The Empire of Wuxi

China's Biotech Giant

Lucas Fluegel and Nick Corvino team up to tackle Chinese biotech. Lucas is a visiting scholar at the Carnegie Endowment for International Peace, where he explores biotech and biosecurity policy. He did his Ph.D. research in biochemistry and bacterial genomics at the Scripps Research Institute.

China wants to be the world’s biotech superpower. But to understand how it got here, it’s best to start with its crown jewel: the WuXi companies.

The WuXi companies are the dominant biotech services consortium in China and have become the lightning rod of U.S. political wrath, most notably as an early target of the BIOSECURE Act.

When we say “WuXi,” we don’t just mean WuXi AppTec. Although this family of companies is often spoken about as if it were a single company, in reality, it is a group of companies comprised of WuXi AppTec (药明康德), WuXi Biologics (药明生物), and a set of tightly integrated businesses, all more or less under the same leadership but dispersed throughout the industry. Together, they are stronger than the sum of their parts, and form what we envision as the Empire of WuXi (hereafter just “Wuxi”).

The TSMC analogy is tempting, since just as TSMC manufactures chips for companies like NVIDIA and AMD, WuXi, instead of discovering and commercializing its own blockbuster drugs, it provides the services (chemistry, testing, manufacturing) that allow others to do so. And both have the ability to gut-punch the global economy if their employees stop coming to work.

But AI analogies, tempting as they are, can do more harm than good. TSMC sits at a true chokepoint, with essentially no major rivals. If you want cutting-edge chips, you go through Taiwan. But WuXi does not monopolize a single irreplaceable step in the biotech supply chain. In fact, it has strong competitors both in China and globally.

