Economic Security Megapod

Featuring winners of our essay contest!

Earlier this year, we ran an essay contest on economic security. We gave entrants two prompts:

What are the most important high level KPIs that policy should aim for? What is the analogy of the Fed’s ’2% inflation and full employment’ target for economic security?

Where today would you put $10-50bn to get the most for your investment in economic security? Feel free to propose both defensive and offensive ideas, and either a portfolio of ideas or the one large idea you think will deliver the most value.

We ended up with a literal four-way tie for first place, with each judge giving a different essay top marks. We heard from Farrell Gregory earlier about how to spend rare earths money, and here, we’ll be spotlighting the three others who went into the framework question.

Joining us today — Jahara Matisek, a lieutenant colonel in the Air Force and fellow at the U.S. Naval War College; Naveen Krishnan at the Belfer Center and an intel officer in the Navy Reserve; and Guy Ward Jackson, senior policy analyst at the Tony Blair Institute in London. No one is speaking for the Air Force, the Navy, Harvard, the Naval War College, the Tony Blair Institute, or the Department of War. I’m speaking for ChinaTalk.

Our conversation covers:

Why economic security is really an insurance problem — you’re paying people to keep factories warm, workers trained, and capacity idle for a war that may never come — and why no democracy likes paying that bill.

Why the U.S. can’t China-proof its economy alone — the case for a distributed allied industrial base and using allied leverage and counter-coercion as an offensive tool.

What $6 billion and four years bought in artillery production, why it still wasn’t enough, and how Patriot missile economics expose the danger of having exquisite weapons without industrial depth.

Why you can’t science your way out of a volume problem — AI, robotics, and frontier R&D are caffeine, but the U.S. is still short on food and water.

Listen now on your favorite podcast app.

Frameworks for Industrial Resilience

Jordan Schneider: Welcome to the podcast, everyone, and congratulations. Jahara, as the senior member of this team, you’ll have to step up first. Why don’t you give the pitch on your framework?

Jahara Matisek: I was looking at this at a pretty high level — what can we do to get China out of the entire industrial base cycle? When I say the entire cycle, the first step would be getting them out of the mines, then out of the business of crushing and milling ore, then the separation and refining, then the metallization of those refined metals into actual usable metal, and finally the fifth step — the alloying and the manufacturing of products that go into the industrial base.

When I say the industrial base, I obviously mean making things for the military, but also important inputs for the U.S. economy — chips, circuit breakers, and pretty much everything in between. So much of the U.S. economy and military depends on metals, minerals, and alloys that pass through China at some point, if not entirely through China.

I decided to think about what we can do to China-proof the U.S. economy by investing in certain things to get us out of that downward cycle. Over the last few years, the Chinese have done a lot to economically coerce the U.S., putting export controls on graphite, germanium, and gallium. These are really important inputs across the entire industrial base.

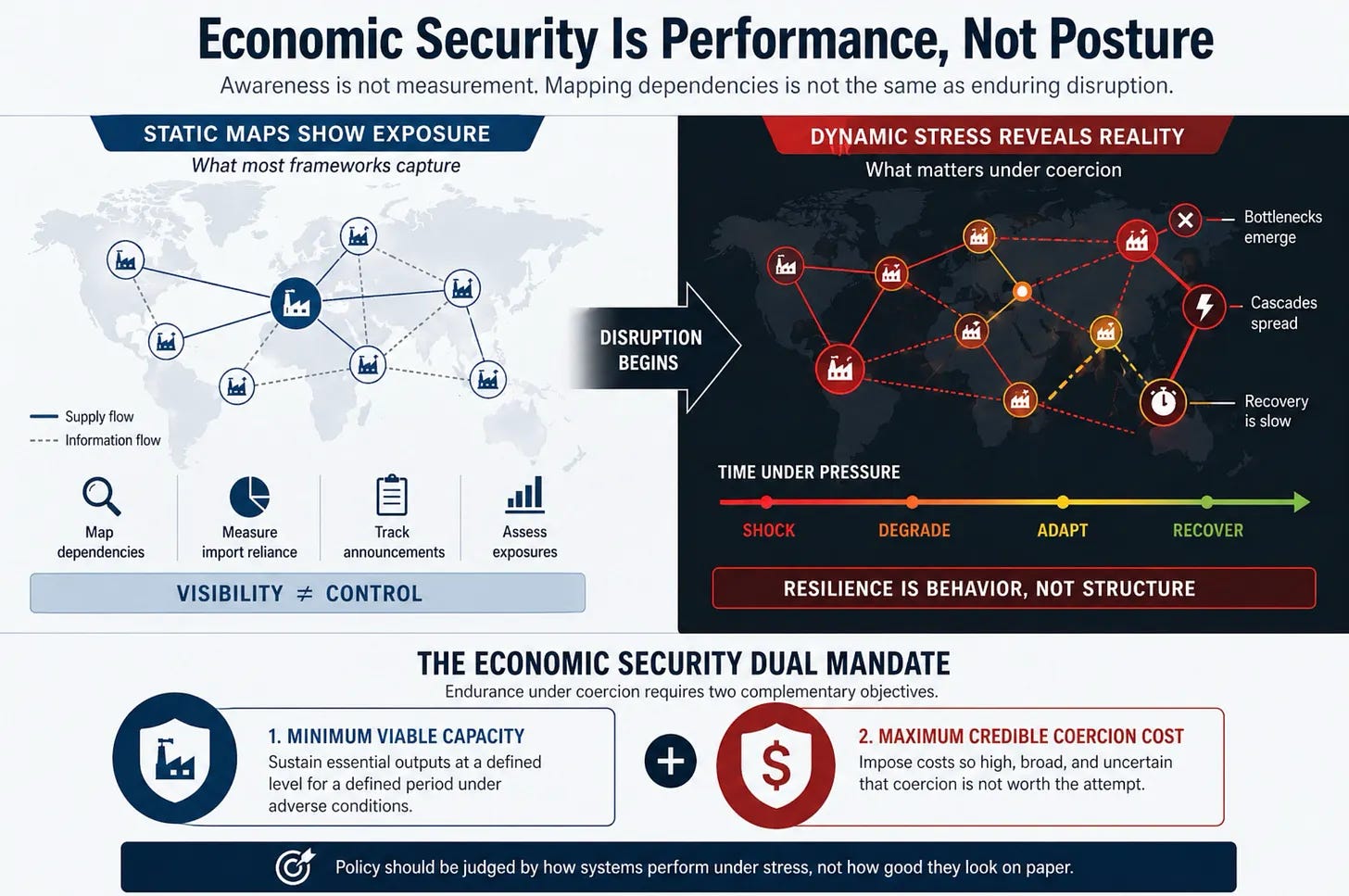

Jordan Schneider: You came up with these KPIs of minimum viable capacity and maximum credible coercion costs. How did you arrive at them, and what do they mean to you?

