Transmission Dominance with Chinese Characteristics

Comparing the US and China Transmission Buildout

Dana Golden is an economist at Argonne National Labs.

The views and opinions expressed in this article are solely those of the author in her personal capacity and do not represent, reflect, or imply the official positions, policies, or viewpoints of her employer, Argonne National Laboratory. This article was completed and submitted in April 2026, prior to the author’s employment with Argonne, and any analysis, conclusions, or statements contained herein were developed independently and outside the scope of her current role.

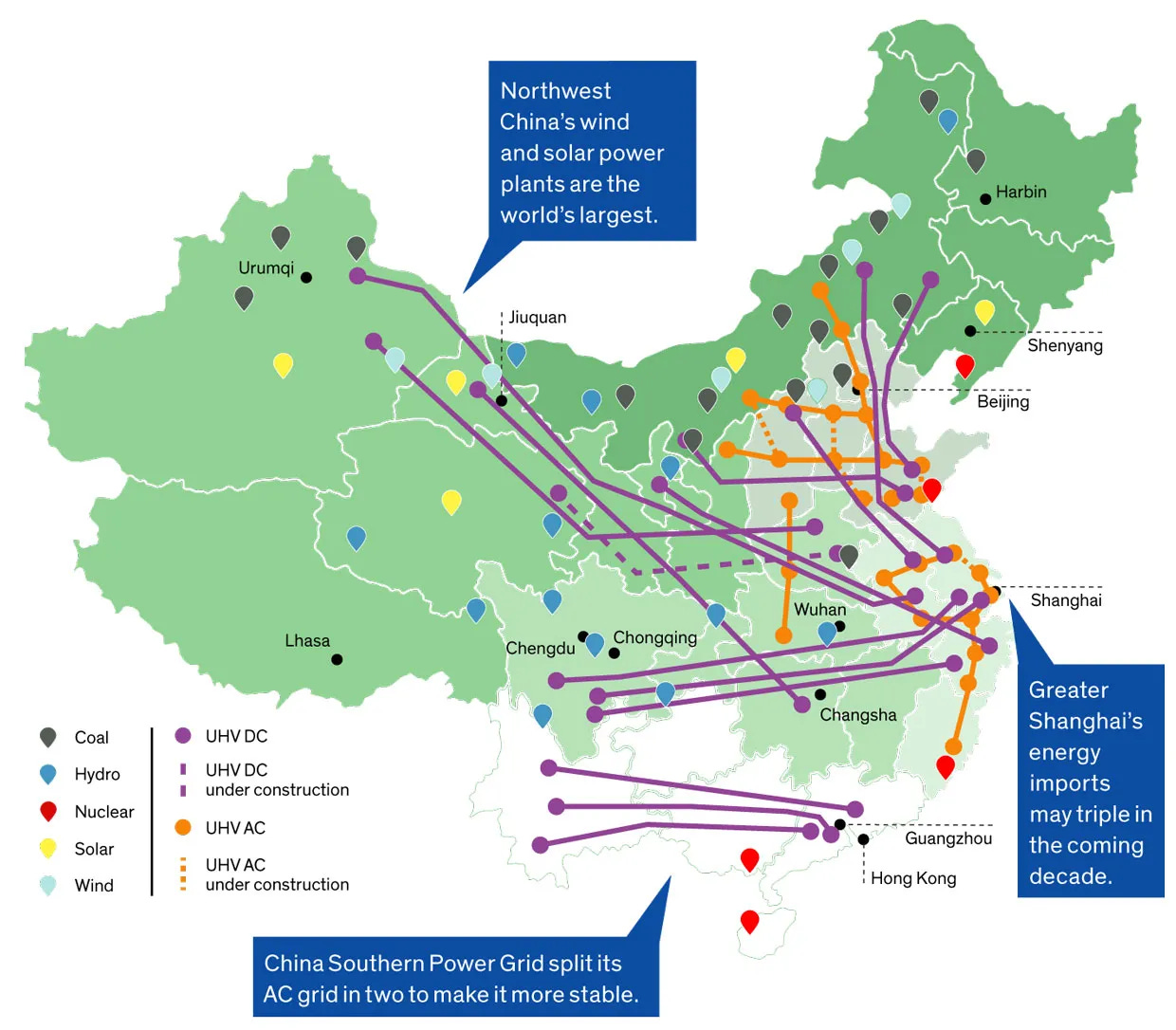

China has built more high-voltage transmission in the last fifteen years than the United States has in its entire history. This is not hyperbole. China has both the most HVDC lines and the longest HVDC line in the world. The 3,293-kilometer (2,046-mile) Changji-Guquan 1,100 kilovolt (kV) ultrahigh-voltage direct current (UHVDC) link runs all the way from the Xinjiang province in Western China to Anhui province near the East Coast and is capable of transmitting 12,000 megawatts (MW). This is roughly equivalent to transmitting enough energy to power 8 million homes from California to Illinois.

During the 14th Five-Year Plan period alone (2021–2025), China’s ultra-high voltage DC transmission network grew from roughly 28,000 kilometers to more than 40,000 kilometers. As of late 2025, the country has 45 UHV projects in operation. These projects mostly run at 800-1100 kV, almost unheard of in the United States. The extensive project list includes 19 UHV AC lines and at least 23 UHV DC lines. Quite a remarkable buildout considering the grid in China was almost nonexistent at a national level in the early 2000s.

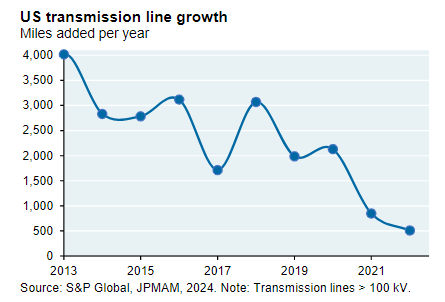

Compare this astonishing buildout to recent development in the grid in the United States, and you immediately see the disparity between investments. The US has built a scant 2370 miles (3810 KM) of HVDC lines. The longest such line is the 846-mile Pacific DC Intertie from Oregon to Los Angeles. It seems almost ironic that the country that built the first commercial power plant and started with an almost entirely DC grid at the cost of at least one dead elephant has fallen so far behind in investments in DC lines. The United States added just 55 miles of high-voltage (345 kV+) transmission lines in 2023, down from an annual average of about 1,700 miles in the early 2010s.

Notably, several new HVDC projects are in the works, including the Grain Belt Express, an 800-mile 600 kV line designed to transfer 5,000 MW from wind-rich Kansas to the Midcontinent Independent System Operator in Illinois and onto the PJM interconnection and a 765 kV regional backbone expansion in the Southwestern Power Pool. Despite recent funding cuts to support for the Grain Belt Express and similar transmission projects, HVDC buildout has continued as planned. However, interregional transmission continues to be remarkably weak — just as the grid is facing its greatest challenges in decades.

As the graph below — based on the S&P Global grid project additions dataset — shows, transmission line growth hit a peak for the 21st century in 2013 and has fallen off a cliff ever since. This would not be a problem for a grid with mostly fossil fuel generators that can be sited near load, but it is a serious problem for a grid that increasingly depends on geographically dispersed renewable resources.

The standard explanation for this gap mirrors the rest of the discourse in the space. The US is bringing lawyers and environmental impact assessments to an engineering fight. China can exercise eminent domain efficiently while the US has these pesky property rights. Authoritarian regimes build infrastructure while democracies endlessly litigate and deliberate. China moves at a breakneck (finger guns) pace while the US is old and slow. This explanation is true, but shallow. The framing obscures the more interesting structural differences.

The two grids evolved and are organized in very different ways. While the US electricity system came of age as the first major electricity grid and was a distributed patchwork built over decades, the Chinese system was underdeveloped as recently as the 1990s, allowing a centralized buildout using newer technology and learning lessons from nearly a century of grid management and failures. These structural differences have massive implications for integrating renewables, maintaining reliability, and keeping pace with electrification.

For this issue, we need to move beyond “China builds fast, America builds slow” to examine the technical and institutional foundations of each grid and the choices that produced these systems.

Mechanism Design Differences: The US has far more developed market mechanisms for electricity including LMP, congestion pricing, financial transmission rights, but it has failed to update them for the renewable age, particularly around incentives for transmission investment. China’s system is state-driven with administered pricing but is rapidly introducing spot markets, capacity pricing, and ancillary services reforms.

Grid Design and Institutional Landscape: China’s grid is centrally planned, built mostly in the 2000s and 2010s with modern HVDC technology, and optimized for moving bulk power from resource-rich western provinces to coastal load centers. The US grid is a patchwork of institutional actors with differing and often conflicting incentives, built over a century for an era of local generation and long-distance fuel transport. FERC has limited authority, ERCOT deliberately avoids federal jurisdiction, and no single entity can direct interregional buildout.

The US-China Tech Gap and Power Electronics: China has invested far more aggressively in UHVDC and long-distance interconnection, building a domestic manufacturing ecosystem for converter valves, thyristors, and complete HVDC systems in the process. The US spends over 90 percent of transmission funding on short, low-voltage reliability projects and lacks the centralized procurement authority to drive a comparable program. The resulting supply chain dependence compounds the infrastructure gap.