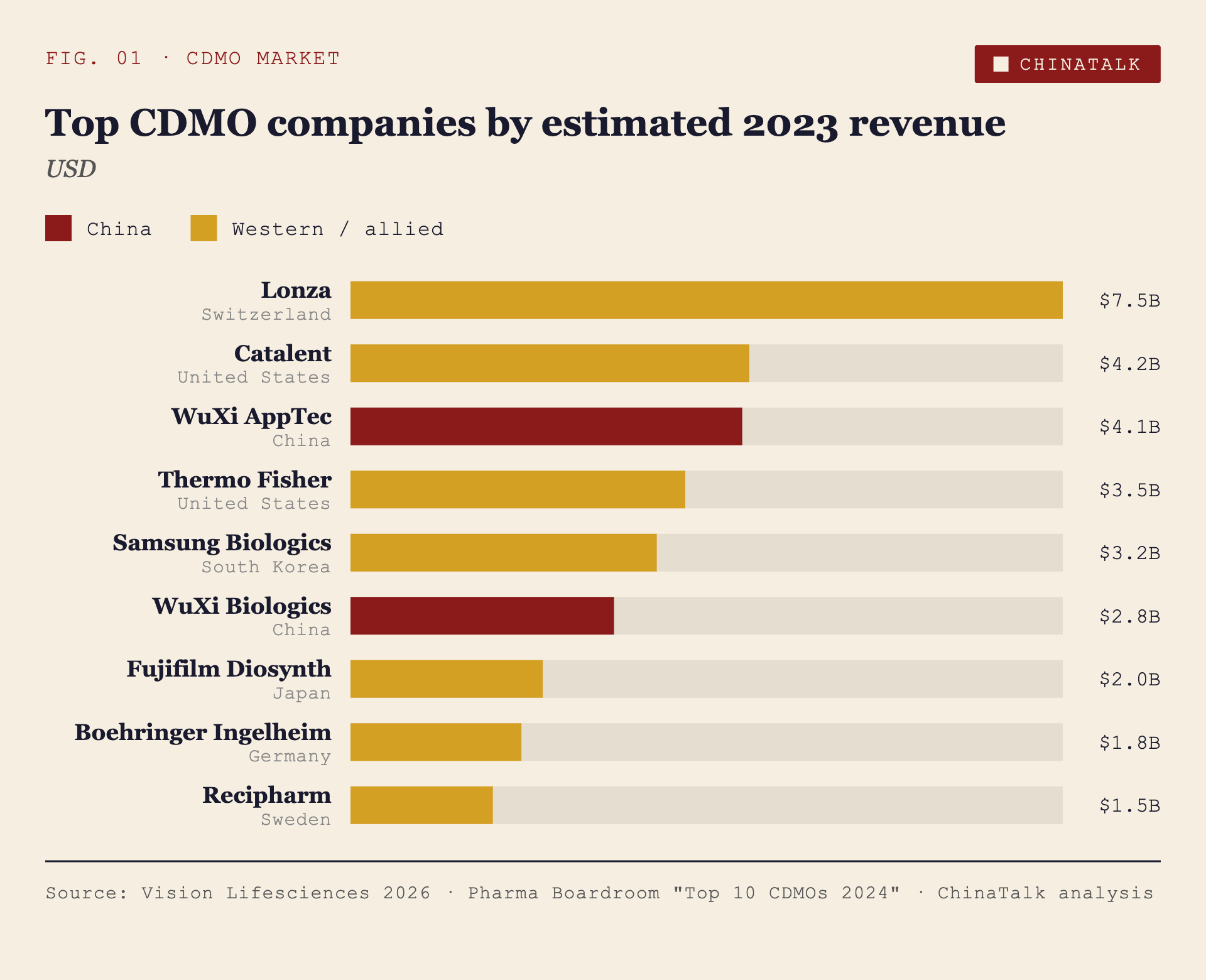

WuXi AppTec and WuXi Biologics are the third- and fifth- largest contract development and manufacturing organizations (CDMOs) in the world by revenue. The remainder of the top ten are all based in U.S. partner nations, including the top two of Lonza (a Swiss company) and Catalent (a U.S. company). So, if there are plenty of alternative companies in U.S.-aligned nations, why is WuXi such a bogeyman for the U.S.?

In the same way that China’s rare earth stranglehold matters because of where those minerals sit in critical supply chains, WuXi, with its unique corporate structure, is embedded at many layers of the biostack. It has accumulated a structural indispensability that is harder to replace than a single dominant manufacturer would be.

A 2024 survey by the Biotechnology Innovation Organization estimates that 79% of US biopharma companies have at least one contract with a Chinese CDMO or CMO. WuXi AppTec alone is estimated to be involved in roughly a quarter of all drugs used in the United States (according to WuXi). And an estimated 65% of WuXi AppTec’s total revenue comes from U.S.-based clients.

Even if the U.S. and its allies lead in certain sectors of biotech, the growing recognition that WuXi has embedded itself throughout the supply chain has raised concern about systemic dependency and the leverage that comes with it.

The U.S doesn’t have an easy way to address this. China’s specific advantages in biotech look less like control over a single node and more like what it achieved with its manufacturing sector. It is about process expertise, cost efficiency, labor and talent, and deep integration into global supply chains — perhaps more like BYD’s success in the EV sector. These are not easily reducible to export-controllable chokepoints.

The biotech landscape is much more diffuse than AI. And yet, perhaps because of the TSMC analogies, Washington has increasingly tried to map its AI playbook onto biotech, with early versions of the BIOSECURE Act explicitly targeting WuXi as it would a company like Huawei.

We’ll get to the geopolitics at the end, but let’s first explore where WuXi came from and why they are so unique, before returning to how U.S. policymakers might approach the emergence of Chinese biotechs.

The Origins of WuXi: A Chinese–American(?) Story

The seeds of the WuXi empire were planted at a moment when it was relatively easy to build companies that straddled the U.S. and China.

Wuxi’s founder, Li Ge (李革), is emblematic of a particular early-2000s generation. Educated at Peking University, he earned his Ph.D. in organic chemistry from Columbia University and went on to become a founding scientist at Pharmacopeia, a U.S. biotech built around combinatorial chemistry.1 By the late 1990s, Li was fully embedded in the American biotech world, becoming a naturalized U.S. citizen. He is also very charismatic and speaks fluent English, meaning you’d often see him on TV segments talking to Western reporters:

And yet, like many in that cohort of returnees — the so-called “sea turtles” (海归) — he felt pulled back to China.

