Rare Earths

What is to be done?

To discuss, we have Farrell Gregory, a researcher at the Foundation for American Innovation and winner of ChinaTalk’s Economic Security essay competition, and Joris Teer, a policy analyst at the EU Institute for Security Studies who authored Beijing’s critical raw material weapon – and how to dismantle it. Co-hosting is ChinaTalk’s Aqib Zakaria.

Our conversation covers...

China’s critical mineral weapon — How Beijing turned its dominance over rare earths into a tool of economic coercion and why the West is struggling to respond.

25 minerals that actually matter — Why policymakers should focus on the specific materials China can weaponize rather than spreading resources across broad critical mineral lists.

Why subsidies alone won’t fix the problem — How China’s industrial policy, overcapacity, and ability to flood markets make it nearly impossible for Western supply chains to compete without coordinated action.

Reshoring the industrial base — The tradeoffs behind rebuilding domestic capacity: higher end-product costs, environmental NIMBYism, skilled labor shortages, and the need for deeper US-European cooperation.

The next resource race — How defense, AI, robotics, and energy demand are intensifying competition for critical materials and what the future of allied industrial power might look like.

Listen now on your favorite podcast app.

The Threat of Rare Earth Armaggedon

Jordan Schneider: We’re going to spend most of this show talking about solutions, but it’s important to define the problem statement. Joris, why don’t you open with what happened over the last 12 months and why it requires liberal democracies to do something about it?

Joris Teer: After foreshadowing for a very long time that China might use this critical raw material weapon — squeezing the supply of all the key materials we need for our defense industries, energy grid, communication systems, etc. — it finally did so in April.

It didn’t just do so against the United States in response to the tariffs and in response to what appear to be far more extreme curbs on ASML semiconductor manufacturing equipment exports to China looming in May. No, it curbed supplies very sharply to almost all countries.

We were in a bind, and at the time it really seemed like we might enter rare earth Armageddon, which the International Energy Agency defines as $1.5 trillion in terms of cost just for the EU alone if we don’t get our permanent magnets anymore.

China reversed the dial and increased exports again of not just rare earths but other critical raw materials, but at artificially low levels under strict conditions that are completely averse to our interests and completely in China’s interest. It’s now very aggressively playing out that leverage.

Farrell Gregory: On the US side, the main difference is that we saw export controls — particularly for gallium and germanium — utilized for the first time in 2023, whereas the rare earth export controls that particularly Europe has found so troubling were in 2025. Our concern and direct exposure to these export controls stretches back to 2023.

Jordan Schneider: What’s been the response in Brussels and other European capitals? What’s been done so far?

Joris Teer: Brussels has been thinking about this for a long time. In the context of the energy transition, critical raw materials became quite prominent because everyone realized that without these materials, you can’t manufacture wind turbines, which are rare earth intensive. You can’t produce EVs, also rare earth intensive. The batteries require cobalt, of course. A lot of reports were written.

Then, in 2023, there was a Critical Raw Materials Act setting specific goals for domestic production in terms of mining, refining, and recycling, with a maximum dependency of 65% on any one country. More recently, Brussels identified 60 strategic projects. This is good — there’s substantial analytical work, and that analytical work always has to precede actual policy action.

However, Brussels hasn’t taken the required actions, and neither have European capitals. We haven’t formulated a good answer on how to make critical raw material production outside of China financially viable despite Chinese state support and the threats of always being able to flood the market. There’s also the issue of Chinese export bans on key rare earth production technology that go back to 2008.

Jordan Schneider: Farrell, how about on the US side? What steps have been taken?

Farrell Gregory: That’s why I bring up this direct exposure we’ve had since 2023 — it’s the accelerant that pushes government policy. You can pull this back several decades to the initial opening of the US economy to China. But more narrowly, post-Chinese export controls of materials to Japan, it becomes more definite.

On our end, towards the end of the Biden administration and into the Trump administration, it’s become tangible, concrete, and policy has as well. The Biden administration implemented very broad subsidies for a very broad list of materials. In the Trump administration, we’ve seen a lot more concerted effort over a few high-priority, high-China-exposure materials. My thesis is that this subsequent approach is a lot more likely to yield real results. It’s focused on the much more pertinent set of materials as opposed to the much broader list that a lot of the US government runs off of.

Overrated and Underrated Minerals

Jordan Schneider: Let’s go to that then. What are some different ways that folks have been prioritizing what to spend money on? Why don’t we have Farrell and Jorris both give their preferred frameworks of what to put first and what to put last on the list?