Jahara Matisek: I was thinking through a couple of KPIs it would take to start executing this and to measure it. The first was time to reconstitute production. The second, and more important — which became apparent after I wrote the essay, during the Iran War — was surge capacity.

The U.S. industrial base was optimized for peacetime efficiency. When you’re optimized for peacetime efficiency and a wartime crisis hits, you don’t have the people, the machines, or the capital to double or triple production the way the U.S. government and military want.

The third KPI was chokepoint concentration. That one gets us back to how to remove China from the entire mine-to-missile process. If a step isn’t partly or fully controlled by China, sometimes Russia is involved, and sometimes unstable countries like the DRC are part of it. What can you do, at a minimum, to onshore a given material or process to the United States, or at least friendshore it through Canada, the Europeans, Australia, and so on?

The fourth KPI was sub-tier supplier liquidity. A lot of people don’t realize that once you get past the big primes — Boeing, Lockheed Martin — many of the tier 2 and tier 3 firms that make a ball bearing, a chip, or an alloy for a missile are mom-and-pop firms. Often that’s the only company making that input. If anything happens to them — they go out of business, they can’t buy materials, they run out of capital — they simply disappear. This has been happening for a long time.

The fifth was what kind of stockpiles the industrial base can feasibly maintain, and who’s going to pay for that, because all of this is very capital intensive.

That took me to the $50 billion question. The first pillar was shoring up energetics for munitions. A lot of people don’t realize there are only one or two factories in the U.S. that can make the explosives and energetics that make missiles work. I allocated $15 billion to that, and the paper goes down the rabbit hole on it.

The next pillar is midstream processing for magnets, where the U.S. government has made some progress. Every motor needs magnets, and for the longest time China controlled that entire process. You probably heard about the big MP Materials deal from over a year ago, which is working toward sourcing everything from the mine to the magnet domestically, so every motor that goes into the industrial base can come from the U.S.

The third pillar is industrial finance for the tier 2 and tier 3 companies, which don’t have the capital Boeing and Lockheed Martin do. That means grants, loans, and credits to reward them for building in surge capacity.

The final pillar is machining. Over the last 30 years, the U.S. got out of the business of making machine tools and equipment, and it slowly migrated to Asia, concentrated in China. A lot of that needs to come back, because many of those machines and tools are the only ones that can make certain inputs for the industrial base.

Add it up, and that’s a minimum $50 billion investment across those pillars. The broader point is that this China-proofs the economy in a much cheaper way. My hope is it moves the needle, because it doesn’t need to be that expensive — but you have to start making these small investments now. Otherwise it will cost far more than $50 billion in the medium and long term, because you’ll be throwing money at people to solve a problem after a crisis has already hit.

Jordan Schneider: Great. Now on to Naveen. Walk us through how you conceptualized the problem.

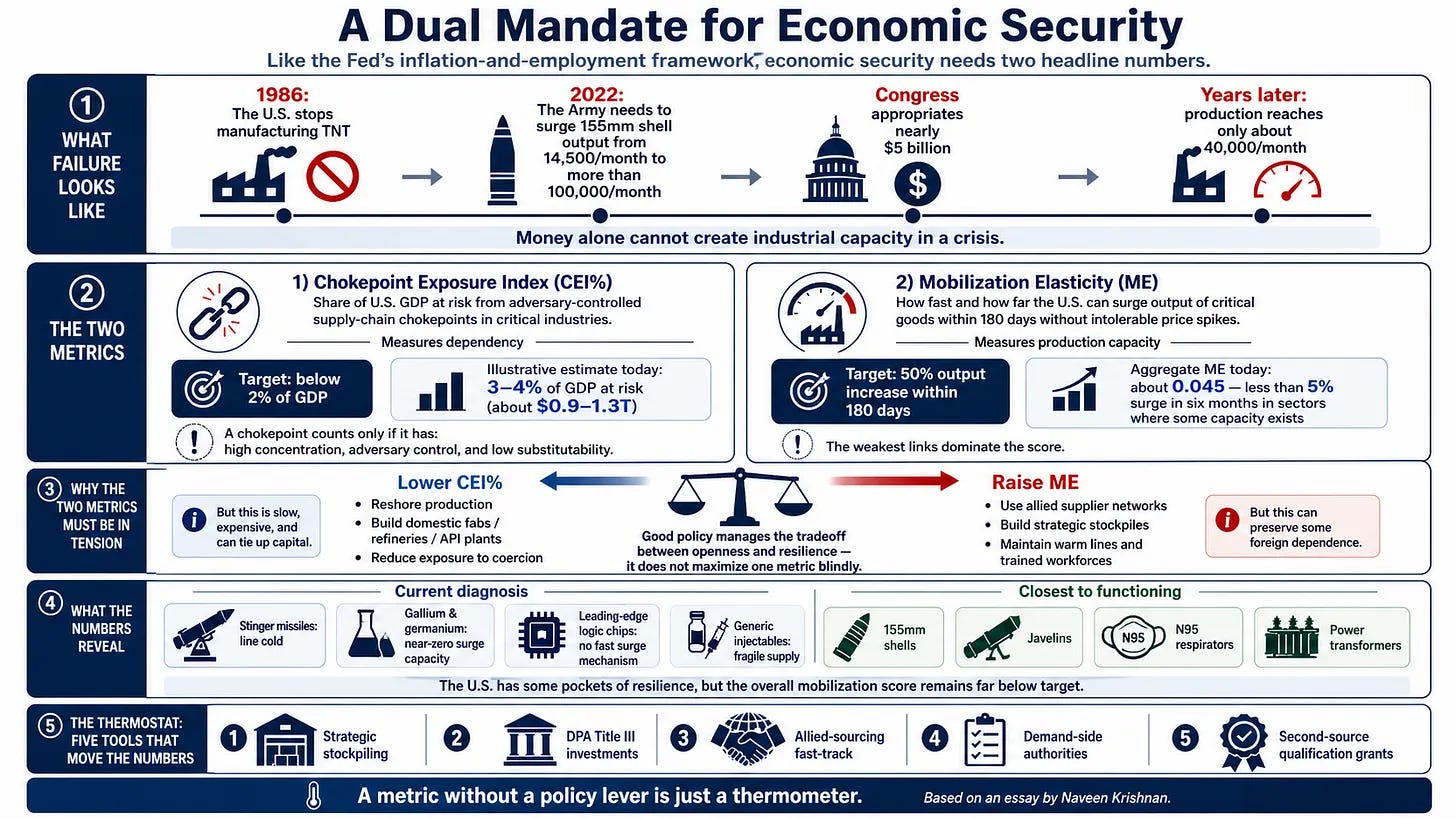

Naveen Krishnan: Similar to Jahara, I looked at that dual-use mandate, specifically chokepoints and the elasticity of surge. The way I arrived at this was informed by my time working in Congress. Last year I was an analyst on the China Commission, at a time when tariffs were a novel instrument and those high tariffs were genuinely shocking. We forget how quickly we adapted, but it was a shocking summer.