The Broken Interconnection Queue: Interconnection queues are broken on both the supply and demand sides. Generators take years to come online. Only 13 percent of projects requesting interconnection from 2000 to 2019 reached commercial operation by end of 2024. On the load side, there is no standardized process for large consumers. Data centers can be blocked for years or come online so fast they overwhelm the grid.

Do We Need Transmission if We Have Batteries?: Batteries solve temporal mismatch. They shift energy across hours within a day. Transmission solves spatial mismatch. It moves power across hundreds or thousands of miles. The two are complements, not substitutes. Every serious grid modeling exercise confirms that significant transmission expansion reduces the total storage needed to meet reliability and decarbonization targets.

Benefits of the American Grid Structure: The decentralized market structure is not without advantages. It rewards cost-competitive technologies. Texas became a renewable powerhouse through market economics, not mandates. The structure also contains failures regionally rather than propagating them nationally, enables policy experimentation, and insulates energy planning from the whims of any single administration. The goal of fixing American grid buildout is not to replicate China’s institutional architecture but to reform the US system to leverage these strengths at greater scale.

Is the Gap Insurmountable?: That depends on the binding constraint. Permitting reform shows rare bipartisan momentum. Capital is increasingly available, though poorly allocated toward interregional projects. The technology gap is real but solvable with concentrated effort. The most likely binding constraint is institutional architecture. Institutional barriers, though human-made and therefore changeable, may prove harder to overcome than technical ones in the current political environment.

Implications for AI Development: Energy enters AI’s production function primarily as a physical constraint on data center siting, not a cost concern. Data center power demand could reach 12 percent of US electricity by 2028. Inference workloads need proximity to population centers; training workloads need massive sustained power. Transmission directly addresses this by decoupling where energy is produced from where it is consumed — the same logic behind China’s UHV corridors.

Policy Recommendations: There is rare bipartisan consensus that the grid needs more interregional transmission. Every serious modeling exercise reaches the same conclusion. Legislation like the Big Wires Act provides a blueprint. Recent reforms like FERC Order 1920 and the CITAP permitting program represent meaningful steps. However, the institutional architecture for large-scale buildout does not yet exist, and building it may be the hardest infrastructure challenge of the next decade.

Background on Electricity Market and Transmission

Understanding why transmission matters requires understanding how absurdly fragmented the American electricity system actually is and how that fragmentation came to be.

Electric utilities in the United States started as power plants with local district service networks. In New England, some are still called “municipal light plants,” an archaic term that captures the original scale: one plant, one town. These local utilities expanded into state-regulated monopolies, each with its own service territory, its own rates, and its own rules. For decades, that was the entire regulatory structure: States oversaw their utilities, and the federal government had a limited to non-existent role.

Federal involvement came in layers, each one incomplete. The Federal Power Act of 1920 gave the federal government authority over interstate electricity sales and hydroelectric licensing. States were still states firmly in control of generation, distribution, and retail rates. The Public Utility Regulatory Policies Act of 1978 (PURPA) cracked open the generation monopoly by requiring utilities to purchase power from qualifying independent producers. PURPA represented the first real wedge into the vertically integrated model.

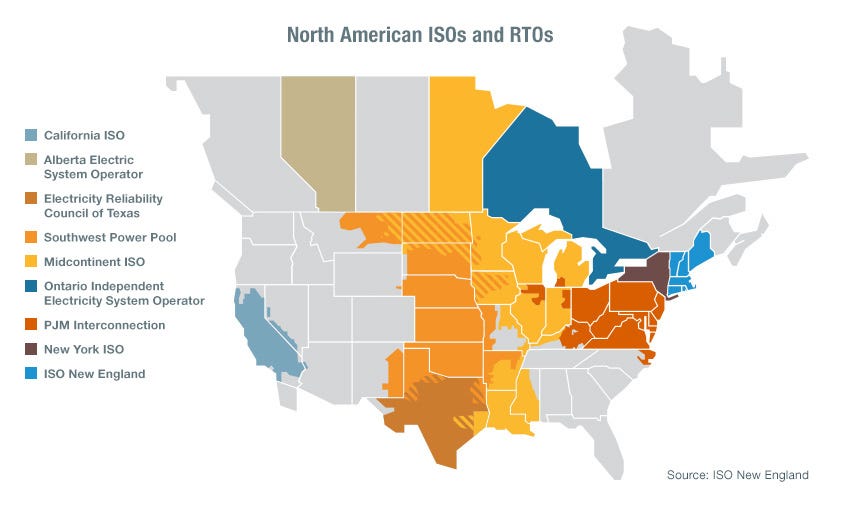

The floodgates finally opened with 90s style deregulation and the creation of FERC Order 888 in 1996. The order mandated open access to transmission networks, which is the only reason Independent System Operators and Regional Transmission Organizations exist at all. The first Independent System Operator was the Electric Reliability Council of Texas (ERCOT).

The result is a regulatory patchwork that defies easy summary. Roughly two-thirds of US electricity consumption is served through organized wholesale markets run by seven ISOs and RTOs, each with slightly different rules in tiny but frustratingly important ways. The rest of the country, including much of the Southeast and Northwest, still operates under vertically integrated utilities with state-level regulation.

Critically, FERC’s authority has hard limits. ERCOT, which covers most but not all of Texas, deliberately avoids engaging in interstate commerce specifically to stay outside FERC’s jurisdiction. CAISO operates under heavy California state oversight. Even within ISO territories, state governments retain enormous sway over siting, permitting, and resource planning. The federal government’s ability to direct grid investment is far weaker than most people assume.

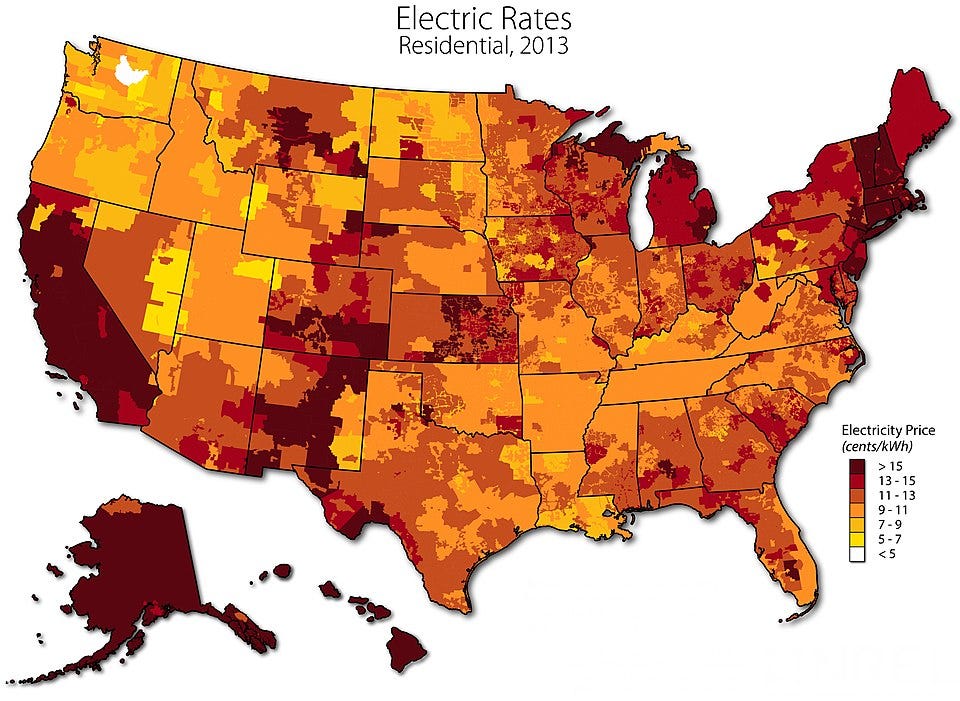

What you need to know about how electricity is actually priced: in organized markets, electric spot prices change every five to fifteen minutes and vary by physical location on the grid. Which substation you are looking at matters a great deal.

The price of electricity is technically both time-dependent and location-dependent, and the rules governing how those prices are set differ across every market in ways that matter enormously to participants and are nearly invisible to everyone else. Think of it as a spot price with extreme granularity. The mechanisms governing the market are a fusion of neoclassical economics and electrical engineering and are about as obtuse as expected. The rules are complicated enough to fill several textbooks and contentious enough to fill several courtrooms.

What makes transmission the central challenge is the mismatch in timescales across every layer of the system:

Energy imbalances must be corrected at the sub-second level.

Spot prices move every 5–15 minutes.

Power plants ramp on the scale of 10–120 minutes.

Dispatch decisions typically operate in 3–8 hour blocks.

Transmission upgrades are planned in 5-year increments.

New generation and transmission requiring new rights-of-way take 10 years — 15 if you draw the wrong opposition.

The price signals that should drive efficient investment do exist. When transmission between two regions is constrained, prices diverge: cheap wind power in western Kansas might trade at rock-bottom prices locally while consumers a few states east pay multiples of that because there is physically not enough wire to move the power. That price gap is, in a literal sense, the economic cost of inadequate transmission.

The problem comes from the institutional machinery. The institutional process to act on those signals operates on a fundamentally different timescale than the signals themselves. Building a power plant takes three to five years; building an interregional transmission line takes ten to fifteen, if it gets built at all. The feedback loop between price signals and infrastructure investment is not just slow… it is broken.