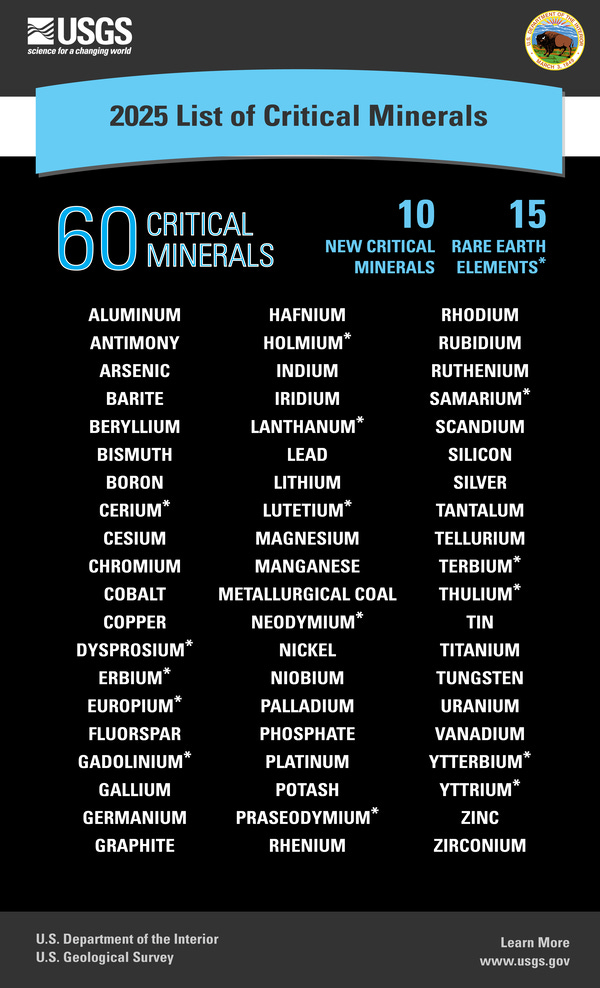

Farrell Gregory: My framework is basically this: if the US wants to reduce exposure to materials China can use as leverage in trade negotiations or broader geopolitical competition, we have to focus on those specific materials. There’s a power law dynamic across the 60-material US Geological Survey list, which is often the reference point for both federal and state governments.

Out of these 60 items, China has no meaningful leverage over dozens of supply chains. A few fall in the middle as edge cases. As I identify in my essay, there are about 25 materials — the majority being rare earths, especially heavy rare earths — where China has tangibly implemented export controls in the past. We need a much more targeted policy for these 25 materials, not just white papers disconnected from current reality.

The Trump administration’s critical minerals policy follows this approach. They’re moving away from broad-based tax benefits like the 45X tax credit, which spreads money across a wide list of minerals, many of which aren’t nearly as essential. This approach diverts money and attention from materials that have actually been subject to Chinese export controls and restrictions. China is using their leverage and telling us exactly what it is. My position is that the US government should respond by focusing attention and capital on reducing our reliance on these specific materials China has indicated it wants to use to extract concessions.

Jordan Schneider: Let’s play overrated and underrated. What mineral has gotten way too much attention that actually isn’t a big deal and shouldn’t be receiving taxpayer dollars?

Farrell Gregory: Lithium. Lithium gets attention for good reasons — it’s necessary for all sorts of hardware, most notably EVs. In the domestic reindustrialization conversation, lithium also gets attention because geological findings in the American South and Northeast make for great headlines about how the US has enough domestic supply to never rely on foreign countries again.

But it stops at the headlines. For various reasons, it’s very difficult to proceed with these projects. Lithium is an enormous market, so if you have benefits spread equally across every item on the list, lithium naturally sucks up a lot of capital by virtue of its size and the number of ongoing projects. That’s why I think lithium’s overrated.

Jordan Schneider: Do you have an overrated one, Joris, or do you disagree on lithium?

Joris Teer: I find it personally very difficult to untangle because if you look at some of the key materials like gallium or rare earths, they’re systemic — they’re in everything. Gallium is used to produce both gallium arsenide and gallium nitride wafers for semiconductors, which are in all of our radio frequency and many infrared products. They’re used to make things more energy efficient, and as a result, they’re pretty much ubiquitous throughout guided munitions, jet fighters, drones — everything you need for your national security. They’re also broadly used within the medical sectors because you’re basically talking about general-purpose chips.

On the rare earth side, you see something similar. There’s definitely a core group of materials that I think Farrell catches very well that are systemically important. Whatever you’re trying to build in this digital age, good luck doing it without them.

When you look at other materials like lithium and cobalt, I know less about them, but you’d be surprised how many of these key platforms — fighter jets, drones, AI data centers that you need for command and control nowadays to train algorithms — ultimately make use of tons of batteries. Maybe you don’t need the volumes required for all the EVs, but throughout everything we hold dear to protect ourselves and keep ourselves prosperous, most materials on the critical raw material list here in Europe have some sort of systemic applications.

Another example is antimony. It’s a hard material used for producing bullets, but it’s also a flame retardant, which is pretty important if you’re trying to build anything military, but also general objects like tables and other things we don’t want to catch fire in our houses.

Jordan Schneider: Is Farrell’s priority list basically one-to-one for the European context as well, or are you fighting somewhat different battles?