I noticed all these discussions about massive money sloshing around — people throwing out wild numbers for almost Christmas-tree-like sets of desires. Some said, here are all the minerals you want, here are all these parts of the supply chain, here are all these parts of healthcare. There wasn’t much rhyme or reason. It was as if someone woke up, read the Wikipedia article on a new vulnerability, and decided that’s where the money should go.

I wanted to focus on two frameworks working in parallel. The key distinction from the Fed’s mandate is that with the Fed, gaining on one goal — say inflation — usually means losing on the other, like unemployment. I zeroed in on chokepoint exposure and mobilization elasticity from both an offense and a defense point of view.

For defense, my chokepoint exposure index tells you what percentage of critical U.S. GDP — defense, minerals, parts of the healthcare system, and so on — is downstream of an adversary’s product, with a target of 2%. The complement is offense, which I’d frame as mobilization elasticity: your responsiveness to a crisis. It measures whether your industrial base can physically achieve, in my case, 50% surge output within 180 days without an economically ruinous price hike, depending on the industry.

That give-and-take is something we need as U.S. decision-makers, because what passes for industrial policy now is essentially a wish list — on any given day, a new pet project for a critical need. Those have to fit into a broader picture. Given how we’ve historically funded defense needs, whether through R&D or other projects, we haven’t had to examine how they interlock into a system. That offense-defense parallel — the critical exposure index, or CEI, and mobilization elasticity — struck a good balance.

Jordan Schneider: And Guy?

Guy Ward Jackson: It’s worth starting by saying I had a lot of fun with this, because I do a lot of European-focused economic security policy. When you put on your essay-prize publication that we had between $30 and $50 billion to play with, I thought, this is great — I can think with the U.S. hat on. If this were a European country, it would be significantly less.

Jordan Schneider: It literally is significantly less, right? The numbers around critical mineral spending are like $100 million here, $100 million there.

Guy Ward Jackson: Exactly. The broad concept of my proposal is taken from the idea of nuclear latency. South Korea and Japan fall under the U.S. nuclear umbrella and don’t have atomic bombs themselves, but they maintain a strategic approach: in theory, they have the industrial capacity and technical capability to build a bomb within roughly six to nine months. The catchphrase behind that concept is that you don’t necessarily need a bomb, but you need the capacity to build one. I take that idea and apply it to economic security in a fairly conceptual way.

Applying it to the U.S. context, economic security policy sometimes seems to fall between two extremes. One is the very offensive toolkit — chip export controls. The other is heavy-handed industrial strategy for what I call tier 1 economic security priorities: your fabs, the CHIPS Act, where yes, there’ll be some misallocation of capital, but the priority is so high that you need to do it anyway.

My argument is that there’s a massive tier 2 in the middle — things that are hugely important economically and from a national security externality standpoint. These are industrial bottlenecks that don’t quite rise to the tier 1 priority list. That’s the problem space my proposal addresses.

My proposal is an economic security latency fund on the order of $30 to $40 billion. The idea is to identify somewhere between 5 and 15 priority areas in tier 2 — areas you neither want to leave to the market nor treat at CHIPS Act levels — and use that money to fund both latent capacity and the ability to surge in a non-peacetime scenario.

A few recommendations fall under this. The first is the toolkit: what would the fund actually pay for, especially during the peacetime latency period before surge capacity is needed? That would include pre-crisis purchases — contracts that incentivize some overproduction so you can stockpile — and the ability to rapidly build modular facilities in areas you’ve identified.

The second aspect is prioritization, where I go into less detail and where more thinking is needed. Once you’ve defined your 5 to 15 tier 2 priorities, you need to prioritize among them. Even the U.S., with its fiscal firepower, cannot do everything. I think this gets to a point that both Jahara’s and Naveen’s essays reach as well: there has to be an element of prioritization.

I use the example of subsea cables and subsea cable repairs. You need some overproduction capacity in vessels and talent — the individuals and capability — so that if you were in an Indo-Pacific conflict, you could rapidly repair subsea cables. There’s also a deterrent effect: by having the capacity to surge, you dampen the incentive for an adversary to cut that chokepoint in the first place.

The final piece is thresholds. You need clearly defined thresholds for when you move from latent capacity to surge capacity, and those will vary by sector.

That’s the outline — far less sophisticated than Naveen’s and Jahara’s, but it gets at some of the same underlying themes: there needs to be more rigor in how we think about economic security, and more prioritization. Even the U.S. needs to prioritize, and in my European work it’s even more the case, because there’s less capital and less fiscal firepower. The final broad point is that the economic security toolkit can’t be only offensive or only heavy-handed industrial strategy. There have to be gray areas in the middle, and the idea that speed is sovereignty comes across in all the essays.

No One Likes Paying for Insurance

Jahara Matisek: What I liked about what Naveen and Guy were getting at — and it’s a theme across all three of our papers — is striving toward industrial resilience. The reason this is such a tough discussion is that it’s going to cost money, a lot of money.

That’s why Guy and Naveen talk about ruthless prioritization — what do we need to do now, and what needs to be done in the medium to long term, because we have to slowly fill these gaps? But it’s going to cost a lot, because you’re essentially paying people to build capacity without producing anything.

It’s easy to say we’ll just build a bunch of factories and spin them up in wartime. But what about the trained human capital to actually produce in those factories? That costs money. You may have to pay people to keep idle factories warm, because you need that manpower in a crisis. You’re paying people to do essentially nothing but keep the machines warm.

That’s the uncomfortable political aspect we didn’t really address in our three papers — though, to be fair, this wasn’t a contest on how to convince policymakers to pass it. The toughest conversation is whether we’re willing to say it’s going to cost all this money to have wartime capacity and endurance, and here’s the bill. And it’s not just an upfront investment; we’d have to pay this each additional year. It’s insurance. We’re paying for insurance.

