive ultra-high-voltage DC projects. North America accounts for only about 8 percent. The converter station, where AC is converted to DC and back, is the most complex and expensive component, accounting for approximately 55 percent of total system cost. This is where supply chain vulnerabilities concentrate.

China’s UHV buildout has generated massive domestic manufacturing scale in precisely these technologies. Companies like TBEA, NR Electric, XJ Electric, and Xuji Group now supply complete UHVDC systems. The equipment supply chain functions as what industry analysts describe as a “regulated duopoly” between SGCC and China Southern Power Grid, which together accounted for an estimated 94 percent of EPC awards in 2025. Chinese domestic suppliers reportedly commanded 68 percent of submarine HVDC cable orders that year, undercutting European competitors through shorter delivery cycles.

Hitachi Energy, Siemens Energy, and others retain expertise in advanced VSC technologies and ultra-high-voltage components. Only two global vendors can currently deliver the 8.5 kV thyristors needed for ±1,100 kV valve assemblies. The picture isn’t total Chinese dominance yet, but there’s a clear trend of consolidating Chinese capabilities in systems integration and high-volume manufacturing, with Western firms maintaining positions in specialized components.

Four Companies Build the World’s Converters

Move up from raw materials to system integration, and a different concentration risk emerges. The global HVDC converter station market is dominated by four companies: Hitachi Energy, Siemens Energy, GE Vernova, and Mitsubishi Electric. The technical barriers to entry are enormous. VSC-HVDC converter design requires deep expertise in power electronics, control systems, high-voltage engineering, and systems integration that takes decades to develop.

Corporate restructuring has intensified this concentration. Hitachi Energy was once ABB’s power grids division. ABB was arguably the most important single organization in HVDC history. ABB pioneered commercial HVDC in the 1950s and claims involvement in roughly half of all HVDC projects ever built. In 2020, Hitachi acquired an 80.1 percent stake. One of the world’s most critical bodies of grid engineering expertise now sits within a Japanese conglomerate rather than the European industrial ecosystem that developed it. GE Vernova emerged from General Electric’s 2024 breakup. Siemens Energy operates with a record $158 billion order book and significant backlog; some turbine frames are sold out for seven years.

The net effect: HVDC supply and critical grid equipment are controlled by fewer, larger entities with complex corporate structures spanning multiple jurisdictions. The United States depends on a small number of foreign-headquartered multinationals for technology foundational to grid reliability.

The Power Semiconductor Supply Chain Mirrors the Chip Industry

Anyone who reads that the supply chain for power electronics is highly dependent on small, specialized providers may be forgiven for having déjà vu. The industry concentration… the complexity… it reminds you of something… A lot of these stories and features are shockingly close to the challenges we have seen in the supply chain for chips. The power semiconductors inside MMC converter stations have their own multi-continent supply chain, and it shares many of the vulnerabilities ChinaTalk readers know from the broader chip industry.

SiC crystal growth uses physical vapor transport at around 2,200°C, with growth rates of 0.1 to 0.5 millimeters per hour and cycle times extending one to two weeks per boule. This is not a process you can rapidly scale. SiC wafer processing is made harder by the material’s extreme hardness, which is second only to diamond. Epitaxial layers are deposited by chemical vapor deposition at approximately 1,600°C, requiring precise dopant control. Device fabrication then involves the standard semiconductor process steps — like photolithography, ion implantation, metallization, passivation — but adapted for wide-bandgap materials with dedicated equipment.

After fabrication, devices move to assembly, testing, marking, and packaging. ATMP capacity is heavily concentrated in Taiwan, South Korea, Malaysia, the Philippines, and China. This is the same concentration risk the broader semiconductor industry faces, applied with full force to power semiconductors for grid applications. Maritime chokepoints compound the logistics risk, with materials routinely traversing the Strait of Malacca, the South China Sea, and the Panama Canal.

What Does Fragility Actually Look Like?

