Critical Mineral Security: The Endgame

a policy framework for derisking success

Farrell Gregory is a non-resident fellow at the Foundation for American Innovation. This essay is the final winner of our economic security essay contest!

After fifteen years of bipartisan attention, countless executive orders, and tens of billions in appropriated and authorized funding, the United States remains overwhelmingly reliant on China for the critical minerals. In some cases, that reliance has increased. Over that same period, foreign interference in critical mineral supply chains has moved from a hypothetical to a regular occurrence.

China’s willingness to use its supply chains as leverage became undeniable when rare earth exports to Japan were cut in 2010 over competing island claims. America had more than a decade to prepare for the PRC’s first direct controls on exports to the U.S. But when China placed export controls on gallium and germanium in late 2023, the United States effectively had domestic alternatives. When the PRC later limited graphite and antimony exports, prices for both materials spiked and threatened supply chains for a wide range of products, from weapons to EVs. Then, when rare earth restrictions hit in 2025, American manufacturers still couldn’t find alternatives, and in some cases were forced to shut down production. Even after a bilateral agreement to lift those restrictions, firms are still suffering from yttrium and scandium shortage. In comparison, there is no shortage of interest in critical minerals; they seem to be invoked to justify countless public policies or acts of diplomacy. But despite this interest, American supply chains remain tangled up in China, which is increasingly willing to strangle them to achieve concessions. Why?

We remain reliant on China because U.S. critical mineral policy has recently taken a categorical approach, rather than prioritized strategy. These policies treated critical minerals as an undifferentiated category, deploying uniform benefits that apply equally across a wide range of materials regardless of their varying exposure and likelihood for interference.

Since the United States Geological Survey list was established in 2018, it has grown from 35 to 50 to 60 materials, with many of those latter materials marginally exposed to China. Because the USGS list is the reference point established by the 2020 ENERGY Act and cited as a definition by many subsequent federal and state laws, broadening the list affects policy and dilutes any categorical benefits across a wider list of critical minerals. Because these categorical benefits do not distinguish between the relative criticality of different materials, they offer benefits to the most consequential and insignificant minerals alike.

What is needed instead is a shorter list that prioritizes materials for targeted investment, defined by proven Chinese ability and willingness to interfere with those specific supply chains, as well as the possibility for government support to make a meaningful difference in the short term. This prioritized list translates into quantifiable KPIs that can be used to measure our success in decreasing reliance on China. America should be well past the point of treating critical mineral risk as a hypothetical–the Chinese certainly are. Our policy should reflect this reality by concentrating active government support for the few materials where China has imposed export controls.

Establishing the Basis for Prioritization

Examining the relative criticality of the materials on the USGS list proves which items China is interfering with–and which we should prioritize, as a result.