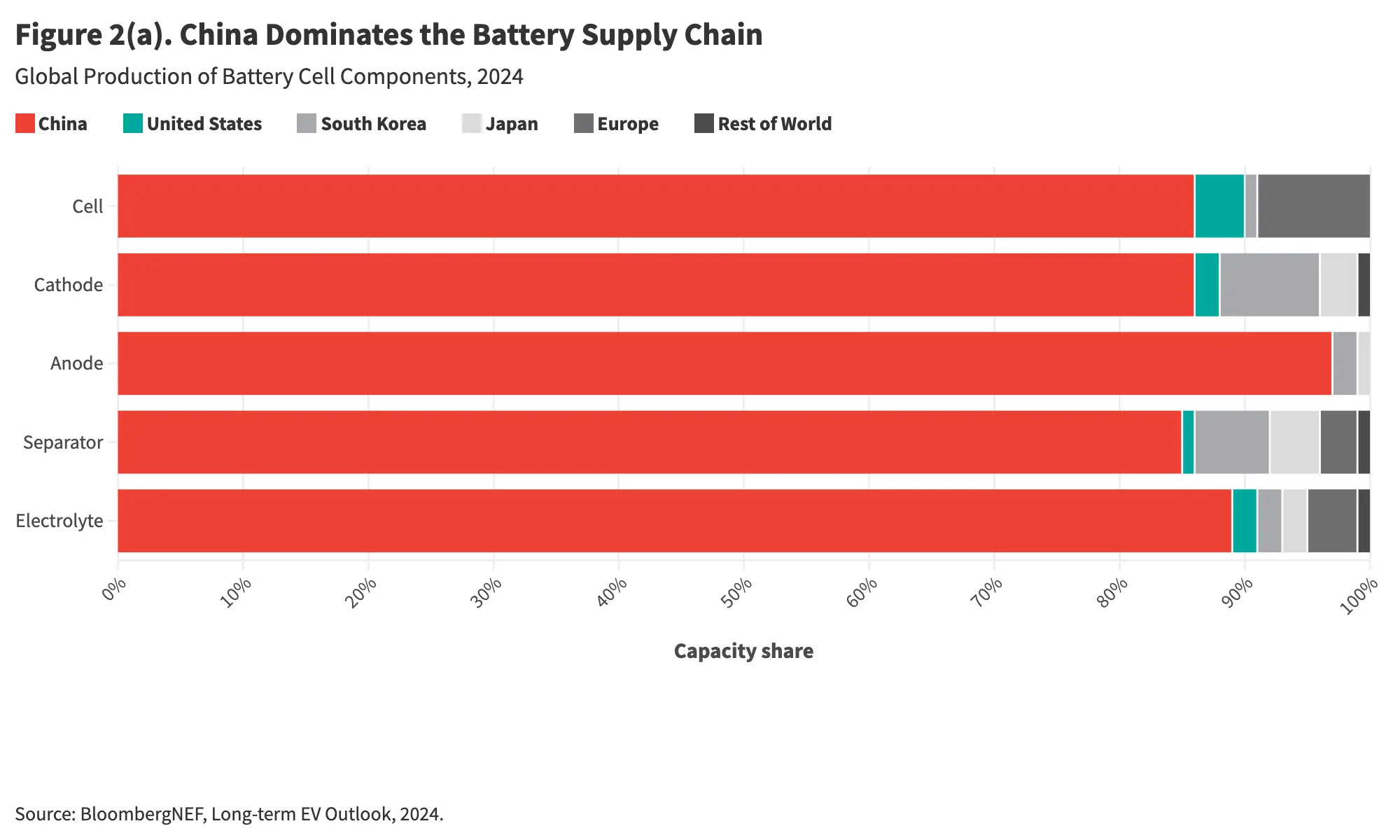

Joris Teer: I can’t dispute the emphasis on rare earths or gallium — they’re hyper-important for the systemic applications I just discussed. What worries me is that while the US and Japan have been relatively successful in plugging supply chain holes — the US brought rare earth mining back online in the mid-2010s, and Japan revived mining and refining operations in Australia and Malaysia — I remain hesitant about our broader systemic competition with China.

China now holds such a dominant percentage of production in battery cells and permanent magnets. Its share in chemicals is growing rapidly, with some estimates placing it above 50% of global production.

{kind=link}

Consider gallium’s trajectory: According to the US Geological Survey, gallium was still 100% produced in China last year. Yet in 1990, the EU and Japan held the majority of production. Throughout the 2010s, Chinese overproduction led to mass stockpiling and the collapse of international markets and prices. Competitors went out of business, and what began as overproduction evolved into overdependence, ultimately becoming a tool for economic coercion.

We’ve witnessed this pattern across numerous critical raw materials — 17 out of 34 materials on the European critical raw material list are now either 70% mined or refined in China. Beyond raw materials, we’re seeing these dynamics emerge in battery cells and increasingly in chemicals.

If critical raw materials are the skeleton of global manufacturing — pull them out and nothing works — then chemicals are the connective tissue and semiconductors are the central nervous system. You need all three elements outside of China, with reliable connections to them, to produce vital end products. This is why I struggle with the “plugging holes” approach that relies solely on subsidies and state equity investment without a more holistic demand-side solution.

Policy Tools and Solutions

Jordan Schneider: Let’s jump to potential solutions then. People talk about price floors — what tools are available to address the minerals in the red bar that you both agree are most worrisome? How do you evaluate the various options?

Farrell Gregory: The good news on the US side is that we have increasingly more tools the government is willing to deploy to plug holes. In some cases, that’s actually the ideal approach — individual deals involving equity in companies, specific assistance on accelerated permitting, or capital. There are many different tools in this much more targeted, concerted intervention.

We also have broader, more traditional tools that have been used over the past couple of years, like tax credits. The 45X tax credit was applied to the previous version of the list, though it wasn’t updated. These traditional tools like price floors and tax credits are helpful at the margin — and the margin can make a big difference — but they’re not as direct or capital-intensive as some measures we’ve seen over the past year.