We know that there are chokepoints, but how do we decide how risky different goods actually are? A risk assessment of the super cascode switch supply chain, a next-generation power switching technology for MMC-based HVDC systems, illustrates the range of vulnerabilities. For our assessment we can repurpose the DOE’s Threat × Vulnerability × Consequence supply chain framework on a five-point scale, the highest-risk scenario is gallium export restrictions, scoring 100 out of 125: threat probability rated 5 (greater than 35 percent annual probability, essentially ongoing), vulnerability rated 5 (severe disruption lasting weeks to months with critical path dependency), and consequence rated 4 (15–35 percent of production affected with major customer contracts jeopardized). SiC substrate shortage scores in the medium-high range of 64. A Taiwan Strait crisis scores 50 with a lower probability but maximum vulnerability and consequence if it occurs.

The cascading failure that struck the Iberian Peninsula in April 2025 is a concrete reminder of why all these investments matter. Spain and Portugal experienced a total blackout affecting 31 GW of load. This was approximately 60 percent of Spain’s national electricity demand, knocked out within five seconds. It was a harbinger of future challenges in low-inertia high-renewables grids and the first time a voltage-driven cascade under high renewable penetration with low system inertia had been linked to a blackout in a major grid. It will not be the last. The technologies needed to prevent these failures — including advanced power electronics, fast-switching devices, and HVDC interconnections — are precisely the ones with exposed supply chains. The issue becomes even more salient in the face of an explosion of highly sensitive large loads with data center and fab proliferation.

Taming the Supercycle

One important detail to note about the economics of semiconductors is that these markets are highly cyclical and subject to long cycles in a very similar fashion to commodity markets. This may seem odd for finished goods like semiconductors. However, the forces that create supercycles in commodities markets are also present in power electronics and semiconductors more broadly. Supercycles arise because both supply and demand adjust slowly, but they adjust on different timescales. Power electronics are upstream and crucial components to investments leading to volatile demand, driven heavily by intense physical investments in capacity leading to unresponsive supply, and substitutable across products to some extent.

Wolfspeed’s recent Chapter 11 filing is revealing about the brutal dynamics of cyclicality in the industry. Wolfspeed held roughly a third of the global SiC substrate market in 2024, but technological leadership does not immunize a firm from the supercycle. During the EV boom, Wolfspeed committed billions to new fab capacity in North Carolina and New York. When the cycle turned, EV demand slowed, Chinese producers like TanKeBlue and SICC rapidly expanded subsidized capacity and drove SiC wafer prices down roughly 30% in 2024, and Wolfspeed’s own fab ramp-up proceeded more slowly than expected.

Wolfspeed found itself carrying approximately $6.5 billion in debt against negative gross margins. A $750 million CHIPS Act grant that had been negotiated under the Biden administration was never finalized before the political transition, and the Trump administration’s hostility toward the CHIPS Act introduced further uncertainty at the worst possible moment. Wolfspeed filed for Chapter 11 in June 2025 and emerged 91 days later after eliminating roughly $4.6 billion in debt but largely wiping out existing shareholders. Even a dominant player could not outrun the supercycle.

Better market institutions can dampen the supercycle. Derivatives markets for compute and power electronics can improve price discovery and allow both producers and consumers to hedge against volatility. Futures and longer-term procurement contracts can reduce the incentive for speculative overbuilding. Regulatory frameworks that require environmental impact assessments before data center construction can slow the pace of development to a rate more consistent with thoughtful environmental planning. International coordination on compute capacity planning could reduce the “arms race’‘ dynamic that drives wasteful duplication of infrastructure across countries. Understanding what policies may enable stable investment cycles requires analysis and analysts.

The Analytical Gap

With the Chips Act, industry analysis was incredibly central to providing a multifaceted analysis of a critical supply chain. DOE has produced useful supply chain reports with solid methodology for evaluating threats, vulnerabilities, and consequences. A structural problem endemic to economic security exists here though: DOE is not equipped to see the bigger picture. As such, DOE’s technical reports are almost entirely disconnected from analysis of geopolitical and economic strategy.