How China’s Mechanism Design Differs from US Design

Let’s start with the economist’s best friend: mechanism design.

The US and China have designed fundamentally different mechanisms for allocating electricity, and those differences ripple through every aspect of grid investment and operation.

The US system, where organized markets exist, relies mostly on LMP to coordinate dispatch and signal investment needs. Generators bid into day-ahead and real-time markets. Transmission constraints are priced into locational differences. Financial instruments like congestion revenue rights and financial transmission rights allow market participants to hedge against and trade on congestion patterns. The theory is elegant: let prices reveal where the system is constrained, and let investment flow toward those constraints.

China’s system is built on a different logic entirely. For decades, electricity was allocated through government-set benchmark prices and administrative dispatch. Generators received a guaranteed number of operating hours at regulated tariffs, and the grid companies (SGCC and China Southern) handled transmission and distribution under regulated cost-of-service models. There was no real-time price formation, no congestion pricing, and no market signal telling investors where transmission was needed. The central plan told them.

This is changing, though not as fast as headlines suggest. China launched electricity spot market pilots beginning in 2017, and by the end of 2024, 29 provincial grids were operating or trialing spot markets. In April 2025, the NDRC and NEA issued a notice calling for nationwide spot market coverage by the end of 2025. China is also introducing capacity pricing for coal plants and has overhauled its ancillary services markets. Ancillary services markets are the contracts that keep the grid stable and the lights on during emergencies.

In December 2021, the National Energy Administration issued its first major update to these market rules since 2006, formally expanding the range of services that generators can be paid for, including ramping up and down quickly to absorb solar and wind swings, maintaining stable frequency when renewable output is unpredictable, and keeping voltage steady across transmission lines. Coal plants remain the primary providers of these services today, but the reforms open the door to battery storage and demand-response resources competing for the same contracts. Perhaps most consequentially, China is moving towards pushing renewable generators to stand on their own and at least in theory, pushing most renewable generators from guaranteed fixed-price contracts into market-based pricing under the February 2025 “Document 136” reforms.

But China’s market reforms operate within a fundamentally different institutional framework than that which governs the US system. Provincial governments retain enormous influence over local power markets, often prioritizing local generators and resisting interprovincial trade. The NDRC and NEA set the broad parameters, but implementation is provincial. Analysts have noted that provincial officials have responded to recent power shortages not by increasing interprovincial trading but by investing in within-province generation. This is the opposite of what an efficient national market would dictate.

Here is the core irony: the US has sophisticated market mechanisms that should, in theory, optimally allocate generation and transmission investment, but the institutional fragmentation and lack of incentive for cooperation amongst the necessary parties combine to prevent those signals from translating into coordinated action. Further, the US pricing system and capacity markets are designed for large fossil resources with fuel costs, and then they distort in messy ways for projects with high capex, low marginal costs, and distributed construction, like renewables. A similar problem exists for incentives for transmission buildout.

China has a centralized planning apparatus that can direct massive infrastructure buildout, but it lacks the granular price signals that would optimize the use of that infrastructure. China is building the hardware; the US has the software. Neither has both, but China is making strides towards upgrading to a better operating system while the US is fine running modern Office 365 on a Commodore-64.

The 15th Five-Year Plan period (2026–2030) may be the most consequential test of whether China can integrate market mechanisms into its centrally planned grid without losing the coordination advantages that made the buildout possible. The US faces the opposite test: whether it can layer enough coordination onto its market system to achieve the scale of buildout that the energy transition demands.

Consider the significant institutional mismatch. FERC, the only federal body with authority over the interstate electricity grid, has approximately 1,500 employees. Its legal authority under the Federal Power Act extends only to wholesale electricity transactions that cross state lines. FERC cannot site power plants, cannot compel states to approve transmission routes, and does not have the authority to regulate transmission line construction, as that authority rests with the individual state. If a state simply refuses to permit a line, FERC has almost no recourse.

Then there is the grid’s lovable scamp ERCOT: FERC’s authority over the Texas grid is circumscribed because ERCOT is not synchronously operated with either of the interstate electric grids. Because ERCOT runs wholesale markets exclusively for trade within the state, it is not subject to the same federal oversight as other RTOs. The entity responsible for coordinating the American grid buildout cannot tell Texas what to do. That is the total polar opposite of how China plans and builds transmission. This may be the single most important institutional fact for understanding why the US cannot simply replicate China’s buildout pace even if policymakers could somehow agree to.

Two Grids, Two Design Philosophies

The physical differences between the two grids are as striking as any of the market design differences.

The US grid is roughly 700,000 circuit miles of transmission lines, of which around 200,000–240,000 miles are high-voltage. It’s organized into three loosely connected interconnections: the Eastern Interconnection, the Western Interconnection, and ERCOT (Texas). The interconnections are themselves composites of systems built outward from load centers by vertically integrated utilities over the past century.

Most of the US is in deregulated wholesale markets with Independent System Operators and a split between monopolistic transmission and competitive generation markets, but some areas like the Southeast and Northwest have vertically integrated utilities. To add to complexity, even in vertically integrated markets, distribution is sometimes separated from generation as in the case of electricity cooperatives. Each grid network is regulated differently, and each state within an RTO is regulated differently.

It is important to note that ISO and even interconnection boundaries are not always drawn in obvious ways. Some states in RTO territories have vertically integrated utilities like Vermont and Virginia. The big difference is whether the transmission and distribution utility is also allowed to own power plants. Dominion (VA) can. AEP Ohio (OH) cannot. Houston is in MISO, not ERCOT. Chicago and its suburbs are in PJM, but the rest of Illinois is in MISO. The transmission lines that connect MISO South to MISO Central technically go over SPP territory. Part of Manitoba is in MISO, so it’s technically an international organization. The grid organization is in some sense strewn together like different ingredients in a slop bowl at Sweetgreen.

The equivalent example for the Chinese context would be if Hebei and Shandong had their own planning authorities and regulatory bodies that had slightly different rules for what counted as a “peak response power plant”, which meant there was a complicated exchange mechanism to sell power across provincial boundaries; meanwhile Yunnan only had 5 GW of transmission capacity to literally any other part of the planet because Yunnan gotta Yunnan. The rest of the country might as well be Inner Mongolia. If this were China’s situation, and we had a centralized grid, we would certainly be patting ourselves on the back with hints of schadenfreude, as I am sure Chinese grid operators occasionally do as they keep the grid running around the clock.

Remember that the United States grid was built in phases by different actors in different regions over decades from the late 1880s to the 1940s. Much of the South did not have any electricity until the investments made by the Rural Electrification Administration as part of the New Deal. As much as Southern politicians would like to forget, the rise of the New South was- and continues to be- only enabled by the infusion of federal investments. TVA and Bonneville Power are still federally owned. The vast majority of Inflation Reduction subsidy money for clean energy, and much of the CHIPS act funding for similar investments went to Republican states.

As electric power in the early days of electrification was highly tied to political and economic power, companies providing the power benefited from creating monopolistic fiefdoms. The utilities had little incentive to interconnect beyond what reliability required. The current structure of the grid even ensures that different utilities can have different incentives, with some utilities with power plants even benefiting financially from higher wholesale prices even as other utilities have their lunches eaten. Even after much of the market structure has been improved, the continuing result is a web of seams: jurisdictional boundaries that create physical and economic bottlenecks wherever one utility’s territory ends and another’s begins.

China’s backbone grid, by contrast, was substantially built in the 2000s and 2010s under national planning with modern power electronics and HVDC technology from the start. This isn’t just a matter of age. It reflects a fundamentally different design philosophy: an increasingly hierarchical hub-and-spoke system optimized for one overriding purpose. The Chinese grid is designed for moving bulk power from resource-rich western provinces to the coastal megacities where it’s consumed.

The geography demanded it. Three-quarters of China’s coal has historically been in the northwest, most hydropower is in the southwest, and the best wind and solar resources sit in the Gobi and the western plateaus. The population and industry are on the eastern seaboard. Having historical case studies on the value of interregional transmission allowed China to learn from past mistakes.

Building in a time where there was knowledge and a keen insight that the next generation of electric resources would be spatially dispersed and renewable allowed China to design a grid with an eye towards the future. By contrast electric utilities in the US started as urban light plants. Rural electrification did not happen in the United States until 70 years afterward.

The result in the PRC is a system where a single ±1,100 kV UHVDC line, the Changji-Guquan link from Xinjiang to Anhui, can transmit 12 GW over 3,293 kilometers, enough to serve roughly 50 million households. China’s State Grid Corporation calls it the “Power Silk Road” (能源丝绸之路 ) because it follows the ancient trade route through the Hexi Corridor. There is nothing remotely comparable in the United States, or anywhere else.

The US renewable resource landscape is also quite dispersed, providing the economic argument for investment in transmission. Unfortunately, when the US grid was originally developed, high fossil fuel penetration was the standard, and no one would have thought to plan for otherwise. The grid started with coal. Oil and gas came later. For the first power plants, your fuel was solid, could be transported by rail or barge, and could be stored in an open-air pit next to your power plant. The US began with essentially non-existent technology for wind and solar, which meant long-distance transport of renewable energy was neither a first- nor second-order concern.

The Institutional Landscape

The institutional differences are at least as consequential as the physical ones.