In the long term, it pays for itself in theory, because you’re developing industrial sovereignty and making your country more independent and less susceptible to economic coercion.

To Guy’s point about undersea cable cutting: repairing a cable that’s been cut by an adversary — and China and Russia have been doing this a lot, whether accidentally or as acts of signaling — isn’t actually that hard. It takes about 16 to 24 hours to repair the cable itself. The problem is that it requires a lot of unique metals, and there aren’t many ships in the world that can do the work. Depending on where the cable is cut, it can take one or two weeks just to get a repair ship to the location. Once it’s there, it’s 16 to 24 hours to fix it.

If you do this enough, you eventually deter an adversary through the insurance program: we’ll have ten times as many cable-repair ships as we actually need, which signals, don’t waste your time, because it’ll only be a minor inconvenience.

The same thing is happening with U.S. icebreaker purchases. The U.S. defense industrial base can’t make them — we don’t have the people or the know-how — so we’re buying them from Finland. Do we really need icebreakers for current Arctic operations? Not really, because we’re not doing much up there. But by buying a bunch from another country, we’re investing in their industrial base while signaling to adversaries that we’ll be able to operate up there if they want to make an issue of it, or if there’s a geopolitical hot point.

Naveen Krishnan: One thing I like that you’re talking about, Jahara, is that we all explicitly called out autarky as unrealistic. That was a key thing I found in the essays. The more you dig in, the clearer it is that you’re not going to magically undo decades of globalization that have occurred since the ’90s and that support all of our countries.

Hyper-prioritization is the key point, and it’s why I opted for the two dual mandates: what are the overall targets we should aim for? A 2% target on CEI, maybe a surge capacity of X days for critical goods. Then you build your basket of goods around that. I agree with Guy that what you’re really going for is speed. Independence sounds nice, but you’re not going to achieve it across every industry. What you’re achieving is resilience — in a crisis, can you actively respond?

If a crisis hits, can you sustain operations, tactically or economically, long enough to reach a resolution, get back to some normalcy, or take care of the immediate threat? The idea that you’ll permanently have enough capacity for every critical thing forever — in memoriam — just doesn’t work. The numbers don’t shake out.

It’s almost like asking whether you have the immune system to handle a particular pathogen. You’re not going to survive a pathogen every single day in perpetuity, and we’re not building a new immune system.

So I parsed out some industries — defense, energy, healthcare. You can argue about whether healthcare belongs, and that depends. But the main thing I came to is that we really can’t have an omnicause, autarkic model where everyone puts their item on the wishlist. It has to be ruthless prioritization.

It’s interesting to see where that goes, because I don’t know what the discussion is like across the pond. In the U.S., minerals get a lot of the spotlight, especially the production line for munitions. I’m curious which other bubbles emerge as wishlist items in such a broad base.

Guy Ward Jackson: Naveen, to your point about how this is perceived on the other side of the pond: the prioritization problem is even more acute. In continental Europe there are clearly far more dependencies, and in that sense the U.S. is in a more privileged position. A lot of the conversations in Europe tend toward “we need sovereign AI models,” “we need autarky in cloud,” or “we need to de-risk from both the U.S. and China.” For Europe, that’s even more infeasible, so the prioritization question is even starker.

The other thing, Jahara, on your political point that this will cost a lot. There’s often a political incentive to sell economic security or resilience policies — and frankly, in Europe’s case, sometimes defense spending — as things with massive spillover effects that are therefore vital for growth. The argument goes: if we invest in whatever it is, it’ll have dual-use and spillover effects, it’ll be great for jobs and growth.

There are some examples where that’s probably true, and I’m sure there are U.S. policies with genuine spillover effects alongside building resilience. But in reality, some things aren’t dual-use, don’t have spillover effects, and yet you still need to spend money on them. That’s a harder political sell. Often it gets packaged as defense policy being growth policy, which is sometimes shoehorned in when it isn’t actually the case.

Jordan Schneider: What Jahara is advocating for — okay, we set up 20 missile production lines when we only need one — is almost anti-growth, right? You have people who could be doing economically productive things, but instead they’re sitting there keeping the machines warm. It’s an insurance policy, but you have to pay for insurance, and no one likes paying for insurance.

Naveen Krishnan: That was interesting to me. I’d love to have 20 lines, but we don’t even have three. And if we had 20 lines, I think we’d be running all 20, because lately — across the past two or three calendar years — we’ve been continually draining munitions.

What I really liked on the production front was the idea of production lines on standby, as opposed to just having the line itself on standby. There needs to be some standby capacity, which I also captured in surge capacity — can you actually surge? We both addressed the need for some flex in the system. I don’t know exactly what that looks like — whether it’s frontline stockpiles or pulling resources from elsewhere and reproducing.

I have a hard time when I look back at the World War II mobilization and read stories of Ford retrofitting its factories and making tanks the next day. I really struggle to imagine doing that now, because so much of this is niche production and the raw materials aren’t even there. TNT, for example, hardly exists in the United States anymore. So I think about what the surge would actually look like. Jahara, had you thought about what that full spectrum of surge capacity looks like?

Jahara Matisek: It’s important to put concrete numbers to this, because it’s easy to talk in the abstract. Artillery production is a perfect case study of how far behind the curve the United States is — and so are our European allies — on something we’ve been able to do since World War I. Here we are 100 years later, and we still can’t do it as fast as we thought we could.

When Russia invaded Ukraine, the U.S. was producing about 14,000 artillery shells a month. Once the war kicked off and the U.S. and NATO allies began shipping shells to Ukraine, Congress and the U.S. Army said it was unacceptable to produce only 14,000 a month and that we needed to reach 100,000. Why does that matter? At the height of the war, Russia on some days was firing 60,000 to 70,000 shells a day.

Now fast-forward four years. As of February 2026, we’ve thrown $6 billion at U.S. artillery shell production, and we still haven’t hit 100,000 a month — we’re only making about 50,000. We’ve had almost four years to surge from 14,000 to 100,000 and can’t do it in a timeframe that’s relevant to the speed of warfare. That’s a concrete example of something we’re already trying to do and can’t. To Naveen’s point, it’s because there isn’t much propellant or energetics, there aren’t enough machine tools and factories, and there aren’t enough trained, qualified people. You can’t Zoom-call your way into making artillery shells.

And that’s one of the easiest things to ramp up. Now look at Patriot missiles. During the Iran War, by some estimates, the U.S. and coalition allies expended about 1,700 to 2,000 Patriot interceptors in roughly 39 days. Why is that staggering? In under five weeks, the U.S. and its allies burned through three years’ worth of Patriot production. These are the interceptors that shoot down drones and missiles. That’s unsustainable.