My argument, even within this high-priority list of 25 materials, is that you’ll need different tools for different materials. You’re dealing with vastly different scales — the rare earth market compared to copper, for instance. There are significant points about market dynamics I won’t delve into here, but even among the highest-priority materials, there are substantial differences in which tool might work best.

When you’re plugging holes, you need to be open to using a wide variety of tools to address different materials — everything from the very targeted interventions we’ve seen for rare earths to less capital-intensive but still direct policies for larger materials or markets.

Jordan Schneider: We can discuss the principal-agent problem or the coordination challenge here. We have numerous tools and markets, along with various bureaucracies involved — ranging from permitting authorities to Deal Team Six investing in specific mines. There’s also the global coordination angle: you don’t want to duplicate efforts if you’re only targeting a billion-dollar market. How significant is this coordination mess, and is there a path forward to manage it in a less emergent or more centralized way? Or should we just let it manifest organically?

Joris Teer: We almost miss our market economies where there’s simply demand for a particular material and a company jumps in to meet that demand without central planning. If you took China out of the picture, that’s exactly what you’d have. But market actors aren’t moving independently because they know China can flood global markets at any moment.

That’s essentially what China did last year. First, they sharply curtailed supply to show the pain they could inflict. Then they used the licensing procedure to gather IP knowledge from defense industrial networks. Finally, they brought back supply for several materials, but at lower, strictly controlled levels.

In the best-case scenario, I’ve been told only dozens of European companies have received general licenses so far. Even then, China only supplies volumes through 2026 based on averages from 2023 — 2025 for each company. They provide supply at reasonable prices, but this depresses any mining firm that might think, “If the Chinese aren’t supplying anymore, I’ll make this investment for the next three decades.” These firms know China is still drip-feeding supply and might turn around and kill nascent projects.

This brings us to the coordination question. We’re thrown into a new reality where it’s no longer just firms identifying needs, generating demand, and other firms meeting that demand by creating materials. We’re dealing with a monopolist, and we have to intervene politically, which is frankly a nightmare.

In the EU’s case, we’ll have to do this for 17 out of 34 materials that China either mines or refines at over 70%. If the EU’s deindustrialization continues at China’s benefit — along with larger parts of the world — my question is: Are we going to continue this approach of plugging holes? Will we support companies? Will we provide state support for legacy semiconductor producers and semiconductor wafer manufacturers?

I personally think this is unsustainable. The only real option is to build a sectoral tariff wall around China to artificially make their products far more expensive in our markets.

Dismantling China’s Critical Raw Material Weapon

Jordan Schneider: This leads into the broader theme we explored in the Economic Security essay contest: To what extent is all of this feasible? As you mentioned, Joris, there are other leverage points to be squeezed, even if we find tons of antimony, figure out how to process it, and work through all 24 minerals that are in the red zone. You’re doing a PhD on this question — what are the different ways to approach both the defensive and offensive sides of regaining escalatory dominance in the economic domain?

Joris Teer: Unfortunately, my PhD is still in its early days, but I’ll draw from my work as an analyst at the EU Institute for Security Studies. What we emphasize in our paper is that we cannot simply dismantle the critical raw material weapon on our own. I’m very skeptical of a Europe-alone approach, primarily because of our high energy costs. We face significant not-in-my-backyard movements, permitting timelines are extremely long, and we’re not making the same level of funding available that the US and Japan have committed.

However, I am optimistic about an approach where we align demand-side incentives with the United States, Japan, Korea, and Australia. By creating this buyers’ club, we should extend an open invitation to specific mineral-rich countries — like Malaysia (an important producer), the DRC, Brazil, and others — to join, provided they erect the same tariff and public procurement barriers against China.

Without this scale, even the US will struggle to plug all the holes, because China’s industrialization continues unabated. According to the UN, China is projected to control 45% of global manufacturing by 2030, up from its current 30%. We’re going to discover that China has numerous levers they haven’t yet pulled but can deploy in the future. We need allied scale to dismantle the critical raw material weapon.

A crucial component is deterrence — we must understand economic deterrence in the trade domain and ensure we can make credible threats to China. If there’s a lesson from last year, it’s that the Chinese don’t find the threat of 120% tariffs as convincing as their own ability to withdraw critical raw materials from US and allied critical sectors. They recognize that the pain inflicted this way is much sharper and immediate, whereas tariffs cause gradual bleeding over time. China likely has a far higher pain tolerance than any of our societies.

Aqib Zakaria: How can the US and EU effectively collaborate on these issues? In the US, much of the debate centers on friendshoring versus reshoring. When we’re investing in mineral production and allocating funds, the American perspective tends to be: why not spend it on American projects? Why invest in European or Australian projects, even though collaboration might ultimately be more effective? How do you balance these competing priorities?

Joris Teer: That’s a great question. First, investing in many critical raw materials isn’t particularly attractive because it’s debatable whether you’ll make back your investment or face endless subsidies and supports. The problem is that China can always flood global markets.