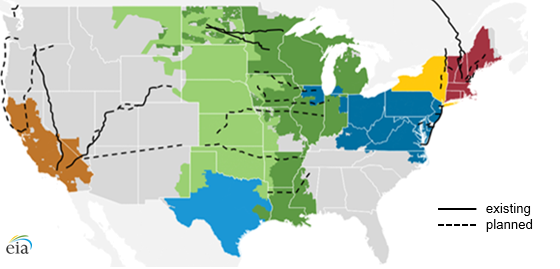

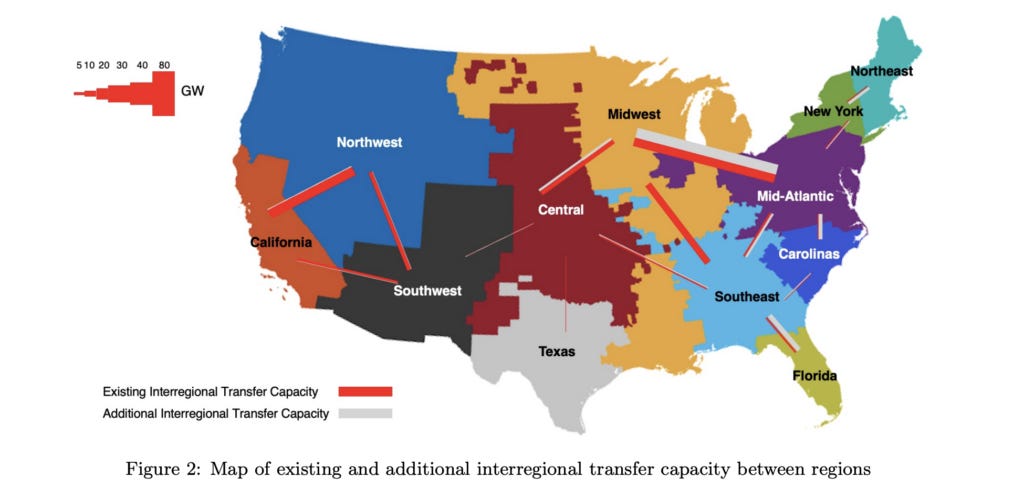

The US has FERC at the federal level, seven RTOs and ISOs covering roughly two-thirds of the country’s load, and a patchwork of vertically integrated utilities handling the rest. Transmission planning is fragmented across regions with misaligned incentives. ERCOT famously remains an island with small connections to the Southwestern Power Pool. This island mentality is at least partially driven by an effort to avoid engaging in interstate commerce as much as possible to prevent FERC regulation under the banner of federalism.

This is changing, though, as ERCOT moves to capitalize on surging data center demand and massive renewable investments by expanding its limited external connections. The proposed Southern Spirit Transmission project, a 320-mile, ±525 kV HVDC line developed by Pattern Energy, would connect ERCOT to the southeastern grid via Louisiana and Mississippi with up to 3,000 MW of bidirectional capacity, more than doubling ERCOT’s existing external transfer capability. The project received up to $360 million in DOE support and is targeting a 2029 in-service date, though it faces legislative opposition in Louisiana. ERCOT has also approved the first phase of a nearly $33 billion Strategic Transmission Expansion Plan (STEP) that includes 2,468 miles of new 765 kV lines. The current buildout is a dramatic escalation from an operator that has historically underinvested in high-voltage infrastructure.

The “seams” between RTOs are notoriously difficult to build across: the benefits of a cross-seam project distribute widely while the costs concentrate, and no single entity has the authority or motivation to push projects through. Given these challenges, it is a minor miracle that any interregional transmission is built at all.

The Grain Belt Express illustrates the point. The project was initiated in 2010 by Clean Line Energy Partners as an HVDC line to move wind energy from western Kansas to load centers in the Midwest and East. Missouri’s Public Service Commission rejected the project outright around 2015, saying it was not needed by Missouri ratepayers, and then rejected the developer’s second application on procedural grounds. The project will span four states and involve three regional grids: SPP, MISO, and PJMs. As Clean Line’s CEO noted at the time, there was no transmission planning process that involved even two RTOs, much less three. Quite a challenge.

Fierce opposition came from rural landowners and farmers across eight Missouri counties who feared drops in property values and forced easement sales through eminent domain. Clean Line sold the project to Invenergy in 2018. Invenergy secured Missouri PSC approval in 2019, but legal challenges, an Illinois appeals court reversal of state regulators’ approval, and ongoing eminent domain battles followed.

Missouri Senator Josh Hawley blasted the project as an “unconstitutional land grab,” and Republican legislators in the state tried for years to strip Invenergy of its eminent domain authority. The DOE terminated its conditional loan guarantee commitment for the project in July 2025. So much for energy dominance! Nevertheless, the project pushes on. Construction on Phase 1 is now targeting 2026, with an operational date of 2029. It is important to note that this is nearly two decades after the project was conceived. Even a line that would connect four grid regions and add 5,000 MW of delivery capacity cannot escape the gauntlet of state-by-state siting approvals, landowner opposition, and political headwinds.

The Plains & Eastern Clean Line met an even worse fate. The proposed 720-mile, 4,000 MW HVDC line would have carried wind power from the Oklahoma Panhandle to the Tennessee Valley Authority grid near Memphis, bringing renewable energy to a part of the Southeast that had little access to it and creating risk sharing between conventional baseload clean power from the TVA and new renewables from SPP. The project faced intense opposition, particularly from landowners in Arkansas. After the Arkansas Public Service Commission denied Clean Line utility status, the developer turned to the federal government, and in March 2016, the DOE signed a participation agreement under Section 1222 of the Energy Policy Act of 2005. This was the DOE’s its first exercise of that authority.

The use of federal power to advance a line over state objections only intensified the backlash; Arkansas’s congressional delegation hailed the project’s eventual collapse as a “victory for states’ rights.” TVA’s refusal to sign a power purchase agreement effectively killed the project’s financial viability, and by March 2018, the DOE and Clean Line mutually agreed to terminate their participation agreement. NextEra Energy Resources acquired the Oklahoma assets, but the line as originally envisioned was dead, a victim of state-level resistance, incumbent utility obstruction combined with the absence of any institutional mechanism to force coordination across regional boundaries. At least the Grain Belt Express is getting built! Clean Line’s CEO was right that the United States is simply not good at building interstate transmission, but the Plains & Eastern experience suggests the problem is structural, not incidental.

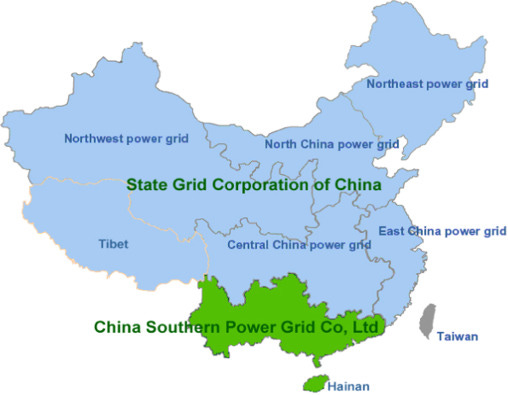

China has two state-owned grid companies: State Grid Corporation of China (SGCC), covering about 80 percent of the country’s territory, and China Southern Power Grid, handling the rest. SGCC is the world’s largest utility by almost any measure. The company has roughly $546 billion in revenue in 2023, around 1.1 billion customers, and somewhere north of 870,000 employees. It ranks among the top five companies globally by revenue with yearly receivables above most nation-states’ GDPs. SGCC operates under central planning directives from the National Development and Reform Commission (NDRC) and the National Energy Administration (NEA), with the authority to site and build essentially at will.

What does this mean concretely? Three comparisons illustrate the gap.

Interconnection queues. In the United States, as of the end of 2024, roughly 10,300 projects representing about 1,400 GW of generation and 890 GW of storage were actively seeking grid interconnection, according to Lawrence Berkeley National Laboratory’s “Queued Up” report. The median time from interconnection request to commercial operation has more than doubled. The time to connection has increased from under two years for projects built in 2000-2007 to over four years for those built in 2018-2024.

Most proposed capacity never even gets built as investment timelines struggle with the uncertainty. Only 13 percent of capacity that submitted interconnection requests from 2000 to 2019 had reached commercial operations by the end of 2024 while 77 percent had been withdrawn. The US interconnection queue contains more than twice the country’s entire installed generation capacity, yet it functions less as a pipeline than as a graveyard. For this reason, people should not use interconnection queues as guidance for what projects are coming onto the grid.

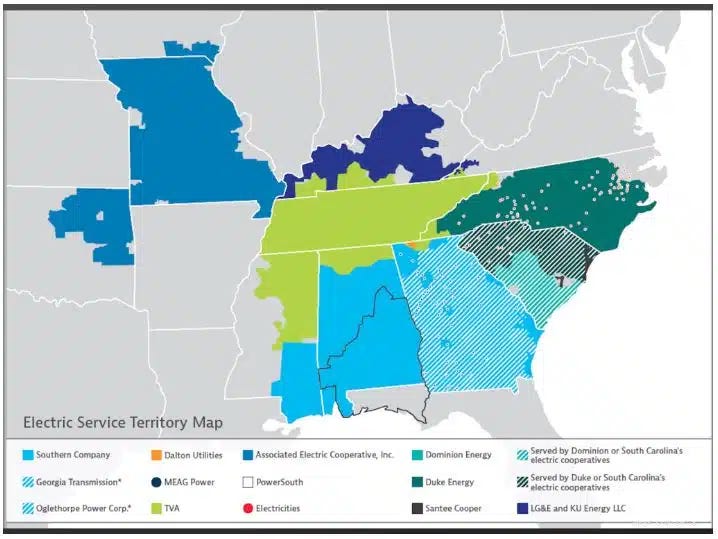

Part of the problem stems from how the US institutional framework separates generation and transmission planning. Within RTO territories, generation and transmission are planned by different entities. Generators and transmission owners operate under distinct ownership structures, with coordination happening primarily through reliability and transmission planning committees. The closest analog to truly unified generation-transmission planning in the US exists in fully vertically integrated utility territories, such as those served by Southern Company.

