China’s SME Industrial Policy in 5 Charts

How much is Beijing spending?

Arrian Ebrahimi is a J.D. candidate at Georgetown Law and a former Yenching Scholar at Peking University. Today, he’ll attempt to quantify China’s state equity investments in semiconductor manufacturing equipment. You can read more of Arrian’s writing on the excellent Chip Capitols Substack. Special thanks to Lily Ottinger for assisting with the charts.

The recent tariff chaos — first exempting only the most advanced semiconductors, then exempting a broad base of electronics important, followed by the current waiting period for more calculated semiconductor tariffs — should not come as a surprise.

Not only was the President sounding a clarion call for tariffs through the 2024 campaign, but rumors were circulating in Washington and foreign capitals that the then-candidate Trump’s tariff wishes would manifest as a tariff on the Chinese semiconductor content of downstream electronics imported into the U.S. A New York Times article recently confirmed those rumors by unnamed administration sources.

Targeting the Chinese chip content of electronics reflects a concern over the PRC’s semiconductor industrial policy that is not unique to President Trump, nor even to U.S. policymakers. European policymakers have also sounded the alarm over China’s allegedly subsidy-induced mature node overcapacity, and your author spoke at a European Commission event in Brussels last November to address just those concerns.

Washington and Brussels’ concerns, however, sound as they grasp in the dark for answers to one as-yet unanswered question: How much public money is the Chinese government spending on semiconductors… total?

Many studies over the past half-decade have tried to figure out how public funds flow from the various organs of the Chinese government to the semiconductor sector. However, the use of conservative methodologies has prevented scholars from uncovering numbers for the entire ecosystem. The two standard approaches are:

Policy Announcement Hunting: China-watching platforms have tried compiling announcements of new semiconductor incentive schemes from China’s central and local governments (see Chip Capitols here on local government programs and here on central government tax subsidies). These program compilations help explain what sorts of policy tools the Chinese government deploys, but they cannot provide even a ballpark number for the total amount of RMB invested, because the Chinese government does not have transparency standards for public expenditures in the way the U.S. does.

Public Company Calculations: The OECD’s seminal 2019 report on market distortions in the semiconductor industry examined the subsidies that governments around the world, including China, gave to their champions. However, the study limited itself to 21 publicly listed firms, only 2 of which were Chinese, because private companies do not have annual financial filings from which they could pull statistics on state investments and subsidies. This approach offers greater accuracy, but only captures a small slice of the Chinese public investment pie.

I set out to compile data as comprehensively as possible on Chinese equity investments, subsidy grants, and tax credits for the country's key semiconductor manufacturing equipment (SME) companies — regardless of whether they are public or private. This challenge required estimation based on the limited public statistics available for private companies, but has allowed me to amass a treasure trove of insights about the Chinese SME sector.

Estimation is critical for reaching conclusions about the macro-state of upstream Chinese chipmaking equipment firms. The SME sector is small — relatively few firms are publicly listed, and some of the most important firms, like Shanghai Micro Electronics Equipment (上海微电子) (China’s only lithography firm), are notably absent from public markets. At the other end of the spectrum, Huawei has increasingly sought to integrate itself vertically by investing in Shenzhen’s SiCarrier (深圳市新凯来技术有限公司), but public numbers are not available about that nascent company which is yet to release most of its products to the open market. Notably, Huawei does not count among the top investors of any of the public SME firms surveyed in this article, suggesting its SME investments are focused nearly exclusively on firms like SiCarrier that haven’t attracted attention from the state-backed Big Fund or institutional private investors.

Ass more Chinese SME firms go public and their financial details become available, I will invariably need to revise these findings. Nonetheless, the world deserves a first (if fuzzy) glance at the totality of China’s industrial policy for chipmaking equipment. In this first of two articles, we find that:

Government and private-sector investments into SME firms dropped precipitously in 2022, the year of China’s COVID lockdowns, and only recovered slightly in 2023 in the wake of the U.S.’s October 2022 export controls.

Beijing’s investment decisions have no correlation, positively or negatively, with SOE investment decisions. Their choices of which SME firms to invest in and when to invest are entirely disjointed.

The amount of liquidity created for companies via subsidies is much smaller than the liquidity the PRC government creates via equity investments. In 2021, subsidies stood at 27% of investments, in 2022 at 31%, and in 2023 at 28%.

Within the subsidy bucket, tax credits have fallen sharply as a tool of industrial policy, and politically maleable grants have come to occupy the majority of China’s subsidy tools.