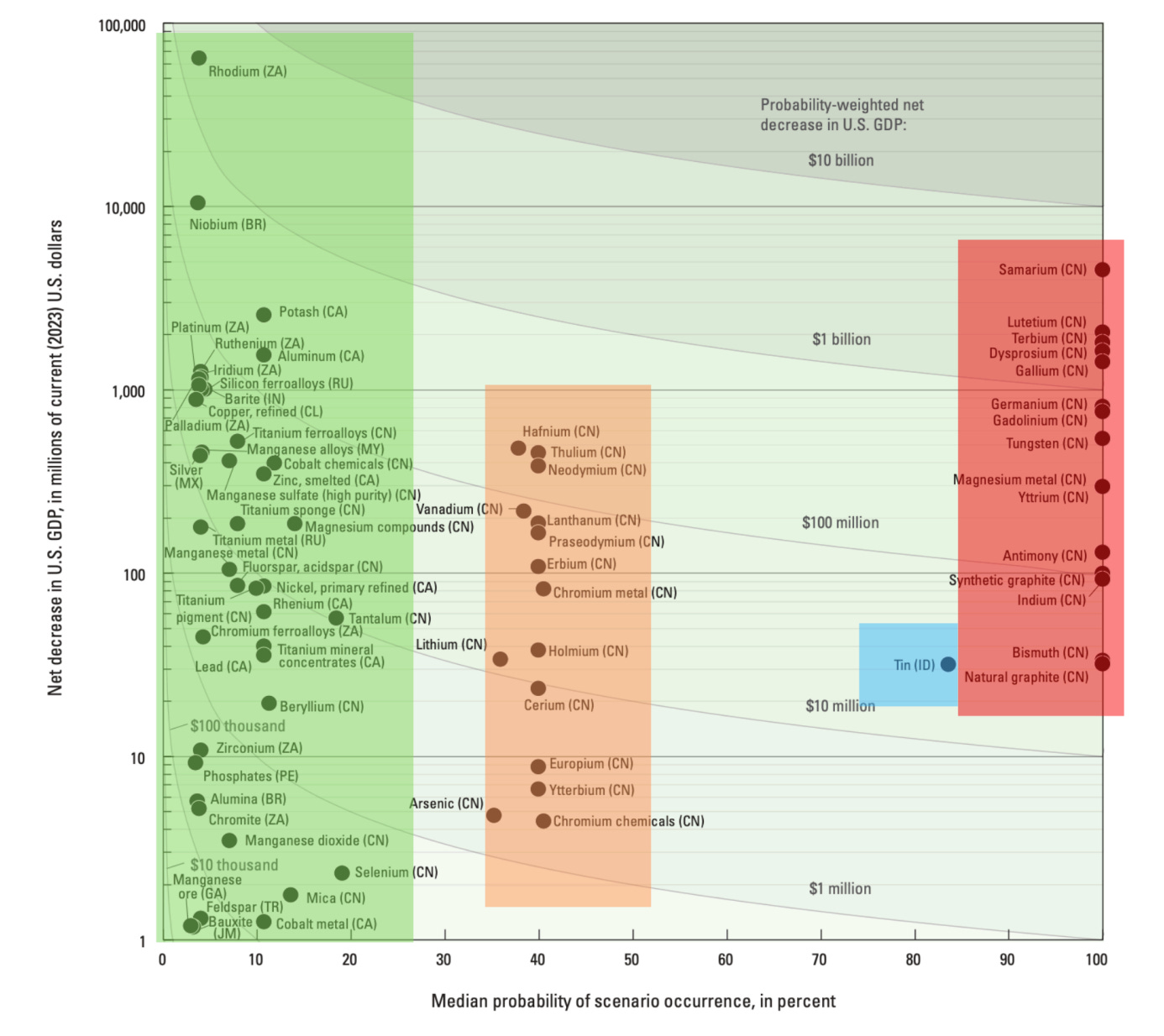

In its mandated three-year update to the list, USGS economists modeled the probability-weighted economic impact of supply disruptions for 84 mineral commodities, including the 60 that the list now included. They estimated both the GDP consequences of disruption and the likelihood that disruption would occur, combining these into a single risk-adjusted metric. The results are striking in their concentration. A small number of materials account for the overwhelming majority of economic risk. The rest contribute only somewhat or marginally.

The disparity is visible in the above graph. Plotting probability-weighted GDP impact against likelihood of disruption reveals a distinct cluster of high-consequence, high-probability materials in the upper right quadrant (highlighted in red). These are almost exclusively materials where China dominates production and has demonstrated willingness to restrict exports. Next to this is Tin (in blue), where the U.S. is highly reliant on a non-China supply chain. A grouping (highlighted in orange) is largely made up of light rare earth elements, alongside chromium metals and chemicals. Finally, a much larger group of materials (highlighted in green) clusters near the origin, with near-zero disruption probability. For these materials, the U.S. is primarily reliant on non-China supply chains; while our relationships with these countries may vary, not one is an active manipulator of critical supply chains like China.

A priority list that responds to Chinese restrictions would consist of exactly twenty five materials, drawing from both the red and orange highlights: sixteen rare earth elements and nine other minerals.