In stark contrast, China’s system doesn’t have an interconnection queue problem in the same sense, because generation and transmission are planned jointly by the state. When the NDRC approves a large renewable energy base in the Gobi Desert, it simultaneously approves the UHVDC line to evacuate the power. The December 2025 groundbreaking on an 800-kV, 700-km UHVDC line from Inner Mongolia to Beijing-Tianjin-Hebei, budgeted at 17.2 billion yuan (~$2.5 billion), expected operational by 2027, illustrates the typical timeline. Approval to energization in roughly two years is the norm for Chinese UHV projects, not the exception. Large load, which is also a victim of a poor interconnection process, has a similar disparity.

Planning horizons. FERC Order 1920, issued in May 2024, now requires US transmission providers to conduct long-term regional planning over a 20-year horizon. This is a significant expansion from the prior three- to five-year window. This was hailed as a landmark reform. China’s State Grid has been planning on multi-decade horizons since its inception, embedded in the Five-Year Plan structure with rolling revisions. Between 2026 and 2030, SGCC plans to invest approximately ¥4 trillion (~$574 billion) in grid expansion and upgrades. This is roughly a 40 percent increase over the previous five-year period.

Jurisdictional boundaries. When a transmission project crosses jurisdictional boundaries in the United States — say, a line from Iowa to Illinois that bridges MISO and PJM — developers face separate regulatory proceedings, different cost allocation frameworks, potentially hostile state siting authorities, and the seams issue that makes interregional planning the third rail of grid politics. FERC Order 1920 attempts to address this, but the order faces legal challenges and will, at best, take years to implement.

When a Chinese UHV project crosses provincial boundaries as nearly all of them do (the Baihetan-Jiangsu line crosses Sichuan, Chongqing, Hubei, Anhui, and Jiangsu), the central government directs and SGCC executes. Provincial governments may negotiate over compensation and local employment, but they are unable to exercise veto power over siting.

The Technology Gap: AC vs. DC

The core technological divergence is China’s commitment to new generation power electronics and ultra-high voltage DC.

The United States remains predominantly an AC system. The highest-voltage AC lines in common use are 765 kV, and the country has only a handful of HVDC transmission facilities. For a good while, only AEP was doing 765kV, everyone else capped out at 500kV. There are approximately 20 HVDC facilities, though the exact number depends on definitions. The most prominent is the Pacific DC Intertie, a ±500 kV line that has been operating for over 50 years. There are no UHV DC lines in the US, and total operational HVDC capacity is on the order of a few gigawatts.

China, by contrast, has built the world’s only operational ±1,100 kV UHVDC line (Changji-Guquan), at least 23 ±800 kV UHVDC lines, and pioneered the world’s first multi-terminal VSC-HVDC grid at Zhangbei. The grid is a ring network connecting wind, solar, and hydro that delivers up to 4,500 MW to the Beijing-Tianjin-Hebei area. In July 2024, China broke ground on the world’s first ultra-high voltage flexible direct current project: a ±800 kV VSC-HVDC line from Wuwei, Gansu to Shaoxing, Zhejiang, stretching 2,370 km across six provinces with a rated capacity of 8 GW and a budget of about 35.3 billion yuan (~$4.8 billion).

Why did the two countries diverge so sharply?

Part of it is geography. China’s resource-to-load distances are genuinely extreme at several thousand kilometers in some extreme cases. This made the economic evidence for HVDC overwhelming even before costs came down significantly. AC losses become prohibitive at those distances. A ±1,100 kV DC line can transmit power four to five times further than a 500 kV AC line, with losses reduced to roughly a quarter of what equivalent AC infrastructure would incur.

However, geography alone doesn’t explain it. The United States has its own vast distances. Wind resources in the Great Plains could supply East Coast load centers. Solar in the Desert Southwest could reach the Pacific Northwest with Pacific hydro providing insurance against Southwestern price spikes. The distances are comparable to many Chinese UHV corridors. The difference is institutional.

China, through SGCC and the NDRC, was able to make a centralized bet on UHVDC as a national technology platform. State Grid put some 2,000 engineers on the UHV program, funded more than 300 professors and 1,000 graduate students at Chinese universities for power-grid R&D, and ensured that domestic suppliers would manufacture 90 percent of UHV equipment. By 2006, 70 percent of equipment for the Three Gorges-Shanghai HVDC project was manufactured domestically. Since then, all ±500 kV and ±800 kV DC projects have used Chinese-made equipment.

The US, with its fragmented planning authority, couldn’t have made this bet even if it wanted to. No single entity has the combination of planning authority, rate recovery mechanisms, and procurement power to drive a national HVDC program. FERC can set rules for transmission planning but cannot direct construction. RTOs can identify needs but don’t build. Utilities build, but their incentive structures favor local, reliability-driven spending on lower-voltage infrastructure. Even when the stars and incentives align for reliability spending, often utilities are not even allowed to build their own generators and have no incentive to prioritize infrastructure for someone else’s investments and profits.

The lower investments in high-voltage infrastructure is exactly what the data show. Grid Strategies found that more than 90 percent of US utility transmission spending goes to lower-voltage, reliability-driven projects, often built outside of regional planning processes entirely. Zonal-separated capacity markets were intended to drive massive increases in interregional transmission but so far seem to have failed to achieve this purpose.

The Interconnection Queue

Returning to the interconnection queue, the generation-side dysfunction described above is only half the story. The load interconnection side alluded to, the process by which large electricity consumers connect to the grid, is where the wheels are coming off most visibly, and where the AI-driven demand surge is creating unprecedented challenges.