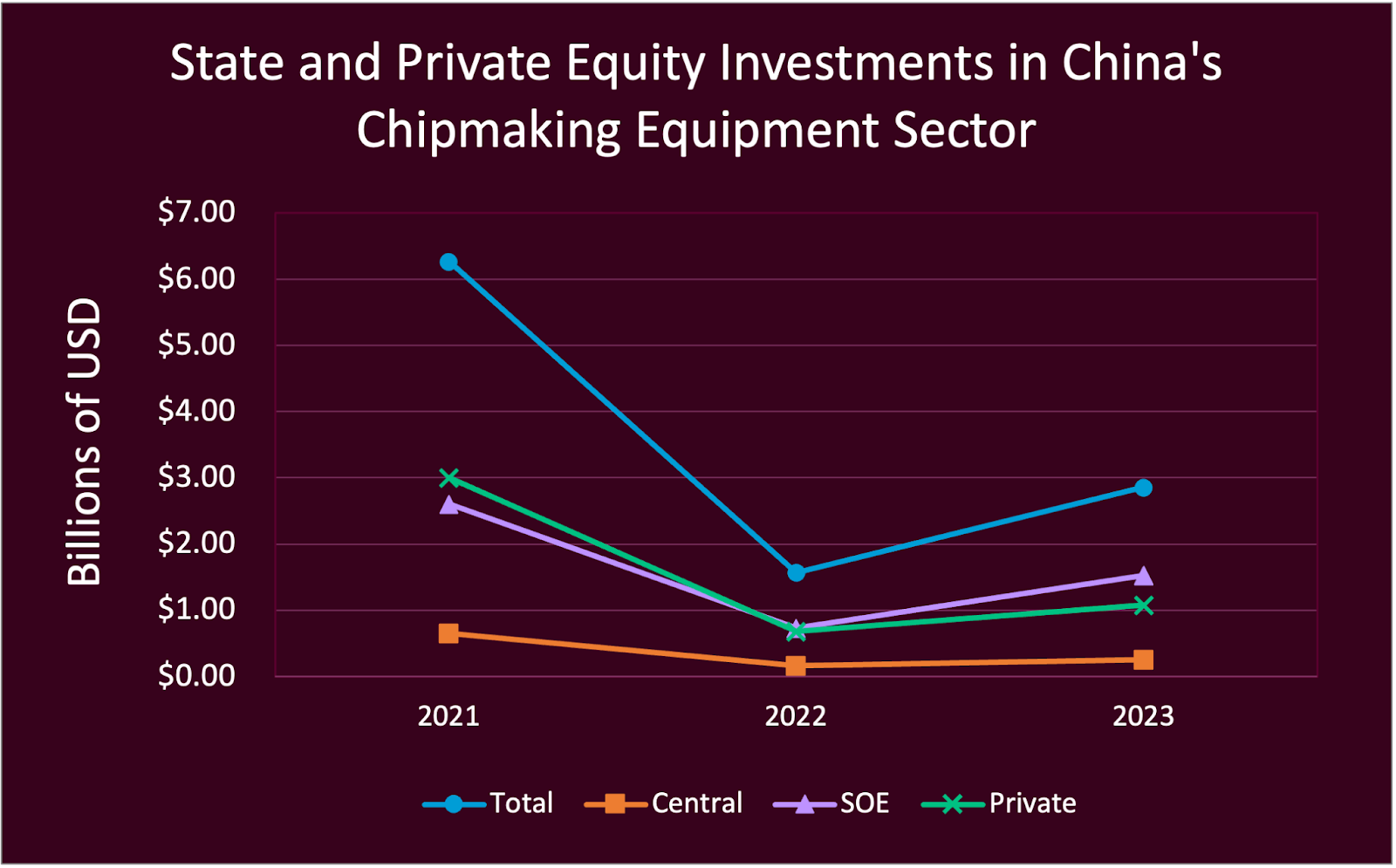

Billions of Pandemic-Sensitive Dollars

China’s investment in SME firms peaked in 2021 at $6.27 billion (a figure that includes investments by the central government, state-owned enterprises (SOEs), and private entities). Investment then fell to a trough of $1.57 billion in 2022 during the height of China’s COVID-19 pandemic. By 2023, investment rebounded to $2.86 billion — less than half of the 2021 figure.

Although COVID-19 first spread in China in late 2019, stringent lockdown policies kept the country functioning mostly as normal until stronger strains forced policymakers to adopt a “Dynamic Zero-COVID” policy in 2022 that wreaked havoc on the country’s economy. (Your author first landed in China at the height of the Zero-COVID era in fall 2022 and remembers getting his nose swabbed every day.)