Most notable are the rare earths: seven light rare earth elements (lanthanum, cerium, praseodymium, neodymium, samarium, europium, and gadolinium) and nine heavy rare earth elements (terbium, dysprosium, holmium, erbium, thulium, ytterbium, lutetium, yttrium, and scandium). The light/heavy distinction tends to follow the chemical properties of each element. These materials enable permanent magnets for defense systems, electric vehicles, and wind turbines, and countless other essential applications. China controls 99 percent of heavy rare earth production, a figure reflecting geological constraints as much as industrial policy. The case for light rare earth elements is more favorable for the U.S.

I group all rare earth elements together on this priority list for several reasons, though there are meaningful differences between heavy and light rare earth elements in both geology and supply chain dynamics. First, while heavy rare earth elements have so-far been the target of Chinese interference, these elements all naturally occur together. Whether a deposit is feasible for heavy rare earth extraction is dependent on its relative concentration of heavy and light rare earths. Second, while China is a near-monopoly provider of heavy rare earths and still a major producer of light rare earth elements, meaning that many supply chains, especially for magnets, run through the PRC. Finally, the usage of heavy rare earth elements in permanent magnets isn’t entirely separate from light rare earths. Neodymium, for instance, is used alongside dysprosium in neodymium iron boron (NdFeB) magnets.

Specific geological facts will necessitate somewhat different supply chains for heavy and light rare earth elements. But it is ultimately in the interest of the U.S. to support finding ex-China sources for both types, as well as develop magnet-producing capacity that utilizes both. So, even though China has not yet imposed export controls on most light rare earth elements, all rare earth elements should be considered high priority.

From here, the priority list turns to non-REE materials that have been targeted by Chinese export controls in recent years.

Gallium and germanium were the first materials subject to China’s current export control campaign, restricted in August 2023. Both are essential to semiconductors: gallium in the form of gallium arsenide and gallium nitride is used to manufacture integrated circuits and optoelectronic devices; germanium is used in fiber optics, infrared optics for night vision systems, and multijunction solar cells. Both are byproducts of other refining processes: gallium from aluminum, germanium from zinc. China produces 98 percent of global gallium and approximately 60 percent of global germanium. The United States is 100 percent net import reliant for gallium, but only 19 percent of US consumption comes directly from Chinese imports; the rest comes from Japan, Germany, and Canada—countries that themselves depend on Chinese feedstock. For germanium, net import reliance exceeds 50 percent, with Belgium supplying 41 percent of US imports and China 23 percent directly. Belgium’s refining operations, however, rely substantially on Chinese raw material.

Tungsten, restricted by China in 2025, is essential for cutting tools, aerospace alloys, and armor-piercing ammunition. China produces 82 percent of global supply. The United States is more than 50 percent net import reliant, with China supplying 26 percent of imports directly—but as with gallium, global production concentration means alternative suppliers have limited capacity to scale.

Magnesium metal is perhaps the most acute near-term vulnerability. China produces 90 percent of global supply for primary magnesium. The sole American smelter filed for bankruptcy in September 2025 after years of diminished production. The United States is now more than 75 percent import-dependent, with Israel and Canada as leading sources—but both have limited capacity relative to Chinese dominance of global production, which allows it to play an outsized role in influencing prices. While China has not yet constrained primary magnesium supply, China introduced export controls in 2025 for a number of magnesium alloys, which caused USGS to list it as a material with high likelihood for Chinese disruption.

Antimony, restricted by China in August 2024 and subject to a full export ban to the United States in December 2024, is used in flame retardants, lead-acid batteries, and ammunition. The United States is 91 percent net import reliant, with 54 percent of US consumption coming directly from Chinese imports—one of the highest direct dependencies among critical minerals. China accounts for 48 percent of global mine production. There had been no significant domestic antimony mine production since 2001.