This is evident in the US and Japanese approaches, where both have implemented extensive price floors — the Japanese one running until 2038 — with ongoing subsidies just to keep heavy rare earth supply alive. The Japanese face similar dilemmas: they’d love Europe to join them and change our public procurement policies to prioritize “European plus partner” suppliers for all the wind turbines we’re building, which need permanent magnets and rare earths. Europe has significant leverage through demand from EVs, wind turbines, and our rearmament push.

However, until that happens, the Japanese are saying, “We’re spending all this public money, so 75% of all the heavy rare earths we produce are earmarked for Japanese industry only.” This illustrates the second-order effects of Chinese policy. They curb supply, create scarcity, and while some countries de-risk faster than others, Toyota and Volkswagen still need to compete — but Toyota will likely have its magnets while Volkswagen won’t.

These dynamics play out on the American side as well, with projects making enormous amounts of money available through $10 billion direct loans. But Chinese policy is focused on preventing anyone from stockpiling. There’s global scarcity, and suddenly huge volumes and money come online on the US side to purchase not just rare earths but other critical raw materials worldwide for stockpiling.

In short, China has brilliantly introduced a wedge in the G7 at various stages. The only way to mitigate this is to prioritize a large block of materials and partner suppliers. If we’re going to do public procurement for G7 plus other key partners — for instance, permanent magnets in our wind turbines (12,000 kilograms of permanent magnets per offshore wind turbine) — we need to prioritize this because the US is desperately looking for offtake agreements to help suppliers scale. We see the same on the Japanese side.

There’s already significant collaboration happening. Europe has considerable chemical and refining expertise, though much has gone dormant after moving to China over the last decade. Looking at US investments, Noveon Magnetics is basically paying Solvay, a Belgian company, with US state support to do heavy rare earth refining for magnets. The same is true for USA Rare Earths’ pipeline projects with Less Common Metals in the UK and Solvay in Belgium.

Underneath the government level, various collaborations exist because globalization is real, and we all have niche capabilities throughout the pipeline. Encouragingly, we’re even seeing movement between the US and EU — they don’t agree on much at the moment, but on critical raw materials, we at least have a Memorandum of Understanding that says all the right things about ensuring access to each other’s stockpiles, driving demand to the proper places, and creating a buyers’ club that’s large enough.

The only problem with the MOU is that it’s just an MOU — it says “we intend to,” “we explore,” et cetera. It’s still early days for implementing these measures, but these are the kinds of steps that will ultimately solve the problem.

Jordan Schneider: Farrell, what’s your perspective on this?

Farrell Gregory: If the question is about competing interests between investing in domestic industry and working with our valued international partners, I actually don’t think there’s such a simple and satisfying answer. My broader idea is that we’re in the return of history. National interest has always mattered — we just happened to ignore it for a little while. But national interest in policy, especially economic policy, is reasserting itself.

The domestic interest and access to specific materials questions aren’t necessarily always clashing. In a lot of cases — and this is something that I’ve written about for ChinaTalk before — geology doesn’t care about national borders. As much money as you might want to invest in extracting heavy rare earths, the name’s not a misnomer. Feasible deposits of heavy rare earths are actually quite rare, and if you can’t find them domestically, your only option is to work with other countries internationally.

What’s been quite interesting is some of this Pax Silica stuff coming out of the State Department, which seems quite promising, especially on this buyers club idea. International cooperation and leveraging American access to other countries for specific materials that we can’t find here make sense.

At the same time, part of the reason we got into this whole problem of supply chain reliance for essential consumer and military supply chains is because we were solely very econ-brained for a while. I don’t think econ-brain alone is going to get us out of this problem. There’s a tangible benefit to domestic industry that goes well beyond the question of China. There are particular social goods to manufacturing that aren’t really accounted for as we analyze how reliant we are on China for gallium.

My short attitude on this is that you obviously work with other countries where necessary for material access. On the question of efficiency versus social imperatives of investing in domestic industry, I do lean on the side of more investment in domestic industry, possibly at the expense of overall hyper-efficient global markets.

For instance, I expect on the European side, this is an even more potent question. We have competition between states in the US, but the competition between states in Europe, especially around these national interest questions, must be even more heightened. I imagine there’s a lot of competition between these different countries — spending German funds on German companies, French funds on French companies in rearmament. I imagine there are similar dynamics at play in whatever nascent European reindustrialization is occurring.

Jordan Schneider: What’s the main challenge facing Europe in critical materials?

Joris Teer: The main problem on the European side is a lack of money. No one is pulling the purse strings to really pay for this. We now have a French action plan that came out a couple of weeks ago that makes me a bit more optimistic — it’s focused on heavy rare earth refining and neodymium-iron-boron magnet production, trying to solve the demand issue by 2030.

A real problem we face is that we’re strictly regulated environmentally, and for good reason. Societies want clean air in Europe, and we’re committed to emissions and energy targets. These are all very energy-intensive industries. On top of that, these industries aren’t economic winners by themselves — you’ll need to keep supporting them to ensure they’re not flooded by China and that China doesn’t kill nascent production.

We’ve had the opposite problem from what you might expect. It’s not that European states are clamoring to all become the next producers of rare earths, but that not enough is being done because insufficient public money is available.