Around this time, local governments poured inordinate amounts of money into COVID testing programs and quarantine hotels, leaving the localities strapped for cash more broadly. The sharp dip in semiconductor investments in 2022 likely reflects across-the-board belt-tightening during that difficult year. This chart only categorizes investors into SME firms as those of (1) the central government (namely the Big Funds run as independent corporations with the Finance Ministry as lead investor), (2) SOEs (including state-owned banks), and (3) private (including all foreign) investors. As a result, the chart cannot isolate investments from local governments to see if the decline was also due to non-COVID-related trends in 2022. However, given the interlocking ownership by local governments and the central government of the largest SOEs, it is likely that the decline in SOE investments from $2.61 billion in 2021 to $0.73 billion in 2022 reflects local governments’ COVID-induced financial constraints.

It is less likely that the decline in central government investments from $0.65 billion in 2021 to $0.16 billion in 2022 was due to COVID. The only mechanism of central government investment this research identified was the (at the time) two iterations of China’s Big Fund (大基金). As a reminder for newer readers:

The first phase of the "Big Fund" raised 139 billion yuan ($20 billion) and invested in 23 companies across the chip industry from September 2014 to May 2018. There were 16 shareholders in the first phase of the Big Fund, among which the Ministry of Finance accounted for the largest share at 36.47%. Among projects receiving investment, chip manufacturing accounted for 67%, chip design 17%, packaging and testing 10%, and SMEs/materials 6%.

The Big Fund’s second phase was established in October 2019, aiming to raise 201 billion yuan ($29 billion). Besides government and SOE contributors, some private companies also joined the round, but the Ministry of Finance still accounted for the largest share at 11.02%. As of March 2022, the second phase fund had announced 79 billion yuan ($11 billion) in investments in 38 companies, with 10% for design, 2.6% for packaging and testing, and 10% for equipment/materials.

Because the Big Fund investments were arranged in advance, it is more likely that the dip in investments in 2022 was coincidental, rather than due to COVID-induced restraint.

Beijing and SOEs Not in Sync

Whenever a communist country releases its 5-year or 10-year plan, Washington takes a collective gasp. These fears assume that countries like China function like centrally controlled monoliths, where policymakers in Beijing can command and control every yuan spent across its vast territory —or at least, every government yuan.

However, the idiom 山高皇帝远 (“mountains are high, and the emperor is far”) tells a different story — it is not easy to centrally manage a country as vast and diverse as China. Government actors like state-owned enterprises (SOEs) and local governments operate with their own parochial interests in mind, and Beijing cannot always afford the political capital required to bring SOEs and local governments in line with national-level industrial policy goals.

If China’s central policymakers in Zhongnanhai (中南海) and the cadres leading SOEs were politically in sync, I hypothesized that investments by the central government into SME firms would be followed by a commensurate bump in investments by SOEs into the same firms.

For each SME company receiving investments from China’s Big Funds (大基金) in 2021, 2022, and 2023, I examined the three-month periods following investments by the Big Funds to search for such a bump in SOE investment interest:

First, I defined a “Pre-Central Stock Purchase” number as the share of total investments in each calendar year from SOE investors. This number gave me a baseline of how interested SOEs were in each particular SME firm in a given year.

Second, I defined a “Post-Central Stock Purchase” number as the share of total investments from SOEs in the three months following each company’s receipt of Big Fund investments. This number served to show what the short-term reaction by SOE investors was to demonstrated interest in an SME firm by the central government.

Lastly, I averaged out the “Pre-” and “Post-” numbers across all SME firms getting Big Fund investments to get each year’s SOE investment baseline and average post-Big Fund SOE investment bump.

The results show that investments by the central government’s Big Fund have no consistent correlation with SOE investment decisions. In 2022, there was a 25% decline in the share of total investments made by SOEs in the three months following Big Fund investments. In 2022, there was an 8% increase in SOE investments. And in 2023, the correlation was again negative at an 11% decline.

This inconsistency bears out on an individual company level, too: Naura (北方华创), for example, saw its SOE investments drop every year following central government investments. Tianshui Huatian (天水华天) saw increases in 2021 and 2022 and a slight decrease in 2023. Meanwhile, Piotech (拓荆科技) saw virtually no change to its SOE investments in any of the three years.

Beyond showing that central government investments do not affirmatively signal to SOEs that they should invest more or less in particular SME firms, these statistics show that central government investments do not signal anything to SOE investors.