Indium, a material used in flat-panel displays, touchscreens, and certain semiconductors and restricted by China in February 2025. The United States is 100 percent net import reliant, but only 12 percent of consumption comes directly from China; leading sources are South Korea (25 percent) and Japan (22 percent). Despite the lack of direct U.S. purchases from China, it remains a major source of indium for other countries that we rely on, such as Japan and South Korea, since China produces 70 percent of the global total.

Natural graphite, restricted by China in late 2023, is essential for battery anodes, fuel cells, and lubricants. The United States is 100 percent net import reliant, with 43 percent of consumption coming directly from Chinese imports. China produces 77 percent of global supply. Synthetic graphite, also under Chinese export controls, faces even greater concentration: China produces 97 percent of global supply. Domestic graphite projects are advancing in New York and Alabama, but battery qualification timelines require three to five years before new supply reaches manufacturers.

Bismuth, also restricted by China in February 2025, is used in pharmaceuticals, metallurgy, and atomic research. The United States is 92 percent net import reliant, with 60 percent of consumption coming directly from Chinese imports—the highest direct China dependence among the non-rare-earth minerals under export control.

Each has been subject to Chinese export controls implemented between 2023 and 2025. Each one is part of a supply chain where Chinese dominance exceeds 50 percent. The USGS risk-adjusted list assigns each of these materials 100% likelihood of interference.

Non-Prioritized Materials

In two cases, I have left materials that USGS rates as high likelihood of Chinese restriction off the priority list. For tellurium, the report noted that the U.S. went from 95% import reliance to becoming a net exporter as a result of a new recovery operation at a Rio Tinto project in Utah. For molybdenum, China is not a relevant portion of our import profile. While China has described these two materials as restricted, American access is not meaningfully impaired. Beyond those cases, Chinese interference is the main basis of this priority list. There are a number of high-profile materials that receive substantial policy attention but that do not belong on the priority list, either because markets are too large for targeted intervention to matter or because the supply chain is not sufficiently concentrated in China.

Copper entered the critical minerals list in 2025 following a Commerce Department Section 232 investigation into unfair trade practices. The addition is defensible on supply chain grounds; Chile, Peru, and Indonesia dominate production, while China holds a substantial portion of global refining capacity. Additionally, copper demand for electrification will strain existing supply chains. However, the global copper market exceeds $270 billion annually. A multibillion-dollar price support program–as might be offered for smaller-value materials–would barely register against existing market forces. The solution for increasing American copper production is permitting, not government capital.

Potash was also among the materials the USGS methodology recommended adding to the 2025 list. The list marks it as a high risk material. But the risk originates with Canada, which supplies 79 percent of American imports. Canadian supply disruption is a trade relationship question, not a strategic threat of the sort posed by Chinese materials.

The U.S. relies on imported refined tin for 77% of its consumption. These materials come primarily from Bolivia, Peru, and Indonesia, which collectively produce 73% of America’s imports. But like South Africa and Canada, these countries have not demonstrated any willingness to weaponize their positions.

The distinction matters because America’s resources to pursue critical mineral industrial policy are finite. Assuming rightly that government-aided reshoring efforts are working with a fixed pool of capital, this means that every dollar directed toward securing phosphate rock supply is a dollar unavailable for gallium recovery or rare earth processing. Prioritization requires limiting benefits not only to areas where China is most dominant, but also to where those dollars will make an impact. Policy tools ought to be designed to address the problem, and for mineral markets that are of a certain size, it becomes impossible to use activist government tools such as price floors and offtake agreements.

From Categorial to Prioritized Critical Mineral Policy

The shortcoming of American critical minerals policy is partly a failure of prioritization and partly a failure of policy design. Even when resources have flowed toward the most consequential materials, they have often flowed through categorical instruments that treat all critical minerals identically. Adopting a critical mineral policy that prioritizes decreasing reliance on China in the short run will require identifying which policies advance that interest, and which don’t.

Both a prioritized and categorical approach are defined by two considerations. First, which critical minerals are being considered? Second, what policy support is offered to those minerals?