Policymakers genuinely struggle with the question of where to start. Everyone can see the logic: without the permanent magnet, there’s no drone. But the logic also applies to gallium — without it, there’s no drone. The same goes for particular legacy chips. How do you create security of supply for your end sectors? That’s been a key issue.

We have these really complicated supply chains running all across the world. There’s a degree of overdependence on China because in many fields China is not a market actor. If you look at gallium, China spent so much money on it that between 2005 and 2020, a state-sponsored producer put 31% of all the gallium they produced in a stockpile, which gave them complete confidence they could kill global prices at any point.

Looking at the gallium pipeline, the US is now getting $7 billion in combined investments from the Koreans and Americans to build a smelter in Tennessee that will produce gallium among other resources. But if we examine what gallium is used for, it’s then shipped to either Europe, Japan, or China to make gallium arsenide wafers, which are shipped back to the US and Taiwan to make various radio frequency chips that we need for guided munitions.

If the logic is that we want to onshore gallium to ensure we can build drones in the US alone, we’re still going to be dependent on gallium arsenide wafer production in Europe and Japan.

This situation is quite worrying. Because of Prime Minister Takaichi’s comments that Japan could intervene if there were a military confrontation over Taiwan, we’ve seen gallium exports to Japan reduced to zero again. This puts massive pressure on the Japanese to produce their gallium arsenide wafers, with the real risk that production capacity will now go to China.

We’re spending all this money on the upstream — we want to produce gallium — but now China’s opening a new front in the midstream, which I don’t think we can solve with the US alone, the EU alone, or definitely not Japan alone, because it’s obviously too small for this.

The Environmental Tradeoffs of Reshoring

Jordan Schneider: There’s a debate about bottom-up pushback around data centers — they’re too loud, they use too much water, they raise energy prices. Is there any way to make refining pleasant? Could we make the air smell nice, like flowers? Maybe this is another tier list you should make, Farrell — ranking the quietest options. Where can we put playgrounds on top of industrial sites? We have all these industrial ruins that get turned into art installations and playgrounds.

Farrell Gregory: In terms of environmental cleanliness, it’s worth reading about how rare earth extraction is actually done, especially in southern China and Myanmar. It involves injecting chemicals into land formations and subsequently draining out this slush that becomes the basic rare earths that go into magnets.

For whatever hesitancy we have in the US around building new infrastructure — and to whatever extent that’s even more true in Europe — I think people would find that method of rare earth production especially intolerable.

There are cleaner ways to do it. But, when we talk about reshoring and friendshoring, a lot of our expectations about the world come from living in a consumption-based, post-industrial economy. You don’t have to see how any of the consumer goods and materials we value are made. You don’t have to bear the necessary costs because they can do it halfway around the world.

I happen to think there are many moral elements to opposing this hyper-efficient global supply chain. Part of it is a more accurate reckoning with the costs and dependencies we actually have. In a lot of cases, it’s easy to be “out of sight, out of mind.” Maybe some social problems might improve if these things weren’t so out of mind.

Jordan Schneider: Once we have that metal taste in the air back over New Jersey and New York City, I can tell my kids, “This is the taste of economic independence, and you should be thankful. This is progress.”

Farrell Gregory: I think the gut feeling is that you can do these things a lot cleaner in the US.

Joris Teer: You’re completely right, Farrell. This is the dilemma we face. We don’t like the overdependence, we don’t like the economic coercion, and we don’t like how it’s used to isolate Japan and make the costs much higher for anyone to speak up in Taiwan’s favor. But it’s also true that a lot of the environmental burden for what we use has been borne by China. The people in Inner Mongolia who live next to the sludge lake certainly didn’t elect to do that.

However, this has real consequences. If we want to produce these materials more cleanly and without the massive state support that the Chinese provide, we’re going to make the inputs for our end industries more expensive. We’ll have to tell companies like Volkswagen, BMW, and GM that we want them to use American magnets or European magnets with particular standards, which will drive up their costs.

These companies face a geo-economic pincer movement. On one side, China pulls out the building blocks for their production by restricting critical raw materials, which leads to more expensive materials and intermediate products that they need to buy domestically. On the other hand, we still have large-scale Chinese subsidies and overproduction in end industries as well.

I don’t think we can get around this without also looking at end industries. If we’re going to ask our medical producers, car producers, and defense industries to use more expensive inputs, we’ll have to find a way to better protect them against Chinese competition in the end-user industries as well. A tariff approach — a replacement for what the Supreme Court struck down on the US side — is incredibly important. At the same time, what we see right now in the EU with the Industrial Accelerator Act is really a move towards greater protections against the flooding of Chinese products. This needs to move forward quite quickly to make it a reality.

Aqib Zakaria: I’m hopeful that we can find ways to be innovative about this in a way that’s not horrible for the environment and also solves the problem at the same time.

Joris Teer: I completely agree. But all of that is what’s going to raise costs for us compared to Chinese refiners and miners, which by one estimate received between $9 and $10 billion in subsidies between 2010 and 2019 alone. When you’re faced globally with two state-owned enterprises that don’t have to stick to the same rules, that get massive state support, and don’t even publish their production quotas anymore, you’re going to see that the rare earths and permanent magnets we produce — hopefully much more sustainably — are going to hike up costs for our end users. We need to protect our end users as well, because otherwise we’re just going to have the same problem in the midstream and downstream.