An alternative explanation to the inconsistent investments received by companies above could be that the central government does in fact direct SOE investments behind closed doors, but just gives different investment instructions each year. Perhaps the central government is pursuing a deliberate substitution strategy, directing SOEs to invest in firms that haven’t already received central government funds, except in years of extreme financial hardship, like 2022.

If this theory were true, we would see SOEs making investment decisions in lockstep, which is not what the data suggests. To demonstrate investment disunity among SOEs, we look to the example of AMEC (中微公司), which is among the most important SME companies in the Big Fund’s investment portfolio. Out of 11 three-month periods following shifts in the central government’s investment stake in AMEC, SOE investors only responded uniformly (either buying or selling AMEC stock) in four cases — that is, they were aligned only 36% of the time.

(In the graph above, 1 represents all SOEs buying stock in the three month period following a central government investment; 0 represents SOEs selling stock for that time period; and 0.5 represents half of SOEs buying and half selling.)

For SME companies other than AMEC, there is a similar lack of cohesion. It is therefore unlikely that central policymakers were successfully orchestrating any unified strategy for SOE investment.

There appears to be no consistent correlation, positive or negative, between investment decisions by the central government in Beijing and those by the quasi-governmental SOEs spread throughout the country. The mountains are indeed tall, and the emperor is far.

Subsidies: Smaller Than Expected and Falling

Discussions around China’s industrial policy regularly talk about “subsidies” without really knowing what that means. Absolutely, the PRC government has been offering immense support to its domestic chip sector, but how has it offered this support? Through subsidies? Through state equity investments? More importantly, what does the answer to that question mean politically?

I define subsidies as comprising tax credits and direct financial grants that the Chinese central and local governments provide to semiconductor manufacturing equipment (SME) and chip manufacturing companies, while equity investments are purchases of firms’ newly issued stock to help them generate liquidity. Both are forms of industrial policy support for SME and chipmaking companies, but China’s choice between these policy tools suggests different levels of central government coordination about which companies receive help.

At their height in 2021, upstream SME firms received $0.87 billion from PRC government actors in subsidies (tax credits and grants), while they received $3.26 billion from government actors in equity investments. SME subsidies were also less than equity investments throughout the COVID lockdowns, at $0.28 billion and $0.89 billion respectively in 2022. Then, after the pandemic, both policy tools rebounded to $0.50 billion and $1.78 billion in 2023, though they remained well below their 2021 highs.

Another look at the graph above tells a story about how upstream SME firms benefit differently from subsidies than downstream chipmakers. The smaller scale of subsidies to SME firms (in orange) is not surprising, since SME firms are smaller compared to the firms in China’s much more mature chipmaking sector. The PRC SME sector is largely comprised of small (often private) companies, with the two largest among them, AMEC (中微公司) and SMEE (上海微电子), posting operating profits of only under $0.20 billion at their peak in 2022. In contrast, the downstream chipmaking sector boasts giants like SMIC (中芯国际), which posted over $2 billion in profit in that same year.

Given that tax credits are calculated proportionately to companies’ operating profits, it is no surprise that upstream SMEs would receive a smaller amount of overall subsidies than their downstream counterparts. What is interesting, however, is that upstream subsidies fell precipitously from 2021 to 2022 during the COVID lockdowns, while downstream subsidies fell only slightly. Then, after the pandemic, upstream SME subsidies recovered about half their lost value, while subsidies to downstream chipmakers continued to fall gradually.

At first glance, these trends suggest that SMEs are becoming a larger target of China’s subsidy efforts compared to downstream chipmakers. To confirm this political observation, however, we will need to dive deeper into the relative share of tax credits and grants within the figures for subsidies overall. Tax credits are a relatively apolitical tool once passed because they apply mechanically to any company that satisfies certain statutory requirements, while grants are allocated on a case-by-case basis and thus react quickly to political trends. These questions are explored in the next section.

The Fall of Tax Credits and Revival of Grants

Tax credits and grants are fundamentally different subsidy tools. Governments can exercise maximum discretion with their grant allocations because they are awarded on a case-by-case basis. In addition to the overall grant numbers in the financial disclosures from which I draw my data, many companies also list the individual sources of their grant awards. For example, Naura received a total of 121.7 million RMB in subsidies in 2022, of which 30.2 million RMB came from the Beijing Municipal Party Committee Office Project (北京市委办局项目). When a grant is a relatively small proportion of a company’s total, government entities can withhold it without fearing that the recipient will be utterly destroyed.