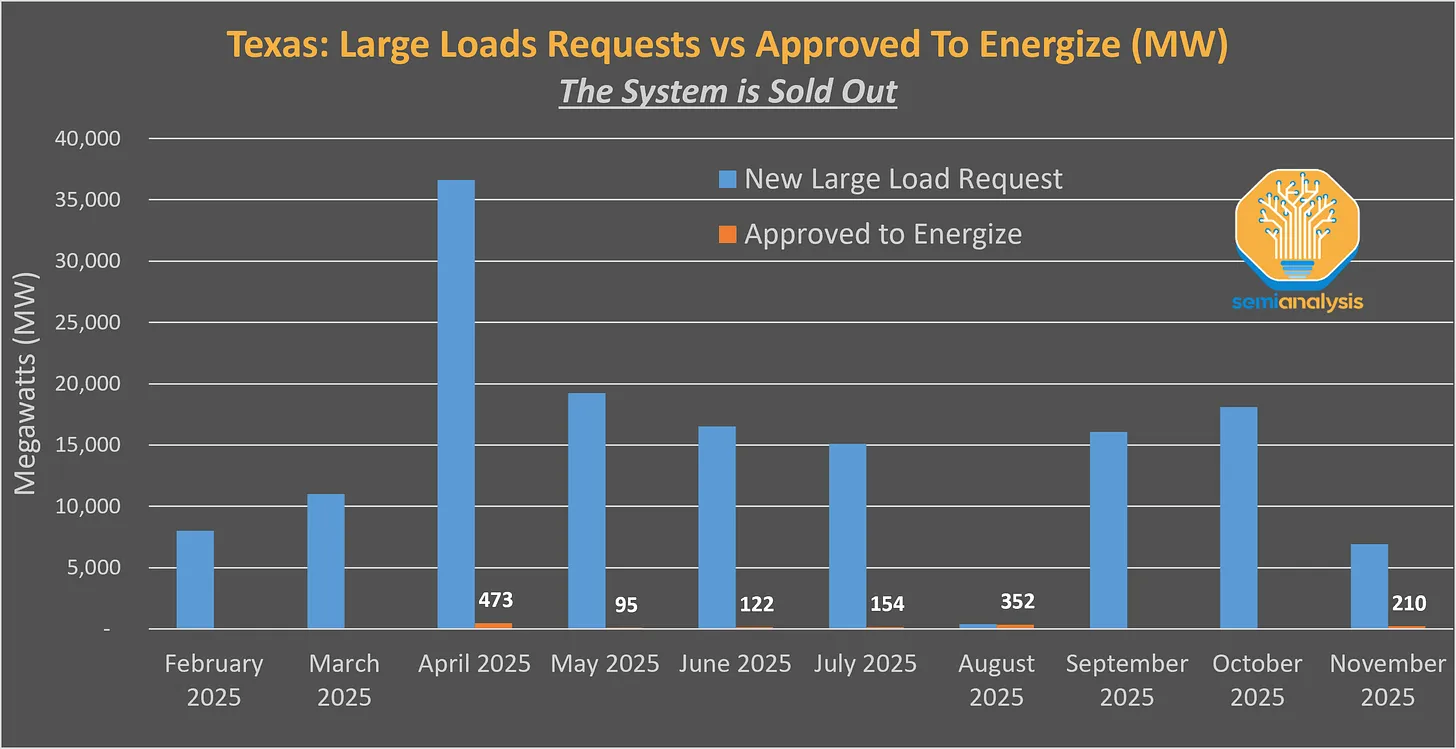

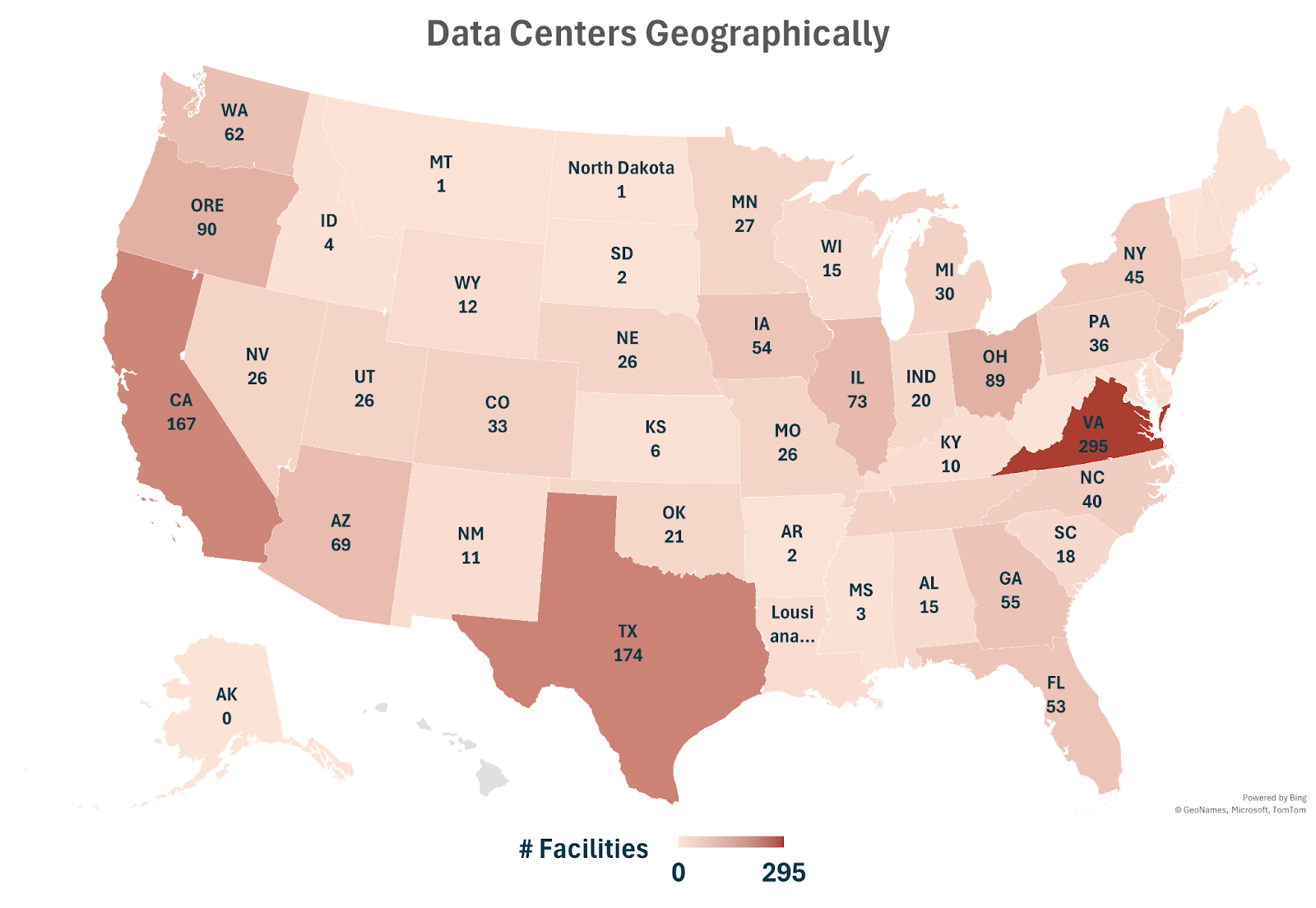

ERCOT provides the starkest illustration. By November 2025, ERCOT was tracking over 225 GW of large load interconnection requests — up nearly 300 percent from roughly 63 GW at the end of 2024. Data centers account for approximately 73 percent of these requests, with some individual projects seeking over 1 GW of capacity at a single site. To put this in perspective, ERCOT’s all-time peak demand record is 85.5 GW. The queue contains roughly two and a half times the entire system’s historical peak load.

The problem is not just volume but also uncertainty. ERCOT’s interconnection process was designed to handle 40 to 50 large load requests at a time. With 225 new requests in a single year, many speculative and many from hyperscalers filing in multiple locations to hedge their options, the system cannot distinguish real projects from placeholders. Projects come online so fast that sometimes grid operators run their interconnection studies, the studies go out of date before it’s even done, meaning they need to re-run the studies. ERCOT cannot plan as it does not know what will get built. Texas passed SB 6 in 2025 to address this, requiring new transparency standards for large-load customers and directing the PUC to standardize interconnection rules. But rulemaking takes time, and the demand is in the process of materializing now.

Other regions face similar challenges at different scales. PJM has seen an explosion of data center interconnection requests in northern Virginia, where the world’s largest concentration of data centers already sits. In late 2025, the DOE took the extraordinary step of directing FERC to initiate rulemaking to bring large load interconnection under federal jurisdiction, representing a dramatic expansion that reflects how broken the current patchwork of state-level processes has become. This was after PJM spent three months in the CIFP-LLA proceeding trying to fix this problem internally, except their work completely collapsed because of infighting. FERC had to step in after this process failed.

China’s approach again offers a revealing contrast. Because generation, transmission, and load are planned jointly under state direction, the concept of a “load interconnection queue” in the American sense does not exist. When the central government designates an industrial zone or data center cluster, the grid infrastructure to serve it is planned and built in parallel. This does not mean China’s system is frictionless. Provincial grid companies still face construction bottlenecks and land acquisition challenges; however, the sequential, adversarial process that characterizes American interconnection is absent. Projects do not wait in line; they are planned into existence. In a race to build the infrastructure to support AI, the US appears committed to filling out forms as China sprints.

Do We Need Transmission if We Have Batteries?

There is a popular argument that the failure to build out transmission is becoming a moot point. Battery storage costs have plummeted. Ember estimated the cost of storing electricity at utility scale had fallen to roughly $65/MWh by late 2025. Battery deployment is also surging. China alone added over 42 GW of new energy storage capacity in 2024, more than doubling its installed base to nearly 74 GW. In the United States, California’s battery fleet now routinely meets close to a fifth of evening peak demand, displacing gas generation that would have been unthinkable to replace just three years ago. If storage can shift renewable generation from when it’s produced to when it’s needed, why bother with thousand-mile transmission lines?

The answer is that batteries and transmission solve different problems, and the evidence increasingly suggests they are often complements rather than substitutes. Batteries excel at temporal shifting. They move energy across hours within a single day. A four-hour battery system paired with solar can shift midday surplus into evening peak. Temporal shifting provides enormous value, but it fundamentally cannot solve the spatial mismatch that transmission addresses. The best wind resources in the Great Plains and the best solar resources in the Desert Southwest are still thousands of miles from major East Coast and Midwestern load centers with coastal offshore wind decades away from being economically competitive. No amount of local storage changes the fact that a wind turbine in Kansas has a much higher capacity factor than one in New Jersey.

Transmission addresses the geographic dimension. A well-connected grid allows regions to risk-pool by sharing diverse resources: when the wind is not blowing in Texas, it may be blowing in the Dakotas. When solar production peaks in Arizona, it can serve evening demand in California. This geographic diversification of variable resources reduces the total amount of storage needed Every serious grid modeling exercise confirms the need for a joint approach. The NREL National Transmission Planning Study found that scenarios with significant transmission expansion required substantially less storage to achieve the same reliability and decarbonization targets.

China has positioned itself well to take advantage of this complementarity. Even as it deploys storage at a pace that dwarfs the rest of the world, it continues to build UHV transmission at breakneck speed. The 15th Five-Year Plan is expected to include both a target of 180 GW of energy storage by 2027 — a planned installation target equivalent to today’s global capacity — and continued expansion of the UHV network. Chinese grid planners are not choosing between batteries and wires; they are deploying both. The physics and economics demand it.

The Supply Chain Dimension

Transformers get the headlines. Everyone has read about the multi-year backlogs for large power transformers, but the supply chain story that may matter more strategically is in the power electronics that make HVDC work: converter valves, thyristors, IGBTs, and the full systems-integration capability for converter stations.

Converter stations account for as much as 60 percent of the total fixed cost of an HVDC project, according to the EIA. This makes the converter supply chain the critical bottleneck. Converters are also heavily concentrated.