A contract dropped last month to surge production, but they won’t be able to double or triple it anytime soon. Maybe by 2030 the U.S. and its allies will produce 1,800 to 2,000 Patriot missiles a year — but that’s years away.

These are the tough conversations people didn’t anticipate when you get into a near-peer fight, compounded by bad doctrine and assumptions about shooting things down. When the Ukrainians were helping with air defense in the Middle East during the Iran War, they were reportedly shocked to see certain militaries firing eight Patriot missiles at a single Iranian drone. Why is that unsustainable? A Patriot missile runs about $3 to $4 million a shot, depending on the variant, while those drones cost less than $30,000. Videos have also surfaced of 11 to 13 interceptors fired at a single Iranian missile. Those interceptors can cost anywhere from $3 million to $15 million depending on the variant, while the average Iranian missile costs maybe half a million dollars.

That’s another reason we have to have this debate: it’s economically unsustainable unless we find a better approach to making interceptors far cheaper and find alternative ways to shoot things down that don’t bankrupt us.

Guy Ward Jackson: We’ve been talking to frontier robotics companies in the UK, Europe, and the U.S., and one point that keeps coming up is that adoption of the next generation of industrial automation is going to be crucial. This won’t apply to every industry where the U.S. needs surge capacity, but the U.S. has offshored a lot of the dirty middle layers of its industrial ecosystem.

The point I keep hearing is that there’s now a window — because of frontier innovation in industrial automation — to reshore some of that capability and have surge capacity at a cheaper cost than would have been possible 20 years ago. If you can tie frontier innovation in industrial robotics to widespread adoption in the U.S. and make that a priority, it could help with some of the cost trade-offs and enable surge capacity in areas where the U.S. currently has none. Tying frontier innovation to broad adoption across the industrial base will be crucial for the U.S. over the next 10 years.

The Offensive Version of Economic Security

Jordan Schneider: I have a provocation for you. All three of you focus on time to reconstitute — how quickly America can get its act together so the squeeze isn’t as painful. That’s a defense-forward framework. Why didn’t you prioritize something like the amount of pain it takes for the adversary to inflict the squeeze — more of an offensive, defend-forward version of economic security?

Naveen Krishnan: When you say defend-forward, do you mean focusing on how much it would cost the adversary, and whether we can increase that cost for them?

Jordan Schneider: Yeah, that’s it. Or are there other frameworks besides time to reconstitute that you considered and threw out?

Naveen Krishnan: If I think about a weakness of U.S. security policy among decision-makers broadly: our economy is largely consumption-based. It’s not heavily resource-dependent, and we’re not a major resource exporter the way Russia is. We’re not a hydrocarbon market or a purely export-driven economy — we’re services. That arguably makes us more vulnerable to these kinds of shocks.

I view economic shock and turmoil as a large strategic concern for a U.S. policymaker, more so than for someone in Beijing. That’s what happens when you live in a democracy: you have to make decisions that affect the economy writ large. When I look at the list of U.S. adversaries, I view economic shock — relative to their domestic concerns — as a minimal worry for them compared to the U.S.

That’s more ideological and not strictly tied to the technical issues in our paper. But it’s something we’ll rightly have to weigh more heavily than our adversaries, because we operate in a more prosperous, interconnected economy, and we have to treat economic pain as a greater concern.

Guy Ward Jackson: Sitting outside the U.S., I may be biased, but over the last 8 to 10 years I think the U.S. has already squeezed a lot of its chokepoints on the offensive side. Part of the problem is that China has spent the last decade-plus de-risking from some of those chokepoints — not all of them, and you cover a lot of this on your other episodes.

This came to fruition when Trump went head-to-head with China, and it became clear that, by holding the critical minerals card, China had escalation dominance. My argument is that this wasn’t just because China held the ultimate offensive economic security card; it was because they’d de-risked from the U.S.’s chokepoints over 10 to 15 years.

The other thing I’d say — which I touched on in my essay — is that squeezing offensive tools is politically easier. To Jahara’s point at the beginning, telling your electorate you’re going to spend a lot of money on something that has no direct impact on them unless there’s a crisis is hard. And it’s very hard to prove it has an impact in a crisis, because the irony is that you don’t really know when it’s worked, only when it’s failed — and then you have a COVID-like situation. It’s politically easier to squeeze chokepoints offensively than to convince a U.S. electorate — one that spends more on debt than on defense — that it needs to build resilience and defensive tools. So there’s a political dimension here too.

Jahara Matisek: Bringing this back to Jordan’s question about why we didn’t address going on the offensive: I actually wrote an article, currently under review, that should come out in RUSI later this year, where I argue this can’t be a purely U.S., Canadian, or European solution. There needs to be a kind of NATO industrial commons, because as much as we’d all like industrial sovereignty, everyone in NATO has niche things they’re really good at. Pursuing domestic autarky is a waste of money and time, especially when another country can do it far cheaper and already has the ability and know-how to scale.

In that article, I argue we need to get past the idea of NATO interoperability, because it only exists on paper. I’d contend it stops after 5.56 and 7.62 rounds for guns. Everything after that, everyone is doing their own thing. We all say we’re NATO-interoperable, and everyone makes a piece of the F-35, but that’s a brittle approach to the industrial base.

There needs to be a proper NATO approach to the transatlantic defense industrial base — a real interoperability framework. If it requires a digital passport so we all know how to make a certain alloy or a part in a gun or a munition, and it’s interchangeable without going through recertification and requalification, that fixes the defensive side of the industrial base for the U.S. and its allies.

On the offensive side, I’ve been working through an idea called a counter-coercion leverage model. That’s how you actually help the U.S. and its allies China-proof their economies. You’d share industrial intelligence to identify the spots where we have a chokepoint over China that China doesn’t realize. The next time China tries to leverage us in a trade deal or turn off the flow of gallium and graphite — and China controls essentially 100% of the world’s supply of those two materials — we can counter: “Sure, you can do that, but we’ll turn off X, Y, and Z to your country. Are you sure you want to? Because we can cause you pain too.”

That bargaining point needs to be discussed: how can we counter-coerce as an alliance? You have to do it as an alliance, because China knows how to pick off allies one by one using its economic leverage. If you can do that, you’ve China-proofed your economy without spending tens or hundreds of billions of dollars. There are small test cases — the U.S. turning off the flow of Nvidia chips to China, for example. If you could do that at scale, you’d reach economic coercion parity with China and other adversaries, so these tools can’t be used anymore and the industrial base isn’t disrupted by geopolitical events.