The categorical policy approach was overinclusive on the first count and undifferentiated on the second. From 2018 to 2025 the USGS list grew from 35, then 50, then 60 materials. But those later additions were disproportionately lower priority. Of the 25 materials added to the list since 2018, only one of those is listed as ‘high priority’ on the 2025 USGS list report: potash. Five are noted as elevated priority, seven as moderate priority, and twelve as limited priority.

This listing dilution resulted in unfocused policy. The 45X Advanced Manufacturing Production Credit exemplifies this approach. The policy was beneficial, but it failed to focus on America’s most urgent reshoring needs. Established under the Inflation Reduction Act, and using a statutory list of minerals borrowed directly from the expanded 50-item 2022 USGS list, the credit provided tradeable tax credit incentives that cover 10% of production costs for facilities producing critical minerals without distinguishing among materials by strategic significance. Now, recent legislation will phase the credit out by 2034.

The 45X credit was not unique. The critical minerals list itself functions as a categorical instrument. Inclusion on the list triggers eligibility for various programs, preferences, and authorities without distinguishing among the sixty listed materials. The Defense Production Act Title III authorities have been deployed categorically. Between 2023 and 2024, the Department of Defense invested more than $250 million through DPA III authority: supported projects included many non-priority critical materials, such as lithium and tin.

Prioritized policies work differently. Funds would only be available to the twenty five materials listed earlier. Additionally, the form of such investments would change, too. Prioritized policy would involve targeted bets on specific materials and specific companies, with further financial instruments designed to the characteristics and needs of each supply chain.

Stockpiling provides a buffer against disruption while longer-term supply chain investments solidify. The Defense Logistics Agency maintains an existing National Defense Stockpile, but it is nearly $10 billion below wartime-ready levels. Prioritized stockpiling would require more than just additional funding. Such funding must be targeted. Accumulating the materials most likely to be disrupted by further Chinese export controls would afford flexibility in a scenario where American manufacturers have lost access to Chinese exports.

Equity investments and direct loans are the most targeted approach. These instruments allow government to take positions in supply chains where private capital is insufficient or where risks are too concentrated for commercial financing. More than anything, equity investments are useful for signalling government support and priorities. Such support can attract outsized follow-on investment from the private sector.

Price floors address a distinct problem. Chinese producers, backed by state support and operating at scales American producers cannot match, can suppress global prices or survive market price swings that would render Western production uneconomic. Chinese magnesium production drove a Utah smelter into years of losses before bankruptcy. Price floors guarantee domestic producers a minimum return, insulating them from the vicissitudes of commodity pricing and creating certainty for ex-China production.

Offtake agreements commit governments or firms to purchase output from domestic producers, reducing demand risk and enabling project financing. For prioritized materials where private demand is uncertain or where qualification timelines are long, government offtake can bridge the gap.

Financing critical mineral mining and processing, whether using price floors or equity investments, is complicated. There are many more nuances than I could fit in this paper. Prioritizing certain materials is a first step, but different financing solutions should be adjusted to the needs and market dynamics of different materials.

One additional recognition underlies all of these support policies: the cost of continued reliance on China is far worse than whatever inefficiencies and expenditures exist as a result of robust government support for ex-China markets. I can understand why, in the early stages of post-2010 critical mineral policy, when supply chain interference seemed to be a hypothetical, that policymakers would rather wait to let American innovation bring these supply chains back, or try to find less expensive/wasteful ways of moving the supply chains out. But now that weaponized supply chains have moved from wargames into real life, it becomes necessary to choose between the options before us.

Putting Prioritization into Practice

Prioritization is as concerned with how to support supply chain adjustment as which minerals to support. In a prioritized framework, the job becomes matching policy to material in order to maximize China de-reliance.

For the priority set of approximately twenty five materials, I propose a straightforward measure of success: domestic and other ex-China sources should equal 100% of American consumption within a ten-year goal.