Aqib Zakaria: There’s always a trade-off between economic security and lower prices. We often think of rare earth processing as a primitive operation — just extracting materials from the ground and smelting or refining them. But Joris, you mentioned earlier that China has export-controlled much of the technology for refining rare earths.

What’s the technology ceiling here? Is there a lithography-level moat in rare earth refining like we see in semiconductors? And is there significant room for American and European innovation to make refining more efficient and clean — potentially allowing us to compete against Chinese subsidies or at least reduce costs?

Joris Teer: That’s an incredibly pertinent question, and I’ve received contradictory answers from industry sources. Let me share a few key data points.

First, the Financial Times recently reported that US defense companies are “clamoring” to delay the defense ban on Chinese permanent magnets. This ban was supposed to take effect in January 2027, but apparently we’re still far from ready even for defense applications.

Second, the Trump-Xi meeting readout from the US side states that “the Chinese side will address the concerns of the US side of not shipping out key rare earth production technologies.” Essentially, the US is pleading for access to these technologies, many of which have been banned since 2008 — long before the lithography controls. This isn’t an encouraging sign.

As for where industry actually stands, it’s difficult to ascertain. As of April 2025, when China tightened heavy rare earth controls, there was no commercial-scale refining outside of China — a 100% dependency by all accounts.

We’re hearing mixed signals. Lynas has reportedly made significant progress with heavy rare earth refining in Malaysia. The CEO of Solvay, the famous Belgian company, gave an extensive interview to a Dutch newspaper claiming, “We can refine all 17 rare earths. You just haven’t created a business case for us.” He added that the Chinese can simply turn on the tap again and kill any attempts we make, so he won’t make the long-term investment.

The picture is extremely mixed. This is a critical question that needs answering, and I don’t have a definitive response.

The Strategic Race for Industrial Capacity

We also haven’t discussed the deterrent side much, which really worries me. When you put this all together, you hear different things. The International Energy Agency just came out and said we’re nowhere near fixing even the permanent magnet problem before 2035. You see some more hopeful signs, but regardless, it’s going to be 2028 or 2029 at the earliest for many materials — and even then only in small volumes.

A lot of bombs are being dropped on Iran. Those need to be replaced. It’s not just the US defense industrial base — we’re also buying a lot of defense systems. You did extensive podcasting, Jordan, on “No Ammo for Taiwan” — this undergirds all of that.

How are you going to ensure in the short term that you put enough pressure on China to at least get the materials you’re still receiving? In the Chinese export control clause, there’s an automatic denial if you write that you’re buying critical raw materials for defense industrial users. What does this mean for the actual defense replenishment that needs to happen in the US and the rearmament in Europe?

This is a key question I’m struggling with. If you listen to interviews with the CEO of Rheinmetall, he says, “We have rare earth stock for about a year, and I insist on being updated weekly on this.” I’m not sure how this is affecting the many shortages we already face and the $32 billion arms delivery backlog to Taiwan.

How do we deter China to ensure that, at least for the time being, we’re getting part of the critical raw material supply — that they don’t give us the Japan treatment of limiting exports to zero, which they’ve done to Japan for the last four months? It’s a pertinent question because if you don’t ask it, you might find yourself in China’s endgame where they’re confident they can put much more pressure on Taiwan, perhaps even a quarantine, because of production issues in our defense industrial value chains.

Jordan Schneider: Farrell, on your side, why don’t you talk about how various emerging technologies are changing the appetite? Joris’s missile concerns are relatively fixed and predictable, but what are robots and the data center buildout doing to change the chessboard here?

Farrell Gregory: The change that novel technologies are producing is almost making our reliance on China less of the problem — though obviously it’s still a problem.

If you look at projections for how much copper we’re going to need, how many foundational materials and building supplies we’re going to need for the AI buildout, and what kind of increase you’re going to see in rare earth consumption — already a pretty tight supply chain — for different robotics applications, the picture is concerning.

In the future, we’ll see how things go in Europe and the US in cultivating these supply chains. Regardless of how that goes, if you’re not going to see less reliance on China as an issue, at the very least you’re going to see scarcity for a lot of these materials as an issue.

Now, obviously you don’t get Malthusian about drawing straight-line projections — we’re not going to be able to come up with novel efficiencies. We probably will. But it’s worth acknowledging that we’ll need either new materials, new efficiencies, or at the very least something, because we have this huge wave of demand coming towards us, and we’re all still fighting about who has access to which supply chain.

Jordan Schneider: This discussion helps put the issue in perspective — it’s not just an isolated problem. One dynamic I’ve been hearing about in the American context — and I’m curious how this works in Europe — is energy. Refining is a pretty energy-intensive process. We’re not just trying to get refineries online; data centers are also choking the grid. We’re having to compete for energy with all these other factors in the economy. How do we balance funding and production of rare earths versus the things that need rare earths?

Joris Teer: You’re completely right. One underappreciated bottleneck is skilled labor. Even in the JD Vance and Marco Rubio announcements of Project Forge, the US government had to admit we’re only graduating around 200 mining engineers per year — hardly ideal if you’re trying to onshore or friendshore so many different critical raw materials.