Guy Ward Jackson: If I can hop in with my European-UK hat on — in theory I totally agree with Jahara. On the alliance perspective, the U.S. has eroded some of its easier wins on defensive resilience and economic security through alliances. Sitting in these conversations in Brussels and across Europe — the conversation right now is all about how to de-risk from the U.S. We know we won’t manage it in every part of the stack, but how can we build our own chokepoints? How can we ensure we have a stake at the table and national winners that sit at future points in future technology stacks?

The problem is that there’s a lot of low-hanging fruit for the U.S. on things like critical minerals and partnering with Canada and Europe. Quantum is another example — Jordan, you did a podcast on that recently. There’s no doubt the U.S. has the leading quantum hardware companies, but it doesn’t really have the component companies: the cryogenics, the advanced lasers, and so on. Europe doesn’t lead on the hardware side, but it does lead on the component side.

I’ve had conversations with people in both Europe and the U.S. about whether there could be a Pax Silica equivalent for quantum. When Europe thinks about that, they’re thinking, how can we build leverage in the quantum supply chain so we can play tough at the table with the U.S.? They’re generally not thinking about how to work together. That mindset shift, generated over the last eight years or so, will be tough to pull back.

Naveen Krishnan: When you crunch the numbers — and I focus a lot on defense tech and healthcare, while people tend to focus on minerals — any way you cut it, you need allies. That’s the only way to accommodate surge capacity in any given area.

In my paper, I looked at what I considered tolerable levels of price increases — where your economy doesn’t fully collapse — and there’s no way the numbers work without allies in the mix. Shipbuilding is a great example. We’re at maybe 0.05% of global capacity, if we’re being generous, and South Korea and Japan get us a lot closer to China.

So it’s an unfortunate development on the transatlantic side: more hesitancy as everyone tries to figure out how to diversify away from everyone — not just China, but the U.S. writ large too. From the American point of view, the one benefit is that you have a lot of pools to draw from: your Asian partners, attempts to grow resource relationships in Latin America — though I’m more doubtful there — and others. It’s messy, but if you’re making the best of the situation, you piece together where you can find parts of the puzzle and assemble a collage from this broad bucket of allies.

To Guy’s point about concern over American reliability, that uncertainty might push the relationship toward existing defense partnerships. The bucket that makes the most sense, or where more work is getting done, may end up being NATO, simply because there’s more structure around NATO than around technologies that don’t fit neatly into a defense-coded box. It’s easy for the Department of War or defense organizations to take ownership of defense-coded problems.

When we look at critical areas, some things aren’t neatly defense — things that don’t have an obvious owner. In the U.S. it’s relatively easy to shake some coins loose at the Pentagon for a pet project, but that funding looks very different once you leave defense and move into healthcare. Energy, for example, is across the board. The hardest thing is that I have these metrics, but outside defense there aren’t neat stakeholders. It’s much cleaner to have different countries and their militaries handle sourcing. The problem gets a lot messier when you leave munitions and weapons systems and look at raw materials, automated manufacturing, and healthcare.

Guy Ward Jackson: One thing to add: a lot of what we’ve discussed — munitions, subsea cables — are fairly traditional areas. The question of economic security and chokepoints inevitably tends to be somewhat backward-looking, because that’s where the data is. You look at existing production lines or technology stacks and ask, where do we have vulnerability, resilience, or leverage?

But from a state capacity standpoint, the U.S., the West, and Europe also need future-facing economic security capacity — people trying to figure out what the next big bottleneck will be. What are the next iterations of the AI stack that will be hugely relevant — the future of inference compute, for instance — and what happens if Nvidia loses its monopoly because other companies build more specialized compute? Having future-facing state capacity is a very important part of this.

It’s easy to be retroactive. It’s easy to think, “We’re so reliant on X — how did we miss that 20 years ago? Let’s correct it,” rather than asking, “How do we avoid an equivalent thing happening to something we haven’t even thought about, 20 years from now?”

We Can’t Science Our Way Out of It

Jordan Schneider: Another thing you all under-indexed on a little is buying your way out of these problems through research and novel technologies. Jahara, you brought up the drone, Patriot, and energetics stuff. Maybe there’s a better, cheaper solution out there, and we could throw some scientists and engineers at it. Any thoughts on how to conceptualize sciencing your way through these problems?

Naveen Krishnan: When I first took on this question — maybe I’m more of a fundamentalist — I look at the current defense apparatus, from Ukraine to the present, and the biggest problems the U.S. has aren’t the sexy ones. They’re basic: munitions issues and sheer volume, using technologies we already have.

I focus on the Pacific. There’s a rich literature, including plenty of armchair experts, arguing the U.S. is becoming what the Imperial Japanese Navy was — an over-indexation on exquisite systems to compensate for a lack of resources and industrial might, versus the U.S. in World War II simply out-producing every other power in steel combined. That’s industrial might versus exquisite stature.

In the Indo-Pacific, the issues I see are about volume. On innovation, there may be something to the novel skills used at the operational and tactical level with drones, but my point is that even the new tech is volume-oriented. Whether it’s automation, asymmetric defense, or AI enabling asymmetric defense, it still relies on sheer volume. I see volume as the biggest constraining factor.

The one caveat is that you do get efficiencies — automation in dark factories that reduces the need for human capital, or the ability to refine critical minerals at a higher yield, getting, say, 20% of synthesized gallium out of a sample rather than something smaller. But you still need a production line running. You still need the existing facility. So I view higher tech, novel R&D, and new solutions as nice-to-haves. The need-to-have is volume and something that works.

It’s like what you’re suggesting, Jordan — caffeine. It’s nice to have a stimulant to go a little faster, but you need food. You’ll starve to death on Red Bull. You need fat and carbs. That’s how I’d characterize U.S. capacity: we’re so far from needing caffeine. We’re holed up with no water or bread.

Jordan Schneider: Jahara, as the full-time member of the military, I need your take on CENTCOM energy drink consumption. What should we take from that?

Jahara Matisek: Oh, you mean the Rip Its? You can still find Rip Its — for the audience that hasn’t deployed to the Middle East, a Rip It is a knockoff Red Bull that’s been around the last 10 or 15 years. For a while after I got back from Iraq and Afghanistan, you could find them at your local Dollar Tree, where you pay a dollar for something low quality and cheap. I don’t know if you have those in Europe, Guy or Naveen. The wars in the Middle East over the last 20 years basically ran on Rip Its. That was our cheap energy drink. Whoever won that contract — the Rip It company — made off pretty well.