Around 2000, during business trips back to China, Li noticed something that is fairly obvious in retrospect but was underexploited at the time. China had a large pool of well-trained, low-cost chemists, while Western pharma companies were steadily increasing their appetite for outsourced R&D, driven by the rising cost and complexity of drug development. Bringing a new drug to market was getting more expensive as the low-hanging fruit had already been picked, older blockbuster drugs were losing patent protection, and the revenue that funded new research was starting to dry up. Outsourcing was the pressure valve, letting companies chase more drug candidates without expanding their own overhead. At the same time, China’s entry into the WTO and improving IP protections were making it newly viable to plug into the global pharmaceutical system. As Li later put it:

“Around 2000, as China prepared to join the World Trade Organization, intellectual property protection in the Chinese pharmaceutical industry significantly improved. I realized that Chinese pharmaceutical companies definitely needed to develop new drugs.”

He founded WuXi PharmaTech in 2000 with his wife, Zhao Ning (赵宁). Pharmacopeia, his former U.S. employer, became its first client.

From the beginning, WuXi PharmaTech was built as a cross-border company. It served Western customers, adopted international standards, and quickly oriented itself toward global markets. In 2007, it listed on the New York Stock Exchange, becoming one of the first Chinese biopharmaceutical companies to do so. However, WuXi PharmaTech later restructured, delisting from the NYSE in 2015 before relisting WuXi AppTec on the Shanghai Stock Exchange and Hong Kong Stock Exchange in 2018, alongside a separate Hong Kong listing for WuXi Biologics (药明生物) in 2017 and, more recently, WuXi XDC (药明合联).2 Wuxi made a series of correct bets on when to embrace the Chinese and American markets, respectively. Even today, although transparent data post-BIOSECURE is scarce, an estimated two-thirds of WuXi’s revenue comes from U.S.-based customers.

A key inflection point for WuXi is the 2015 reform of China’s drug review and approval system. By decoupling drug approval from manufacturing and encouraging outsourced production, the reforms accelerated a feedback loop: more innovative drugs → more R&D → more outsourcing → more innovative drugs, and so on. WuXi expanded aggressively to meet that demand and become the titan it is today, including earlier moves like its 2008 acquisition of a U.S.-based AppTec business, which gave it both new capabilities and a physical foothold in the American market (and the name of its most famous company, WuXi AppTec).

WuXi was not alone in embodying this Chinese-American model. Asymchem (凯莱英) was founded by a Western-trained Chinese scientist who returned to Tianjin and built a contract services platform. Porton (博腾), based in Chongqing, likewise evolved into an internationally oriented pharma services company with a large U.S. footprint.

For years, this dual positioning was an asset. The intertwinement of the U.S. and Chinese biotech systems was not accidental but foundational to WuXi’s rise. Western pharma outsourced to China for cost and scale; Chinese firms like WuXi grew by serving those needs. You could argue that this was exactly the outcome the U.S. wanted before it realized how powerful China would become.

That equilibrium has since come under strain. In early 2024, after being named in the initial BIOSECURE Act proposals, WuXi’s stock plunged sharply, wiping out tens of billions in market value in a matter of days. Although some of those losses have since been partially recovered, WuXi is now a target of the U.S., and its future is highly precarious.

A generation of Chinese biotech companies emerged from this earlier era of integration, commercializing Western training and global demand through China’s industrial base. But WuXi remains the most internationally salient and successful of them all.

Why?

What Makes WuXi So Good?

Li’s vision for WuXi’s role in the pharma business ecosystem was explicit from early on. WuXi was not meant to be a traditional drug company, but an enabling platform for global innovators. Rather than designing drugs, they would build the infrastructure needed to quickly find and develop them. The novelty of this business model was not simply exploiting wage arbitrage — U.S. and European pharmaceutical companies already knew how to outsource chemistry. Instead, Li’s key insight was to reframe the role of contract R&D in the drug development process.

Traditionally, outsourcing drug companies would partner with different contractors for each step of drug development. WuXi provided an enticing alternative. Instead of contracting one company to test the initial drug, another to optimize its potency, and another to manufacture it at commercial scale, drug companies could work with WuXi through the entire pipeline.

Li would later define this approach as an “open-access platform” (开放式平台). Unlike more siloed competitors, WuXi was committed to “following the molecule” as it progressed from the research laboratory to regulatory approval and commercialization. This business model would later be codified as a “contract research, development, and manufacturing organization” (CRDMO) and copied by other companies.