This metric is measurable with existing data. The USGS Mineral Commodity Summaries report net import reliance and import source breakdowns annually. It directly measures concentration, which is the source of leverage for China.

China has demonstrated which supply chains it considers leverage points. The export controls of 2023, 2024, and 2025 were composed of roughly twenty materials that Beijing is willing to weaponize. The USGS probability-weighted analysis confirms that these materials account for the overwhelming majority of economic risk from supply disruption. Chinese strategists and American economists have independently identified the same chokepoints. With a list of prioritized minerals, American policymakers could act before the Chinese do.

Domestic rare earth supply chains have seen the most attention in the last year, both from China and the U.S. In response to two rounds of Chinese export controls, American policymakers have put into place policies ranging from equity investments, offtake agreements, and a series of grants from DOE. While much of this investment has been focused on magnet manufacturers and producers of light rare earths, the U.S. government is clearly looking for options to develop an ex-China heavy rare earth element supply chain, such as in Brazil.

For gallium and germanium, the constraint is different. Since both are byproducts, meaning production depends on the primary commodities from which they are recovered. The United States refines aluminum and processes zinc domestically. Gallium and germanium recovery could be integrated into existing operations without new mining. The investment required is small relative to the strategic value. The case of tellurium illustrates the success that implementing recovery operations can bring.

For antimony, the picture is more encouraging. In late 2025, two domestic mines began restarting operations in Montana and Idaho, representing the first significant American antimony production in more than two decades. Supporting these projects through offtake agreements or DPA financing could reduce import reliance meaningfully within a near-term window. Antimony exemplifies a tractable near-term opportunity that targeted policy could convert into supply chain progress.

While the United States has not commercially mined tungsten since 2015, our identified 5.4 million tons of reserves are among the world’s largest. Several domestic companies retain the capability to convert concentrates into tungsten carbide and metal powder, but all feedstock is imported. The near-term opportunity lies in restarting dormant domestic mines—Colorado hosts primary molybdenum-tungsten deposits that were produced historically—while the longer-term objective is rebuilding an integrated supply chain from ore to finished carbide products.

Since late 2025, the United States has been entirely dependent on magnesium metal imports for a material essential to aluminum alloys, steel desulfurization, and aerospace components. Israel and Turkey maintain independent production from domestic resources and currently supply most US imports. But their combined capacity cannot match China’s role in the market. Rebuilding domestic smelting capacity is a multi-year undertaking, but the site—which was recently purchased by the Utah state government—creates an opening for federal acquisition or recapitalization under Defense Production Act authorities, possibly functioning with some price floor to counteract any future Chinese-led price swings.

For indium, the constraint is less acute than it appears. South Korea and Japan supply nearly half of US imports, though China’s dominant upstream position give the PRC latitude to exercise influence on the indium prices. Given the fact that prices have surged in the wake of China’s export controls, the policy priority for indium should be helping our partners and suppliers manage supply shocks and increase non-China supplies.

For graphite, both natural and synthetic, urgent action is needed. Synthetic graphite faces even greater concentration—China produces 97 percent of global supply—and domestic production requires substantial energy inputs that favor regions with low electricity costs. However, a substantial amount of investment has gone into domestic graphite production. over the last few years, and this January marked the first time that graphite has been produced in the U.S. in more than 50 years.

Bismuth, like gallium and germanium, is a byproduct, recovered primarily from lead and copper refining. The United States operates lead smelters and copper refineries that could integrate bismuth recovery, but current economics do not justify the capital expenditure. With a majority of U.S. consumption coming from China—the highest direct dependency among non-rare-earth controlled materials—bismuth represents a clear case where state-led processing investments could yield supply chain resilience.

Implementing these policies will require more detail than I have provided in this paper. Highlighting the twenty five high-priority critical minerals is a starting point for more targeted and effective policy, but these distinctions should clarify where America’s most immediate critical mineral interests lie. And already, the Trump administration seems to be following something of a prioritization policy in critical minerals. While the administration’s more active and robust support for critical minerals is notable, so is its focus on particular materials, especially rare earths. The equity investment in MP, offtake agreement, international deal-making, and support for the rare earth build out demonstrate that the administration is aiming for results.