But to go back to what Naveen was saying about whether R&D, the frontier, and novel tech can alleviate the problem -– it’s like Matt Damon in The Martian, where he says he’s going to have to science the shit out of this. That’s what Jordan was alluding to: can we science our way out of this? In the long term, yes. In the short term, no. But I’d argue current policy makes it a no even in the long term, because over the last year and a half the U.S. government has pulled a lot of grants and funding from the universities and institutes working on materials science and engineering — figuring out how to 3D-print things we didn’t think we could print, recycling e-waste, and so on. These are things we should be able to science our way around.

But if you don’t put in the R&D money now, it ends up costing far more later, and it opens you to another point of coercion. From my perspective, the biggest problem is that we’re not investing in the science and technology needed to clear these industrial-base hurdles in the long term — and that’s where you really get the cost savings and economic efficiency.

I know the U.S. seems to have a blank check to do whatever it wants, and supposedly deficits and debt don’t matter. But at some point they do, and you need economic efficiency. If you haven’t invested in the universities, the research, and the grants to find designs and new materials that are cheaper, more effective, and more efficient, you’ll be a prisoner to contemporary economic coercion. You won’t be able to make weapons systems, quantum, or AI work as efficiently or effectively as an adversary. Over time, you lose your comparative advantage, because an adversary can do things at scale, cheaper, faster, and more effectively.

Guy Ward Jackson: One quick thing: the classic dynamic is that China goes for market share and overproduces while the U.S. focuses on the frontier — and that applies to many things, including AI versus China’s open-source ecosystem.

What I’d say goes back to the alliance point. In the end, the U.S.’s political economy is better optimized for leading at the frontier and taking that approach, while China’s is better built for allowing inefficiencies to exist and just letting them happen. By eroding some of those alliances — or at least going some way toward eroding them — and therefore reducing its ability to build resilience through cooperation, the U.S. has undermined its own comparative advantage. Its playbook is generally less good at mass but great at leading at the frontier.

Naveen Krishnan: On that point about China — since I look a lot more at AI spending now — there’s actually a flipped problem in how China sees the AI race. In Chinese media, they’re constantly citing the total CapEx that U.S. hyperscalers spend on data centers — $40 billion figures coming out seemingly every day — and they view it as if America has a Manhattan Project of resources aimed at the problem.

So, to your point, Jordan, it depends on the threat. With cyber, bio, CBRN, and that kind of frontier risk — and a certain amount of AI — I do buy that you can science your way out of it. I buy that novel things are emerging where R&D yields disproportionate output, like if it’s a Mythos-type capability.

But for this particular prompt — what are the weaknesses of U.S. industrial strategy, what am I worried about? — it’s actually the numbers game. It’s the very boring threats people have faced since we fought with spears and stones: can you field enough to sustain yourself until the threat subsides? That’s a manufacturing problem. R&D can deliver outsized results — you can automate, you can gain manufacturing efficiency — but not if you’re starting from zero. Maybe caffeine takes you from 80% efficiency to 90%, but it can’t take you from zero to 80%. You still need the baseline capacity. I view R&D as an accelerant that aids manufacturing efficiency, not a replacement for manufacturing that doesn’t exist.

Guy Ward Jackson: If we’re calling some economic security questions sexy and others unsexy, the frontier stuff is sexy and the bread-and-butter stuff — which is what the U.S. struggles with — is unsexy.

This is pure speculation, but I wonder — because I see it in the UK and Europe too — whether being a democratic country makes the unsexy spending harder to sell. It’s much easier to spend money on a DARPA-style advanced R&D project and have that accepted as a norm than to say, “We’re spending all this money in case there’s a supply chain shock,” when the electorate is worried about a cost-of-living crisis.

There may be a structural issue for the U.S., and arguably for other Western democracies. I definitely see it in the UK, where we’ve offshored essentially all of our industrial base. There’s no political incentive to say, “We have to spend money that would otherwise go to the NHS on rebuilding this capacity, because it’s essential for these reasons.”

Naveen Krishnan: One recurring theme is that, depending on the industry, there’s no way to solve the problem without some allied distribution at scale. There was this great article. For the past three years or so, everyone in the U.S. has been obsessed with the idea that we’ll have an industrial revolution, and we do see money coming toward reshoring certain capacities — but it’s extremely slow.

There’s a funny graph comparing the people who support this versus who would actually do the work, and a shockingly small percentage of Americans, when push comes to shove, actually pivot toward these industries. Granted, it takes a few years for the jobs to appear, then for training, then for people to enter those roles. But it’s like trying to race from A to B with all these zigzags when the straight line is obvious: we have countries with decent industrial scale that we have decent relations with. We should look at our exquisite goods, their volume, and figure out a distribution model. Jahara, did you have thoughts on that?

Jahara Matisek: It takes me back to the artillery example. At the start of the war, Russia was making about 1 to 2 million shells a year. Four years in, they’re now making over 7 million a year. Part of this is political willpower. If we needed to match Russian production, we would — but we don’t, because it’s seen as a priority, just not a top-five priority. A lot of this has to be treated as a priority, and that’s the ruthless prioritization issue, with all its politics.

We can throw $6 billion at making more artillery shells, but without accountability, leadership, and follow-through, it just meanders. Then people say, “We can’t make as much artillery as we thought, because we can’t get the propellant — there are only one or two factories that make it. We’re trying to convince them to hire more people and source more materials, but we haven’t figured out the mechanism to fund it.”

That ends up being the dumbest reason things don’t happen. Government asks, “Can you do this?” The private sector says, “Yes.” A few months later: “Have you done it?” “No, because you haven’t given us money or a long-term contract to incentivize us.” So they say they’ll do it, but they don’t have the money.

Or: “Yes, we signed a contract to produce this many shells at a per-unit price, but because you wanted us to surge, the supply chains drove the price of materials up double or triple, and now I can’t afford to deliver. We need to renegotiate, or you can cancel the contract.” And then you’re out of luck, because nobody else can really do it.

That’s another tough, modern acquisition and contracting problem: there isn’t enough flex in the system to adapt to reality. A company gives you a quote, and it may look like price-gouging when costs rise, but they genuinely can’t deliver as many, and it takes longer than expected because of weird bottlenecks.

For anyone listening who wants to get rich in the coming years: if you can focus your company or startup on industrial intelligence — identifying every little bottleneck — you’ll get really rich. I wish I could do that, but I’m stuck in the Air Force for four more years. So whoever wants to hire me — Guy or Naveen or Jordan, you all look really smart….