This approach is a win-win for both parties. For the drug developer, it minimizes the need to switch between different corporate ecosystems, eliminating the inefficiency of juggling multiple contracts and ensuring each partner is up-to-speed. For WuXi, it incentivizes customers to stay “stuck” to their services for years, leading to predictable business and access to the revenue scaling that occurs as the drug progresses towards commercialization. Given the immense uncertainty involved in pharmaceutical development, this level of stability for provider and customer is extremely attractive.

WuXi doubles down on this model by targeting a “long tail” of biotech customers. Rather than limiting themselves to massive deals with the pharmaceutical giants, they target many small- and medium-sized firms. With more limited resources, these small companies benefit particularly from the cost efficiency of WuXi’s end-to-end services, which then locks them into the pipeline. Their sheer number and diversity also diffuse the risk of major damage from any one customer pulling out. Furthermore, research by consultancy firms has shown that these smaller companies tend to produce more innovative drug leads than their big pharma counterparts. WuXi is therefore able to link itself to these disruptive — and therefore lucrative — products early on. These strategic decisions have given WuXi a “strong, diverse, and sticky customer base.”

Does WuXi have a technical moat?

Importantly, however, these technologies didn’t originate from WuXi labs. So, unlike the TSMC analogy, there is not a WuXi-specific technological moat around their services. Instead, WuXi’s biggest competitive advantage lies in their integration across the technology stack.

Indeed, a quick scan of their advertised capabilities reads like a catalog of the hottest frontier capabilities in drug development. A company can use WuXi’s DNA-encoded libraries to quickly scan for usefully potent molecules, including with options to avoid sharing IP. Biomanufacturing for complex biologics has been standardized and optimized, with new methods being deployed to further boost productivity at scale. In-house expertise in finicky drug types like peptides (including GLP-1s), antibody-drug conjugates (an expanding class of mainly anticancer drugs), and monoclonal antibodies (of COVID-19 treatment fame) expands the customer base they can serve. And, of course, AI and automation are being deployed throughout the pipeline.

Most biotech and pharmaceutical firms lack the resources and expertise to deploy these advanced biotechnologies in-house. But WuXi’s comprehensive and integrated platform offers them the access and support needed to compete at the technological frontier. A positive feedback loop is born as WuXi aggressively invests in further optimization and expansion, and the platform becomes even more attractive to the next wave of ambitious firms.

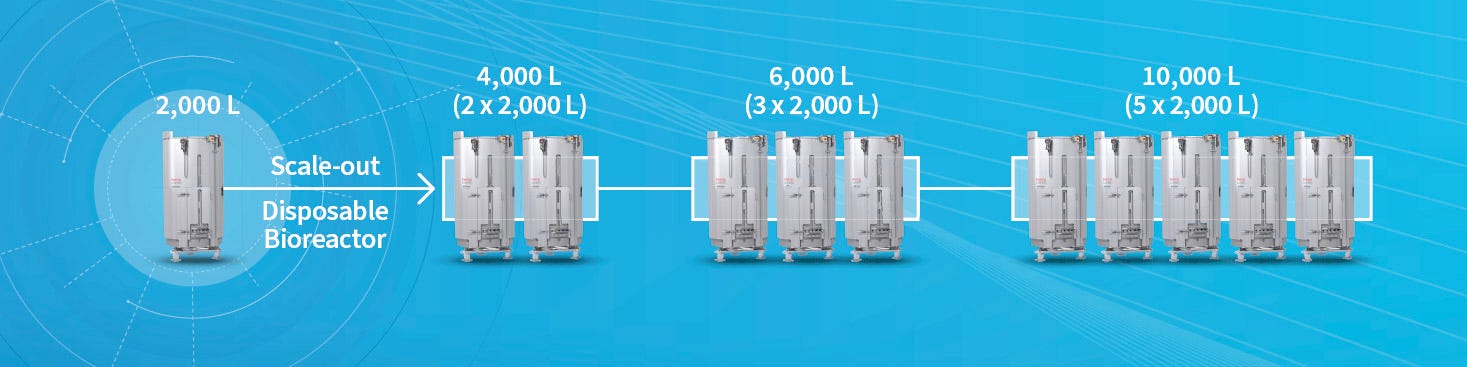

An excellent example of WuXi’s ability to adopt and deploy new technologies is their development of the “scale out” paradigm for manufacturing biologic drugs.