In contrast, tax credits are given out mechanically to companies that fit the credits’ qualifications. The central government’s largest tax credit is a 15% income tax deduction for companies designated under the Management Measures for the Recognition of High Tech Enterprises program (高新技术企业认定管理办法). Certainly, it is a political decision by the PRC Ministry of Finance whether to qualify companies for a tax credit (see here for an article I wrote in The Diplomat describing China’s tax credits). But tax credit qualification is a stickier (and thus more financially consequential) decision than individual grant awards, so government actors are more hesitant to use the blunt cudgel of tax credits in reaction to moderate changes in political priorities. Subsidies, rather, are the scalpel best suited for reacting to modest political shifts.

Some interesting trends emerge in the three-year period covered by my analysis. Even though the PRC released ever larger R&D tax credits over the past few years, the amount of tax credits China has provided to the chip sector has fallen since 2021. In part, this could imply that firms’ profits declined over this period, thereby decreasing the size of their tax obligations and thus making tax credits appear less valuable.

However, the graph above demonstrates that operating profits did not decline in 2022 for the companies I studied, contrary to the decline in tax credits. This suggests that a policy shift in 2022 reduced total tax credits, even as the income tax credit stayed stable and the R&D tax credit increased.1

The other trend that becomes apparent is the oscillation of grant numbers (see the first graph in this section). 2022 saw a sharp fall in the value of subsidies apportioned via grants because of COVID-induced financial strain. Since grants can be given or withheld relatively flexibly, there was a sharp decline as soon as local governments reprioritized their resources to pandemic-prevention activities.

In 2023, the value of grants recovered while tax credits continued to fall. Knowing that the PRC chip industry’s operating profits also fell in 2023, the rise of grants that year suggests that government actors are not simply doling out support to profitable companies in their jurisdictions, but rather to companies that are a political priority. This does not mean that local governments’ choice of which chip companies to subsidize overlaps with central government priorities (the second chart in this article about lack of central government-SOE coordination in investment suggests otherwise), but the political prioritization of the chip industry as a whole does seem to withstand the sector’s economic struggles.

Methodology — Equity Investments

I analyzed the following companies for this article on equity investments. The scope of firms selected comprises (1) all of those known to have received investments from either of the first two Big Funds, as well as (2) those with the most advanced domestic technology in China in the following equipment areas: lithography, etching, deposition, implantation, epitaxy, and metrology.

Despite your author’s greatest efforts, I could not collect enough data about the not-publicly listed Shanghai Micro Electronics Equipment (SMEE) to speak confidently about its equity investments; however, subsequent charts about China’s subsidy grants and tax credits will include estimations of how SMEE benefited from those policy tools.

Firms analyzed:

中微公司|Advanced Micro-Fabrication Equipment Inc. China

北方华创|NAURA Technology Group Co., Ltd.

拓荆科技|Piotech Inc.

天水华天|Tianshui Huatian Technology Co.,Ltd.

长川科技|Hangzhou Changchuan Technology Co., Ltd.

芯源微|KINGSEMI Co., Ltd.

盛美上海|ACM Research (Shanghai) , Inc.

中科飞测|Skyverse Technology Co., Ltd.

华峰测控|Beijing Huafeng Test and Control Technology Co., Ltd.

华海清科|Hwatsing Technology Co., Ltd.

新益昌|Shenzhen Xinyichang Technology Co., Ltd.

屹唐半导体|Beijing E-Town Semiconductor Technology Co., Ltd.

北京烁科中科信|Beijing Zhongkexin Electronics Equipment Co., Ltd.

凯世通|Shanghai Kingstone Semiconductor Corp

浙江镨芯(万业企业)|Zhejiang Praseodymium Core Electronic Technology Co., Ltd.

至微半导体|Not certain about English name: Zhiwei Semiconductor

沛顿存储|Payton Technology(Shenzhen) Co., Ltd.

东科半导体|Dongke Semiconductor Wuxi Co., Ltd.

精测半导体|Shanghai Precision Measurement Semiconductor Technology,Inc.

睿励科学仪器(上海)有限公司|Ruili Scientific Instruments (Shanghai) Co., Ltd.

东方晶源|Dongfang Jingyuan Electron Limited

合顿科技|Hefei Payton Storage Technology Co., Ltd.