China’s UHV buildout has generated massive domestic manufacturing scale in precisely these technologies. Companies like TBEA, NR Electric, XJ Electric, and Xuji Group now supply complete UHVDC systems, from converter valves to control and protection equipment. The HVDC equipment supply chain in China functions as what industry analysts describe as a “regulated duopoly” between SGCC and China Southern Power Grid, which together accounted for an estimated 94 percent of engineering, procurement, and construction awards in 2025. Domestic suppliers reportedly commanded 68 percent of submarine HVDC cable orders in 2025, undercutting European competitors through shorter delivery cycles.

That said, the global HVDC equipment market still features significant non-Chinese players in critical niches. Hitachi Energy (formerly ABB Power Grids), Siemens Energy, and others retain expertise in advanced VSC technologies and ultra-high voltage components. Only two global vendors can currently deliver the 8.5 kV thyristors needed for ±1,100 kV valve assemblies, and certain high-performance power semiconductors still rely partly on non-Chinese production. The supply chain picture is not one of total Chinese dominance yet. However, we are seeing rapidly consolidating Chinese capabilities in systems integration and high-volume manufacturing with Western firms maintaining positions in specialized components.

For the United States, the supply chain constraint interacts with the institutional constraint in a particularly vicious way. Even if US policy resolved the permitting and planning barriers to HVDC construction overnight, the converter stations and specialized equipment would take years to procure, and much of the manufacturing capacity would likely have to be located in or dependent on China.

For more on the power electronics supply chain, see Dana’s other piece:

Are There Benefits to the American Grid Structure?

It can be hard sometimes to see the method in the madness; however, for all its challenges, the American grid structure has some real advantages over more centrally planned grids that any fair comparison must acknowledge.

The most underappreciated may be the role of market incentives in driving technology adoption. Texas, the Republican bastion, the poster child for deregulated, politically conservative energy policy, has become one of the world’s largest wind, solar, and battery energy markets, not because of state planning mandates but because wind and solar were cheaper options. The competitive market simply rewarded efficiency.

ERCOT added nearly 10 GW of new solar capacity in 2024 alone, alongside massive growth in battery storage, driven entirely by market economics. In some ways, this buildout is in spite of the best efforts of some of Texas’s lawmakers. In an alternate world with centrally planned expansion of generation infrastructure, it is far from obvious that politically conservative states would have embraced renewables at this pace. The American market structure, for all its coordination failures, has proven remarkably effective at identifying and scaling the cheapest generation technologies in markets where they are cost competitive.

Decentralization also provides resilience through diversity. The US grid’s fragmented structure means that planning mistakes, regulatory failures, or technology bets that do not pan out are contained within regions rather than propagated nationally. When ERCOT nearly collapsed due to lack of weatherization during Winter Storm Uri in 2021, the Eastern and Western Interconnections continued to function as normal. No $9,000 dollar per megawatt-hour electricity for Oklahoma.

China’s more centralized system creates different vulnerabilities: a single planning error at the national level can misallocate resources across an entire continent-sized grid. The system’s heavy reliance on long-distance UHV corridors also creates concentration risk. A failure on a single 12 GW line affects power supply for tens of millions of people. Better hope Xinjiang remains under Beijing’s heel or else, a lot of power and power manufacturing for Eastern China will get knocked offline. Of course, we are not necessarily in a position to talk. Substations are sitting ducks in an open field. The grid is a notorious target of cyber-attacks, but the physical domain is also exposed. There has recently been a scourge of attacks coordinated on Telegram by far-right domestic extremist groups against substations and power infrastructure including plots to attack energy facilities in Idaho, Maryland, and Ohio and a shooting of a Duke Energy substation with a rifle in North Carolina. Physical attacks or threats on grid infrastructure doubled between 2021 and 2023, rising to 185 according to NERC. Even with recent pushes for enhanced physical security, an IED on a consumer drone could cause major outages, and a coordinated attack on the electricity grid could cause thousands of deaths according to a 2012 report from the National Research Council.

Additionally, the US system creates labs of experimentation. Having many market structures allows us to learn quickly the conditions under which they are faced with extraordinary pressure and the conditions under which they work well. Many market innovations in the electricity space have been ported when they were seen to achieve desired results.

Additionally, decentralized markets allow for the creation of localized policies for areas that may have different needs in terms of population and resources. The abundance of hydropower and dispersed demand in the Mid and Mountain West creates very different challenges from the concentrated load and relative resource poverty in New England. Offshore wind requires different investment incentives from geothermal or solar. Also, the decentralized nature of grid ensures that no Republican administration could cancel all offshore wind farms because of concerns about the birds, and no Democratic administration could cancel nuclear to appease its radical left wing. This problem of energy planning held hostage by political concerns certainly does appear constraining for… some advanced democracies 👀👀👀.

There is also the question of political legitimacy. American infrastructure, for better or worse, is built through processes that give affected communities some voice in siting decisions. This creates delay and cost, but it also produces infrastructure that has broader public acceptance and is less vulnerable to the kind of political backlash that can accompany top-down development.

It is certainly true that a given project, no matter how important, can be derailed by 5 people complaining that TX towers ruin the view, as long as some NGO pays the legal bills. The Sierra Club has certainly exercised legal power. There is also an angle for a foreign adversary with deep pockets to potentially snarl up infrastructure projects with relatively low cost. These guardrails are unquestionably unnecessarily cumbersome in many cases. However, it is also highly valid to point out that the history of the United States is littered with examples where planners like Robert Moses moved fast and broke things and are today remembered more for things they broke than the fast movement. The balance is difficult, and when the system works well, which is admittedly rarer than it should be, it can work wonders to create sustainable to inclusive growth.

In an environment where inflation has proven a political third rail, the fact that it is not easy to raise electricity prices in the Midwest to support clean energy ambitions on the coast without corresponding transfers might be a feature not a bug. China’s ability to site transmission lines rapidly comes partly from its ability to override local objections. This approach generates resentment in affected communities and would be neither desirable nor feasible in the American context where that resentment can be raised at the ballot box.

The challenge is not to replicate China’s system but to find ways to achieve coordination and speed within the American institutional framework. FERC Order 1920, the CITAP permitting program, and the DOE’s National Interest Electric Transmission Corridor designations represent meaningful steps. It is also clear that current steps towards improved grid policy are inefficient.

In some sense, the remarkable newsworthiness of energy in the current era is already a failure. In the words of Ajey Pandey, an Energy Analyst at SemiAnalysis and former Resource Planner at an electric utility, “Infrastructure is supposed to be invisible to regular people. The fact that readers have heard the words “PJM Interconnection” is a dire failure of the institution. Most people do not know what a kilowatt-hour (kWh) is, and if the electric grid worked well, they would not need to. They could simply put their electric bill on autopay, turn on their lights, and think about the rest of their lives. The reality of electric service is too complicated to fully comprehend, even for people in the industry, and it’s frankly an indictment of the American project that we are now asking normal people to have nuanced opinions about to balance grid reliability, decarbonization, and cost allocation. The grid is supposed to simply work!”

Chief among the new admirers and critics of the grid, the administration certainly has taken note of the issue of challenges to the electricity market on Truth Social. It is wild to think that we are living in times where the PJM auction has reached the attention of the American president. While I’m sure Trump is spending his days hunched over a Bloomberg terminal analyzing capacity auction results on GridStatus.io, we will need more nuanced policies than current proposals from capacity-market-designer-in-chief Donald Trump in order to improve the market.

Is the Gap Insurmountable?

Whether China’s transmission advantages are insurmountable depends on which constraints you think are binding for the US and how much political capital leaders are willing to expend to make changes.

If the binding constraint is permitting, then there’s reason for cautious optimism. Permitting seems to be a rare issue with an emerging bipartisan consensus. FERC Order 1920’s long-term planning mandate, the CITAP program aimed at cutting federal permitting to two years, DOE’s designation of National Interest Electric Transmission Corridors, and Congressional permitting reform efforts collectively represent the most serious attempt at structural reform in decades. But “seriously trying” and “good enough” are different things. The order faces legal challenges, implementation will take years, and federal permitting reform doesn’t solve state-level siting barriers. We still have a complex patchwork of citing, not to mention an uncertain policy environment that creates inconsistency. Policy inconsistency is often what finally kills long-term infrastructure projects.

If the binding constraint is capital, the picture is a bit blurry. US utility spending on transmission has increased to over $25 billion annually, with the Edison Electric Institute projecting about $30 billion per year going forward. The money is there in the aggregate. That’s better than in the past, and tech money seems to be fueling capital investments by utilities.

But that doesn’t solve the problem of allocation: most capital is currently going to local reliability projects rather than the long-distance, high-voltage, interregional transmission that would transform the grid’s topology. This is rational behavior under current incentive structures. Utilities earn regulated returns on their own investments in their own service territories. As a potential workaround, AI developers are starting to think about investing in grid infrastructure.

More competition is on the whole not great for most utilities, particularly given that trade almost necessarily lowers average prices in importing regions. However, locally optimal behavior produces the wrong outcome for the system as a whole. Greater coordination at the federal level and through NERC are needed to ensure the system moves together. Recent developments like the current extension of the Southwestern Power Pool to the Western Interconnection show real progress towards a more unified planning architecture.