Biomanufacturing – the use of a living system or its parts to produce a good – is central to many of WuXi’s higher-end pharmaceutical manufacturing processes. The key step in a biomanufacturing process is growing the organism that makes your desired product in a large vessel, called a bioreactor. Traditionally, scale-up of these processes would proceed linearly, moving gradually to larger bioreactors until the necessary commercial scale is attained.

But the conceptual simplicity of this approach hides many downsides. Bigger bioreactors change the physical processes within, often leading to unexpected engineering problems like poor stirring or slow oxygen transfer. Product yields are compromised, requiring expensive and time-consuming optimization at each stage. Simultaneously, the capital expenditure and financial impact of contaminated batches scales with the bioreactors.

WuXi sidestepped these challenges. In place of building >20,000-liter tanks, they run multiple 2,000- to 4,000-liter reactors in parallel: scaling out instead of up. By doing so, the same proven operational conditions are used at small and large scales. Making more or less of a product requires no additional engineering — simply add or subtract bioreactors. The separation of one production run into several batches also ensures that one contamination event does not spoil the entire campaign. WuXi’s adoption of single-use disposable systems that don’t require meticulous cleaning between runs has simplified operations even further. Though not the first to develop these technologies, WuXi was the first to pioneer it as the backbone of a commercial-scale manufacturing capacity.3

WuXi’s China Advantage

Deploying these suites of frontier technologies and large-scale manufacturing facilities is expensive: WuXi Biologics’s massive Singapore facility reached a price tag of $1.4 billion. But some of this financial pain is offset for WuXi by the favorable political and economic landscape of China’s science and technology sector.

The most critical advantage is the Chinese workforce. Chinese universities produce dramatically more STEM Ph.D. graduates than their U.S. counterparts. WuXi capitalizes on this geographic concentration with targeted training programs that attract top candidates and develop company-specific skills. WuXi also invests in training workers at every level of the production process, including the technicians and operators running factory floors. This is precisely the kind of vocational and technical workforce development that the U.S. has chronically underfunded and undervalued. Because this highly skilled Chinese talent is often half the cost or less than Western equivalents, companies like WuXi can deploy larger teams to shorten timelines and overcome obstacles.

WuXi also benefits from China’s established excellence in advanced manufacturing. Because China largely controls global production of raw materials and active ingredients for small-molecule pharmaceuticals and is rapidly domesticating the supply chain for biologics, domestic companies benefit from easier sourcing and more resilient supply chains. This colocalization directly translates into accelerated procurement and lower overhead costs.

These advantages are compounded by the central government’s aggressive championing of biomanufacturing, such as labeling biomanufacturing a national priority and doling out subsidies.

Overall, this investigation shows that WuXi’s success is not a result of some unassailable technological lead in a core competency area. Instead, the well-rounded profile of the company means there is no singular source of advantage. This fact presents an unusual problem to concerned policymakers, who have been struggling to figure out how to deal with WuXi for years.

The Geopolitics of WuXi

Led most prominently by the National Security Commission on Emerging Biotechnology, the U.S. is racing to determine how to maintain its competitive edge in biotech in the face of rising Chinese pressure. The threat of losing the advantage in innovation or a cutoff of basic medicines has policymakers searching for options. The size and success of WuXi has naturally caught their attention.

The BIOSECURE Act is the most notable move. It prevents the use of federal dollars to pay for goods or services from biotechnology companies of concern. In the earliest versions of BIOSECURE, WuXi AppTec and WuXi Biologics were both explicitly targeted. By pushing U.S. companies away from contracting with WuXi, it was hoped that new and more U.S.-aligned firms would step up to fill the gap.

However, the explicit naming of companies was abandoned in the final version of the Act that was passed as a part of the 2026 NDAA. Given how much pain this would have cost U.S. firms, since WuXi is embedded in a quarter of all drugs in the U.S., quitting cold turkey would have been painful.

Unlike with restricting AI components, where slowing progress would be felt years after implementation (and might even be welcomed by Americans already anxious about the technology), the costs of disrupting access to cancer drugs or GLP-1s would be immediate and personal for Americans.