For public companies on the list, I identified their top ten equity holders (central government, SOEs, and private) per quarter from Wind (万得), a site similar to Bloomberg that aggregates financial data on public companies. I then calculated each investor’s quarterly change in position to determine how many of each company’s stocks changed hands per quarter. Then, I calculated how many new stocks each firm issued per year to determine how much new liquidity these investors provided each firm through their stock purchases. That “new liquidity” is the measure of support via equity investments.

For private companies on the list, I found public reporting on their investing rounds and categorized investors into the same three buckets (central government, SOEs, and private) as for public firms.

Methodology — Subsidies

Getting subsidy data for SME companies posed similar challenges as equity investments in that many of these firms are small and not publicly listed. To that end, I relied on liberal estimation methods.

For upstream public companies, I sourced all my data from publicly available financial reports. For upstream private companies, I tried to find at least one publicly reported statistic in Chinese media, like revenue or operating profit for each company in each year. Then, I estimated all of each company’s other stats by assuming they were proportional with the average ratios from all public companies of the same year. (For example, Shanghai Microelectronics Equipment 上海微电子was not public in 2022, but I found a report of its operating profit, which was 1.2 billion yuan. Therefore, I estimated its "statutory tax obligation" as 1.2 billion/[the average operating profits of public companies in 2022]*[the average statutory tax obligations of public companies in 2022].) This method is not accurate at the individual company level (some estimates even resulted in negative tax credits); however, it results in a reliable estimate in aggregate. More importantly, it provides macro-level insights about China’s SME subsidies that, though imperfect, can help Western government policymakers get a grasp on how much China is spending to catch up in SMEs.

Additionally, it was not enough to look only at SME companies’ financials to get a grasp of China’s countrywide support for these firms because China also subsidizes demand for semiconductor tools when it gives subsidies to the purchasers of these tools, i.e. downstream chipmakers. To that end, I examined downstream companies to estimate the “subsidized demand” for SMEs—i.e., the portion of subsidies received by downstream chipmakers that is used to purchase SMEs. I estimated the subsidized demand for each downstream company as [sum of subsidies]x[capex]/[total expenditures]. I got the underlying numbers for this section similarly as for upstream SME companies, but since most downstream chipmakers are public, I only needed to use media statistics–based estimations for two firms.

Upstream SME companies surveyed:

Advanced Micro-Fabrication Equipment Inc. China(中微公司)

Naura(北方华创)

Yitang Semiconductor(屹唐半导体)

Piotech Inc.(沈阳拓荆)

Skyverse Technology Co., Ltd.(中科飞测)

Shanghai Precision Measurement Semiconductor Technology, Inc.(上海精测半导体技术有限公司)

Shanghai Microelectronics Equipment(上海微电子)

Cetc Electronics Equipment Group Co., Ltd.(中电科电子装备集团有限公司)

Beijing Semicore Electronics Equipment Co., Ltd.(北京烁科中科信电子装备)

Shanghai Kingstone Semiconductor Corp(上海凯世通半导体股份有限公司)

RSIC Scientific Instrument (Shanghai) Co., Ltd.(睿励科学仪器(上海)有限公司)

Downstream chipmakers surveyed:

SMIC(中芯国际)

Guoxin Micro (紫光国芯)

AllwinnerTechnology (全志科技)

Changsha Jingjia Microelectronics (景嘉微)

Nations Technologies (国民技术)

Orbit (欧比特) (航宇微)

Shenzhen Goodix Technology (汇顶科技)

Datang Telecom Technology (大唐电信)

Ingenic Semiconductor (北京君正)

Hangzhou Silan Microelectronics (士兰微)

Sino Wealth Electronic (中颖电子)

Qingdao Eastsoft Communication Technology (东软载波)

GigaDevice Semiconductor (兆易创新)

Beijing Philisense Technology (飞利信)

Ninestar (纳思达)

Shenzhen Kaifa Technology (深科技)

Hua Hong Semiconductor (华虹半导体)

My tax credit numbers look at the actual differences in the statutory tax obligation that a company owes and the amount that it actually pays to calculate tax credits, so it captures the effect of all credits at play. Perhaps some of these distortions are due to deferred tax payments, which the current version of this research does not account for.

| A guest post by

|

Awesome research. This line really stood out: “Discussions around China’s industrial policy regularly talk about “subsidies” without really knowing what that means.” Would be interested in a similar analysis of defense industry (or some subsection, like those involved in drones or hypersonic capabilities.) My own Substack covers some firms involved in PLA C4ISR systems. https://ordersandobservations.substack.com

Pretty shocking how little subsidies the SMEs actually received. In comparison, Biden gave out, what, 65 billion for rural internet?

Am I understanding this right?