There are many constraints, which is why allied cooperation is the only way to do this. We’ll have to make use of comparative advantages between allies. Europe has heavy rare earth refining expertise. We have the gallium arsenide wafers — the key link in the value chain to all these essential semiconductors. The United States was smart enough to reopen the Mountain Pass mine in California within the 2010s and actually start producing rare earths again. Within these constraints, we can make all the puzzle pieces fit together.

What we’re promoting is basically allied autonomy and European indispensability. Allied autonomy means these key strategic bottlenecks need to be moved out of China. From a European perspective, this is crucial because China is the decisive enabler of Russia — a direct threat to many of our member states. But it’s also because of what happened last year with export controls.

The indispensability aspect is hyper important, not just from the European perspective. Having companies like ASML, having sizable production of memory chips in Korea and Japan, having photoresists produced in Japan — these give us levers toward China to keep its coercion relatively in check.

This has probably been a bigger failure than the de-risking part. Despite everything China has done over the last year — the Busan deal was only a partial victory because China kept spying via export licenses and capping rare earth exports — we haven’t been able to make a credible counter-threat to bring this back online, even short-term. That’s really a point of failure that hopefully will change in the coming years.

Farrell Gregory: What Joris said reminds me of a phrase we’ve heard particularly from the State Department and their Substack — the idea of the US and Europe as civilizational allies. It seems like we’re in the process of defining what that looks like in concrete terms.

This industrial relationship between the US and Europe is actually a pretty good example of what that might look like. With what you described earlier about redundancies between having US-specific supply chains for all these materials, is it really desirable or even feasible to have a Europe-specific ecosystem for all these things in addition to the Chinese and US ecosystems? My gut feeling is that it’s probably not feasible. It’s probably not even desirable.

Joris Teer: In Europe, as you may understand, we’ve become quite allergic to these civilizational terms because the National Security Strategy of the United States says — the words used were “civilizational erasure” — that is what we’re currently undergoing in Europe. There are all sorts of disagreements and pain points in the US-EU relationship.

My ideas for allied skill and for allied autonomy — European indispensability — were very difficult to sell here in Brussels when the threat of annexation about Greenland was on the table last January. And during the trade pact as well.

I see it more as other rhetoric we’ve also seen from the US side, namely an interest-based approach. How do we make sure that we have the key building blocks that we need for the MRI technologies, the pacemakers, the fighter jets, the energy grids, et cetera?

I’m convinced that the European-alone approach will not work, and I’m even convinced that a slightly larger G6-plus-key-partner approach will be very difficult to work without the US, given how ingrained the US is in many of these productions.

From an interest-based perspective, we just need to move forward. Also within defense industrial value chains — the Finnish Prime Minister has just announced he’s buying, I think, 50+ additional F-35 fighter jets. The idea that we’re going to disentangle all of this and the dependencies that are also there on the US side — particular parts being produced in Europe or European refining technologies for rare earths — is not going to disappear anytime soon.

I like the allied alignment. I think it’s necessary. I feel very sorry that the US-EU relationship is in such a poor state, but my assessment is that we don’t need a grand ideological narrative. I don’t think it will go over well here. We need cold, interest-based cooperation on this because we both know we’re a lot better off if China doesn’t hold these choke points and these kill switches over our economies.

Farrell Gregory: I agree there’s a lot of complementarity between the dependencies the US has on Europe and likewise. To revive my stand against econ-brained analysis, I do actually think the ideological argument — whether or not it has sway in Europe — is true. The civilizational descriptions do identify something real and something that matters well beyond the industrial compatibility on this material or that mineral.

Joris Teer: That might very well be right. I’ve been focusing recently on communicating my critical raw materials perspective, so I’ve chosen rhetoric that’s somewhat removed from that.

A postscript from Joris Teer: I grew up in Waalre, which is a tiny village just south of Veldhoven and Eindhoven. I live just a bike ride away from ASML’s key production sites — the facilities that produce the systems enabling our entire digital life to function.

It’s surreal when you think about it. If you were writing a science fiction novel and said, “There’s this somewhat rural province in the south of the Netherlands — though it’s not so rural anymore — and they produce machines that manufacture 90% of all chips worldwide, chips essential not just for our weapon systems but also for AI and everything else,” it would seem far-fetched. Yet that’s our reality.

My grandfather was actually recruited after World War II from the Technical University to move to the south of the Netherlands. They had a brilliant physics lab there with funding to experiment and discover new things. There’s a line — not a straight line, but a clear connection — from the work he did then to our current position as this incredible node in the international production system for essentially all technology.

The midstream point is the one I keep coming back to. Subsidizing mines doesn't help much when China can flood the market and bankrupt whoever you funded — so the binding fix is demand-side: guaranteed offtake and price floors, like the Pentagon's $110/kg floor with Lynas and MP. That's what lets a Western refiner invest through a Chinese price war. And your guests are right that the squeeze has moved from the mine to the wafer-and-magnet step — the narrow part that takes years to rebuild. Funding the dig is easy; funding the midstream and guaranteeing it a buyer is the whole game.

the 25-mineral framing is the right one. but the harder question is sequencing: china does not restrict a material until it does not need to export it anymore. gallium was maybe 40% of global supply when the japan restrictions hit. china already had the downstream fab capacity lined up. the restriction was an exit visa, not a siege.