Instead, companies of concern are determined by a deliberative process led by OMB or inclusion on the DoW’s 1260H list of “Chinese military companies”. Unusually, the 2026 version of this list was released for only a short time before being quickly removed from the Federal Registrar. WuXi AppTec was included on this since-removed update, despite being absent from previous versions. So, though the pathway is different, it does seem that BIOSECURE is poised to target WuXi after all.

Implications for U.S. Policy

The U.S.’s policy response to WuXi is an interesting piece of the broader U.S.-China biotech puzzle. Here are a few loosely-held takes:

Take #1: It seems the U.S. policy apparatus is using this company-banning/targeting approach because of its familiar success from AI. But, because most of WuXi’s advantages don’t come from any particular technology lead, does this approach really apply in this situation?

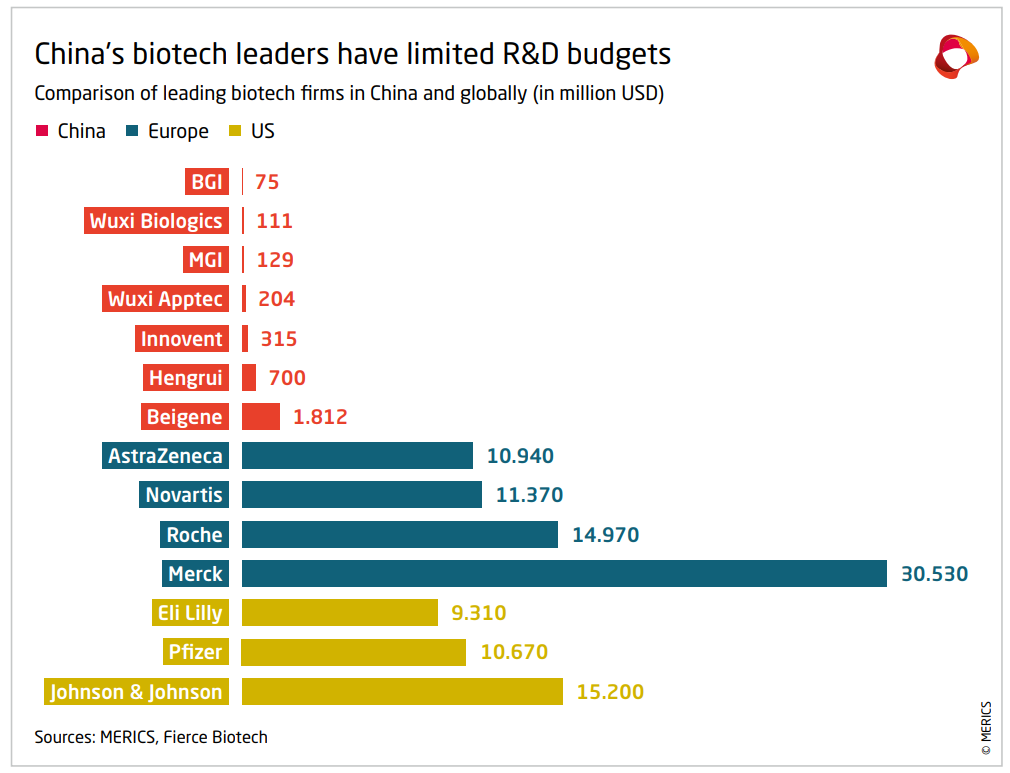

Take #2: The U.S. is quite concerned that China is “catching up” in biotech despite spending far less on relevant R&D:

To us, this suggests that the geostrategic competitive pressures we want to address aren’t primarily about money. If Chinese firms are making important moves with only a fraction of our budget, then whatever advantages they’re exploiting are probably not going to wither away if we further restrict funding. Instead, it seems like we need to think more creatively about how we can race further ahead instead of only worrying about how to slow down our competitors.

Take #3: It’s unrealistic to expect the U.S. to unilaterally dominate every layer of the biotech stack. The U.S. remains a global powerhouse in biotech, occupying advantageous positions across the entire technology stack. But, China is a massive country with a well-educated workforce that has decided to focus major investments into biotech – it’s inevitable that they will become an influential player. Perhaps the right question isn’t how we eliminate Chinese participation in biotech globally but which specific capabilities, if ceded, we could live with.