A DOE assessment will tell you that gallium supply is concentrated in China. It will not tell you how China’s demonstrated willingness to use export controls as retaliatory instruments changes the risk calculus for grid equipment procurement. It will identify SiC substrate availability as a bottleneck. It will not connect this to the broader question of whether the United States can maintain sovereign capability in grid-scale power electronics manufacturing while competing with Asian cost advantages.

This reflects the bureaucratic reality of the U.S. government, where energy policy, trade policy, industrial policy, and national security policy are housed in different departments with different cultures and mandates. For grid equipment supply chain security, that fragmentation produces blind spots. An organization similar to Japan’s METI could be extremely useful for prioritizing the right grid investments. These grid investments require a centralized office partially because of technological and demand spillovers. Creating demand for American power electronics will likely require an entire ecosystem and mean investments in other areas of energy.

The Other Missing Market Problem

Power electronics and HVDC systems serve applications across the electricity supply chain, but US demand for these technologies has been eroding.

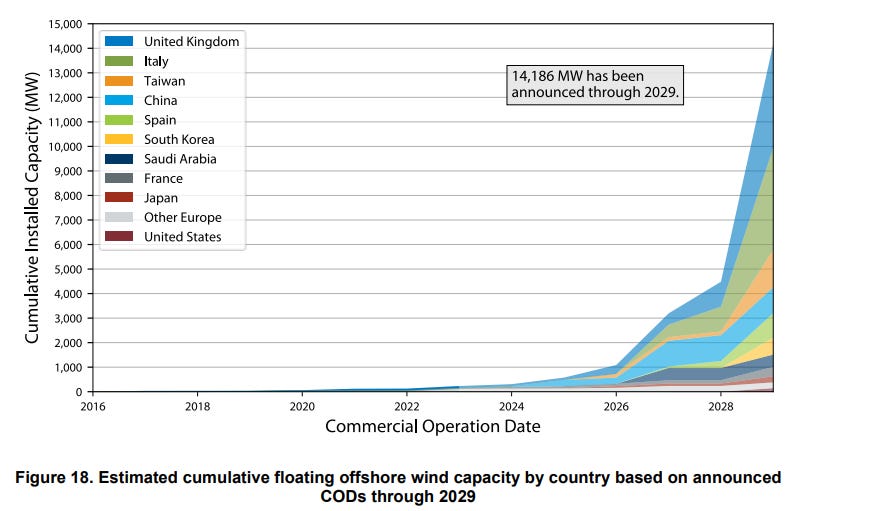

The trajectory of offshore wind illustrates the pattern. Data from the National Renewable Energy Laboratory’s offshore wind reports tells the story in two snapshots.

China invested massively in offshore wind since the 2010s, but the US and UK were not far behind. Then came the cancellations.

Much of the downturn preceded the current administration and stemmed from interest rate changes. But the result is stark: current US projections for 2030 offshore wind capacity are now below previous projections for 2027. Offshore wind is a major use case for HVDC, which enables larger systems where power must travel longer distances to reach shore.

The story repeats across batteries, HVDC systems, and solar installations. China leads in both production and deployment, creating a virtuous cycle of demand that strengthens its power electronics ecosystem.

If the US wants to develop its own power electronics ecosystem and address supply chain vulnerabilities, it needs a multifaceted approach that generates demand and supply simultaneously. Supply-side policies alone won’t get it done.

What Should Be Done

The policy toolkit is not empty. There are plenty of options at our disposal.

Make power electronics a security priority. For many reasons, power electronics are crucial to both defensive and offensive economic security. We need to prioritize building a pipeline both in the education of power electronics workers and in manufacturing for sophisticated power electronics. We should also encourage competition in the space to foster a less concentrated supply chain.

Expand the CHIPS Act’s aperture. Wolfspeed’s $750 million is a start. GlobalFoundries’ November 2025 partnership with Navitas Semiconductor to manufacture GaN in Burlington, Vermont, represents progress. But the CHIPS Act’s attention has been overwhelmingly focused on leading-edge logic chips. Power semiconductors and wide-bandgap materials need dedicated attention within the existing incentive structure.