Naveen Krishnan: I’ve got my MBA coming up. On your point about willpower: that works for maybe 30% of our problems. If push came to shove — if a bomb were going to destroy Earth and we needed to produce X shells — we’d find a way through sheer political will, turning over every stone.

Jahara Matisek: It’s the World War II model, right?

Naveen Krishnan: But you can only get so far with that. With certain toolkits — robotics, drones, parts, actuators — and with materials like gallium, there are things you physically cannot will into existence. You could have everyone descend from the heavens and magically turn the cranks, but some things can’t be willed within a six-month timeline.

A lot of it is honestly, poor vendor management. From my time as a consultant, the Department of War and DoD have fairly weak teeth around contractors, because unless you’re doing a wartime seizure of assets and factories, you can’t compel them to the degree you’d think. But even then, that’s maybe 30% of the bucket. There’s still 70% where we’re not producing many more ships than we already do. The shipyards are there, and you could build a shipyard in a few months if the powers that be insisted. I’m curious whether Guy or Jahara have thoughts on the things we physically can’t spend our way out of without years of CapEx built into the capacity.

Jahara Matisek: The best example, to put concrete numbers to it: in the U.S., it takes about 26 to 29 years to open a mine. By “open a mine,” I mean you identify a spot in the hills that looks like it has minerals, and roughly 26 to 29 years later you’re finally getting usable output. That’s almost three decades.

You might think it’s the bureaucrats, the laws, the regulations. So look at other countries: the fastest you can do it is 16 years. Even if you throw out all the rules, it still takes about 16 years to get usable amounts of minerals out, because — to Naveen’s point — you can’t just throw money at it and do it overnight.

Even if you could will your way through that 30%, it would still take 10 or 12 years to get usable metals or minerals out of the mine. That’s the bigger-picture problem: there are industrial processes that simply take time. Unless you put every human on the planet to work digging that hole, it won’t happen on a timeline that’s useful in a crisis.

Guy Ward Jackson: There are a few factors in deciding what counts as an economic security priority. One is strategic importance, but an underdiscussed one is feasibility. Even the U.S., which is in a much better position than most Western governments on fiscal firepower, will — and this goes back to the allied question — sometimes lack the feasibility.

The other thing, and it’s an obvious but important point, is that economic security priorities are badly distorted by political incentives. This applies 100% to Europe and the UK as well. Sometimes the U.S. is protective of the wrong things and not of the right ones.

For example, when Nippon Steel was trying to acquire part of U.S. Steel under Biden, I’m fairly sure CFIUS, under some pressure, effectively blocked the acquisition. I remember thinking at the time that it was a good example of a bad thing done in the name of economic security, because it was politically popular and sounded like protecting U.S. Steel and national security. Similar rhetoric happens in the UK. But that was a no-brainer: U.S. Steel could have really used the injection of cash and R&D capacity that Nippon was going to provide, and in a way that wouldn’t have required the U.S. to spend money.

One of the fundamental problems with economic security as a discipline — and as an aspect of state capacity — is that it’s so easily distorted by short-term political priorities. To Jahara’s point, long-termism is therefore very difficult to sustain within economic security state capacity.

Jordan Schneider: Any concluding thoughts? What do you want to leave the kids out there with?

Naveen Krishnan: When you dig into the numbers, there’s really no way to solve this puzzle — industrial capacity, economic security, supply chain reshoring, whatever buzzword you prefer — without a system of global partners. The numbers just don’t crunch otherwise.

For the United States, if I look at adversarial threats globally, I put my attention on China; others may have bigger buckets. Looking at the assets in the U.S. bucket — alliances, hopefully going forward, and the inclusion of exquisite R&D and exquisite capacities — those are the strengths to leverage, while volume sits in the adversary’s bucket.

When you’re solving for volume, look at what you have. South Korea and Japan build a lot of ships, something we can’t do. Any view of economic security has to embrace that. If you’re not looking at it as part of your solution, you’re in denial about how the numbers crunch.

My takeaway is that economic security is really an umbrella for global industrial strategy. Nations have industrial strategies that address national elements, but you have to think about them along distributed supply chains. Even with the mine example, the mines themselves usually aren’t the limiting factor — there are plenty of mines for the minerals we need in Australia, Canada, and elsewhere. It’s refining that’s the bottleneck, and that’s a distributed chain. Whatever list of critical sectors we settle on, we’ll need a sophisticated ally chain to meet the need. The U.S. has the benefit of many different groups to draw from — the EU, Indo-Pacific partners, and others. That’s where I hope industrial policy moves, though it’ll have to overcome these domestic challenges.

Guy Ward Jackson: I’m happy to go next, though “final messages for the kids” feels rich coming from me — I think I’m one of the kids.

Very crudely, economic security is three things, and the third is often left out. The first is leverage — where you have chokepoints, the offensive side, to your point, Jordan. The second is resilience, which is where most of this conversation has focused: surge capacity and everything we’ve discussed.

My final takeaway is the third aspect: restraint. This applies more to Europe and the UK, but it applies to the U.S. too, and sometimes the U.S. forgets that. This goes to something Chris Miller has written about — opportunity costs. The difficult question in economic security is often where you decide not to spend money. There are lots of important things, and the way I frame it in my essay is tier 1, tier 2, tier 3 priorities. Figuring out where you show restraint is almost as hard as — if not harder than — pulling levers.

Jahara Matisek: For the kids out there: this is about education and educational reform. The West has collectively forgotten how to make the stuff that lets you make the stuff.

I feel bad saying this, but if you wanted that art history or literature degree, there isn’t going to be a job for you in the coming years. Look for a school with a mining engineering degree, or programs in alloys, materials science, industrial engineering, and manufacturing — because this is the missing middle that the U.S. and the West abandoned over the last three decades, when the Chinese were willing to do it for pennies on the dollar. Now we have to do it again, and it’s unsexy. You can’t Zoom-call your way to making the parts that make the stuff.

I’m saying this as a 42-year-old with a political science degree, telling the kids not to waste their time on one because it’s worthless now. Focus on knowing how to make the stuff that makes the stuff. That’s my old-man-shaking-at-the-sky advice.

Naveen Krishnan: That’s good advice. Hopefully, Jordan has a more upbeat note to end on — something positive.

Jordan Schneider: No, man. I think we all just yearn for the mines. I guess the answer is just more people underground.

Congratulations again, and I’m looking forward to recording the “Oh My God, Look How Economically Secure We Are” show in three years’ time.

Jahara Matisek: More like 30 years, but yes, Jordan.

Naveen Krishnan: I appreciate your optimism.