No single country is waiting to absorb WuXi and China’s cheap and diffuse biotech role. India has a large base of FDA-approved facilities, competitive costs, salaries about half of China’s, and a large and growing Ph.D. pipeline. It has thus received a surge of inquiries from U.S. pharma eager to diversify away from China. However, most of India’s strength is concentrated in small molecule generics, a very different skill set from the complex biologics manufacturing that makes up so much of WuXi’s value. South Korea’s Samsung Biologics is strong on biologics (rivaling WuXi Biologics), but weaker on the small molecule CRO and chemistry services where WuXi AppTec has built its deepest moat. No single country or company can replace all of the different roles WuXi plays, but if the U.S. leveraged its multilateral relationships to build a coordinated alternative across trusted partners, that would be its best shot, something Trump 2.0 has moved against.

The uncomfortable truth is that a U.S. biotech industry fully decoupled from China would be a slower and more expensive one. Policymakers need to be honest with themselves about that tradeoff, unless they think Americans will be fine with fewer cancer drugs for the foreseeable future.

Combinatorial chemistry is essentially the idea that instead of testing one drug candidate at a time, you build a massive library of thousands of slightly different molecules all at once and screen them simultaneously to see which ones have the properties you want. Before this, drug discovery was painstaking. You had to synthesize a compound, test it, synthesize the next one, test it. Combinatorial chemistry turned it into something more like casting a very wide net, and it was considered a major breakthrough in the 1990s for the speed it promised to bring to early-stage drug discovery. Li absorbed this philosophy of scale and throughput at Pharmacopeia, and it shows in how he built WuXi. The entire open-access platform model is premised on the idea that doing more chemistry faster and cheaper, for more customers simultaneously, is how you win.

Li attributed the decision to frustration with Wall Street’s short-termism after WuXi’s stock dropped 20% on earnings day despite strong revenue growth. But the move coincided with a wave of Chinese government policy changes explicitly designed to encourage U.S.-listed Chinese firms to return to domestic markets, and the $3.3 billion take-private was backed by a consortium of Chinese institutional investors, including Hillhouse Capital, Boyu Capital, Ping An Insurance, Legend Capital, Yunfeng Capital, and the international arm of Shanghai Pudong Development Bank. A subsequent shareholder lawsuit (Altimeo v. WuXi) alleged WuXi had concealed plans to relist subsidiaries in Asia all along. Even though the case was dismissed, WuXi Biologics listed in Hong Kong just nineteen months after the buyout closed, and WuXi AppTec followed twenty-nine months after that, both at significantly higher valuations than WuXi had achieved on the NYSE.

Of course, there is a tradeoff: at very large scales, running one massive bioreactor is often cheaper than an equivalent volume of smaller bioreactors due to economies of scale. But, because these are higher-margin, lower-volume pharmaceutical products, this modest inefficiency does not seem to severely damage WuXi’s–or its customers–bottom line.

Great read. What fascinated me was that this is not merely a story about Wuxi or manufacturing. It is a story about how industrial ecosystems compound over decades until they become nearly impossible to replicate elsewhere.

People often discuss technological dominance as if it comes from one breakthrough company or one brilliant policy. But systems rarely work that way.

What China appears to have built in places like Wuxi is not just capacity, but dense interdependence:

universities, suppliers, logistics, local governments, skilled labor, financing, tacit knowledge, and rapid feedback loops all reinforcing one another simultaneously.

This is a lucid exposition of Wuxi's rise. As you correctly state there is no moat per se-I'd argue that the closest western company is ThermoFisher-although that is a conglomerate (Wuxi's direct competitor Patheon is a business within the corporate umbrella), plus Lonza. The attraction of Wuxi lies in its "follow the molecule" strategy from its early discovery phase through to commercial manufacturing, coupled with the breadth of offering. In the Pharmaceuticals business technology transfer between CDMOs is a source of real technical risk therefore a single point of contact is clearly a boon for the emerging biotech sector.

Western companies will always be at a cost disadvantage compared to Wuxi and the Indian CDMO sector simply doesn't have the scale or reliability to effectively compete.