Now, the administration should ensure that future critical mineral efforts, especially its most ambitious policies, take into account the differences between critical minerals and prioritize accordingly.

In recent weeks, the White House announced a $12 billion new stockpiling effort, Project Vault, which combines private and state funds to stockpile critical minerals. This should focus on priority materials. Similarly, the Under Secretary of State for Economic Affairs Jacob Helberg’s flagship supply chain effort led by –Pax Silica–has already indicated a promising vision for coordinating development for various ex-China supply chains. And most notably, at the Critical Minerals Ministerial at the State Department, Secretary of State Marco Rubio and Vice President JD Vance both spoke about using America’s network of allies and partners to form a mineral-buying and price-setting bloc. As these examples demonstrate, the administration has both an instinct for prioritization and a willingness to try new policies. Making this approach explicit, and using these twenty five materials to set a goal of complete independence from China, is the framework for tangible progress on critical minerals.

Prioritizing certain minerals is not a complete solution; other materials on the list are there for good reason. However, America’s most immediate concern is reliance on China for a particular set of critical minerals. Developing ex-China supply chains for 100% of U.S. consumption of these 25 materials is a short-term goal, but adopting this framework also sets up American industrial policy to better address future critical mineral threats.

Our lack of prioritization is a reflection of a deeper problem–an inability to make distinctions within a category. Some minerals are too big for active government intervention to make a difference. Some are not critical enough to justify it. The problem for some critical minerals is that China will interfere in the supply chain. The problem for others is an upcoming scarcity crunch that will impact the U.S. and China alike. All these different problems demand different responses. To the extent that prioritization is a solution, it is a solution for some materials and makes distinctions that could help solve others. For now, prioritization is a step in the right direction.

|

|

I happened to publish an article today on China’s export ban targeting MP Materials and USA Rare Earth. So here are my thoughts on Farrell Gregory’s policy prescriptions.

Even if these policies were executed perfectly, they would still fall far short of a real “Critical Mineral Security Endgame.” Gregory underestimates the distance between a policy list and industrial substitution. Critical minerals are not just a mining problem. They are an industrial-system problem. China’s advantage is built across extraction, refining, separation, purification, materials engineering, scale manufacturing, price control, export licensing, and downstream demand.

Strategic stockpiles can help with small-volume defense needs. They cannot solve large-volume industrial minerals such as graphite, copper, lithium, and nickel. Price floors are also much harder to internationalize than they look. European, Japanese, and Korean downstream manufacturers also want cheap inputs. They will not automatically agree to pay a long-term premium for a U.S.-led mineral price floor.

Offtake agreements face another constraint: the U.S. government itself is not the largest end-user. Defense demand matters, but its volume is limited. The real demand sits in EVs, batteries, wind power, power grids, consumer electronics, and semiconductor manufacturing. A 10% tax credit cannot close the structural cost gap created by China’s integrated industrial system. Equity investment has the same problem. The U.S. can put money into projects, but policy cycles are short, congressional funding is unstable, environmental and permitting conflicts are intense, local litigation is frequent, and projects remain exposed to commodity-price volatility. Whether the U.S. government can organize an industrial system over decades, the way China does, is a different question.

That is why I think the target of covering 100% of U.S. consumption of these 25 priority minerals from domestic or non-China sources within ten years is too aggressive. Twenty years would already be difficult, even under near-perfect execution.

A more realistic goal is narrower: within ten years, the U.S. and its allies should establish minimum non-China supply capacity for defense, advanced semiconductors, aerospace, power grids, and critical battery materials across these 25 minerals. That would create a security floor. It would not amount to full commercial substitution.

An interesting angle on this topic:

Recommendations for Strengthening the United States Strategy on Critical Materials (https://ebelousso.substack.com/p/recommendations-for-strengthening)