This change in structure is not because they are more important than AI chips; it’s because they serve a fundamentally different and equally critical national security function. Also, as power is a major bottleneck to AI development, the power grid supply chain is in many ways the AI supply chain. This doesn’t necessarily mean that every critical industry needs its own CHIPS Act, but we need to have a more generalized approach to economic security that can systematically handle different strategic industries according to their needs.

Accelerate allied-nation gallium diversification. The Minerals Security Partnership provides the framework. India, Australia, Canada, and European producers all have the potential to expand gallium recovery from aluminum production byproducts. Broadly, we should recognize our strengths and weaknesses in the production of metals and rely on partners where needed. After a decade of trying to rebuild the American steel industry, it may be useful to have a plan B. DOE has announced its intent to issue funding opportunities for gallium processing technologies, but progress has been slow. The pace of action needs to match the pace of escalation. Currently, we lag.

Consider strategic stockpiling. The arguments for stockpiling gallium, rare earth elements, and potentially SiC substrates parallel the arguments for the Strategic Petroleum Reserve. Stockpile materials where supply disruption could have cascading effects on critical infrastructure. Recent actions to set a price floor for critical minerals are a step in the right direction. However, efforts need to be significantly more focused to prevent investments that spend too much to spread money too thinly.

Decrease mining lead times. The US should embrace mining of critical minerals where it makes economic sense to do so and a market exists. These mines will have spillovers for minerals where mining is currently impractical but would become economical in a scenario where Sino-US relations fully break down. The US should aim to streamline mining approval and get closer to China in mine lead time.

Create a Unified Set of Rules for Mining. Labor and land will always be more expensive in the US compared to developing countries. However, the US has significant capital advantages in many tools that promote mining. Many of the advantages developing countries have in mining come from poor labor and environmental practices. The US should use its formidable domestic market and work with its allies to create terms of trade that ensure that minimum standards for labor and environmental protection are met up and down the supply chain. This includes the utilization of tools similar to the carbon border adjustment mechanism and the Dodd-Frank regulations on conflict minerals.

Close the analytical gap. The United States needs an integrated assessment combining DOE’s materials expertise, Commerce’s trade analysis capability, and the national security community’s threat assessment frameworks. Integrated assessments can help in examining the grid equipment supply chain with the same rigor that the rest of the semiconductor supply chain now receives. We should also redevelop the leadership we once had in power electronics and critical minerals research.

Promote the development of well-designed markets for semiconductors. Markets prone to supercycles have inherent challenges, particularly during large secular investment booms like the present AI race. However, thoughtful market design, instruments for demand smoothing, and financial risk management tools have been shown to dampen the effects of supercycles. The semiconductor market broadly needs mechanisms to create more stable investment cycles like have been developed for certain other critical commodities.

Invest throughout the Supply Chain. If we want a strong power electronics ecosystem, we need to have demand for the outputs. Part of this demand will certainly come from data centers, but a broader increase in investment in energy technologies will provide a major boost to a US power electronics ecosystem and a significant investment signal.

It should be noted that none of these pieces of advice involves nationalizing the industry or providing massive subsidies. Capitalism can get most of the important work done here, but government does need to participate in providing support for the market.

The public conversation about chips evolved from “we need more fabs” to a sophisticated understanding of chokepoints, leverage, and strategic competition. Grid equipment and power electronics need to make the same transition. The transformer meme is where awareness starts, but the real question is not whether we can get transformers. It’s whether the United States can secure the supply chains for the more complex, more geopolitically exposed technologies that the grid of the future will require.

I’m continually impressed with the depth of research and quality of the analysis you all put out. This was very informative and interesting.

“So critical. Important minerals. Very wow.” Excellent overview of the fundamental rate-limitations and what is causing them. Spamming the re-stack button ;)