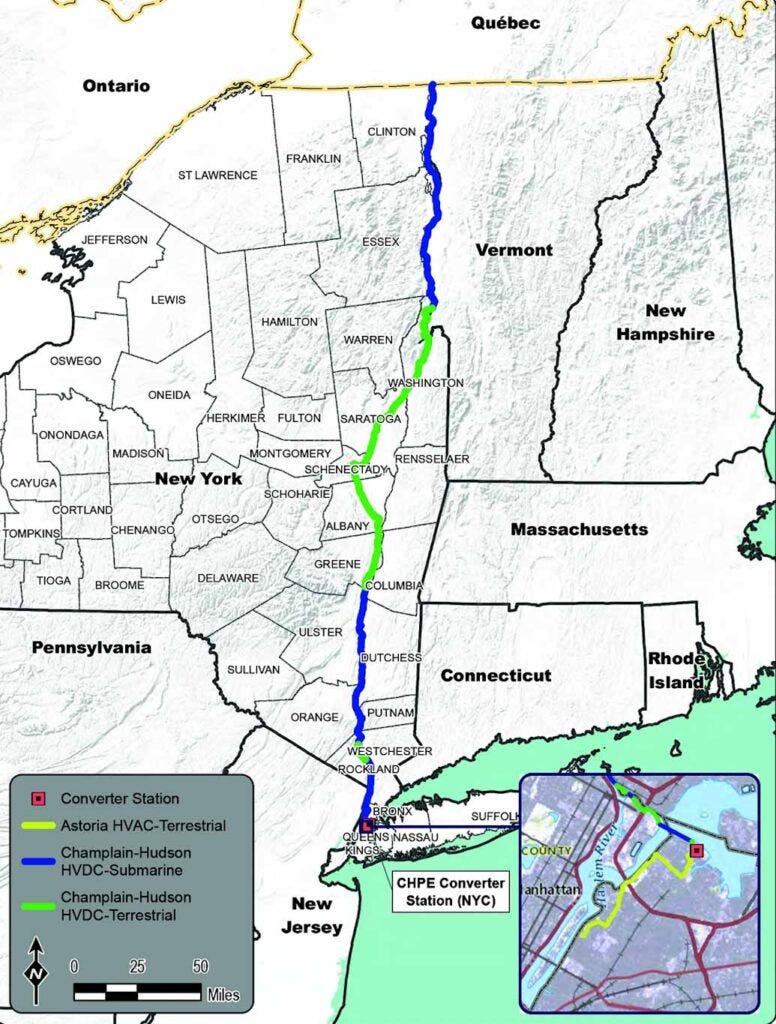

If the binding constraint is technology, there are some reasons to be worried. The US faces a genuine gap in HVDC deployment experience and domestic manufacturing capacity. A handful of new HVDC projects are moving forward — SunZia (a 550-mile, 525 kV HVDC line in the Southwest), SOO Green (a buried HVDC line along a railroad right-of-way from Iowa to Illinois), the Champlain Hudson Power Express (connecting Quebec hydropower to New York City), and several Grid United projects. Encouraging, but a fraction of what would be needed to approach anything like a national HVDC overlay.

If the binding constraint is institutional architecture — and this seems most likely — the path forward is less well-defined. Most engineers I talk to see this as a political rather than a technical problem. Unfortunately, it may be easier to solve hard technical problems than political ones in the US. Solving these problems is both everyone’s job and no one’s job, so no one person has the mandate to make changes — and if they did, they would not have the authority to implement them. The question becomes whether the US can achieve through federated, market-based processes what China achieves through organized centralized planning.

The National Transmission Planning Study from NREL and DOE estimates that the American transmission system needs to grow between 2.4 and 3.5 times its 2020 size by 2050 to meet decarbonization goals. That is a transformation on a scale the US has never attempted in this sector. Current expansion plans suggest that it may not be smart to hold our breath.

One important observation about constraints: physical and institutional constraints have remarkably different malleability, and we systematically misjudge which is which. There is a prevailing instinct, especially in technology-adjacent discourse, to treat physical constraints as engineering problems that innovation will eventually solve, while treating institutional constraints as immovable features of political reality. In practice, the reverse is often closer to the truth.

The laws of physics governing power losses over distance, the material properties of conductors, and the thermodynamics of grid stability are all set hard boundaries that no amount of political will can override. Institutional constraints like permitting timelines, cost allocation frameworks, jurisdictional boundaries are human constructions that can be reformed with sufficient political commitment.

Someone made them up, and that someone can choose to change them with enough will. The energy transition will ultimately be bounded by physics. Whether we bump up against those physical limits or get stuck well short of them because of institutional paralysis is a political choice. However, fixing this problem begins with acknowledging that Maxwell’s Laws are unchangeable and created by the universe while legal codes are created by men and therefore can be reshaped by men.

What are the Implications for AI Development?

You probably are not reading this piece simply because you love thinking about locational marginal prices and financial transmission rights. Energy is at the forefront of policy minds because of AI; you came here for an AI story and forced yourself to sit through a grid story. If that’s you, kudos for making it to your reward as the energy story now becomes an AI story.

Energy enters the production function for AI companies not primarily through the pricing channel but as a physical constraint on data center buildout. For all the handwringing, energy is actually estimated at about 2-6% of total cost of LLM training. A hyperscaler does not choose a data center location in the same way a household chooses an electricity plan. The binding question is not “what will electricity cost?” but “can I get 500 MW of firm power to this site within 18 months?” Electricity price matters at the margin, but availability is the hard constraint. Mark Zuckerberg carries around 100 million in his coat pocket in case he runs into an OpenAI researcher at Starbucks. He’s not batting an eye at Constellation’s bill for service.

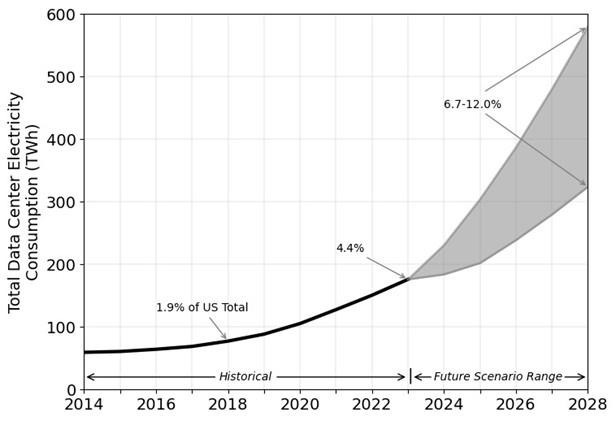

The numbers are staggering. US data center electricity consumption is estimated to have reached roughly 176 TWh in for 4.4% of total electricity demand in 2023 and is projected to reach 325 to 580 TWh for up to 12% of electricity demand by 2028 according to the DOE, depending on the pace of AI scaling. In ERCOT alone, data centers account for approximately 73 percent of the 225 GW of large load interconnection requests tracked by the end of 2025. McKinsey projects US data center power demand capacity could grow from 25 GW in 2024 to over 80 GW by 2030.

Data center demand is spatially concentrated in ways that interact directly with transmission constraints. Northern Virginia hosts the world’s largest data center cluster, sitting within PJM, a region already grappling with generation retirements, interconnection backlogs, and a strained capacity market. Texas is attracting enormous data center interest because of available land, cheap power, and a permissive regulatory environment, but ERCOT’s transmission infrastructure was not designed for gigawatt-scale point loads and the current rapid growth explosion. Other emerging strong growth areas include Georgia, Indiana, and Pennsylvania.

There is a latency-power tradeoff that limits how much data center load can simply relocate to where power is abundant. AI inference workloads — the kind that power ChatGPT, Claude, and similar services — are in some sense latency-sensitive. Every millisecond of network delay degrades user experience, which can be particularly pronounced for many users, especially with a desire to become competitive with a Google search. This means data centers serving real-time inference need to be within a few hundred miles of major population centers, not in remote areas where wind is plentiful, and people are outnumbered by cows.

Training workloads are almost entirely removed from latency-sensitivity on the demand side and can be located more flexibly, but training clusters require massive, sustained power draws that strain local grids and create challenges for reliability and power quality. Training workloads also are often distributed and require highly parallelized workflows. Thus, these workloads benefit from concentration. One option to deal with this tradeoff is to move inference workloads on devices or to specialized edge data centers close to population while highly power-intense training can be done in massive hyperscale data centers closer to renewable centers.

Transmission addresses this tradeoff directly. A robust interregional transmission network expands the geographic footprint within which data centers can site while still accessing cheap, renewable power. We can move power rather than data center locations and keep the internet backbone in place. An HVDC line from wind-rich Kansas to data center clusters in Dallas or Chicago does for AI infrastructure what the Changji-Guquan line does for Chinese industry: it decouples where energy is produced from where it is consumed.

There is also a resilience dimension. Data centers require extraordinarily high uptime, typically over 99.99% availability. A grid with strong interregional transmission connections is inherently more resilient to localized generation failures, extreme weather events, demand spikes, and inertia challenges. After Winter Storm Uri, the value of interconnection to ERCOT became painfully obvious to all but Texas legislators.

For AI companies making multi-billion-dollar infrastructure commitments with decade-long time horizons, grid resilience is not an abstraction. It has proven a core input to site selection. There is also risk that larger grids are susceptible to cascading failures, but this can largely be handled through improved power electronics and the benefits data centers bring through behind-the-meter power that could eventually connect to the grid. Sergio Toro, CEO of data center and energy data provider Aterio provided the following statement on tradeoffs of the behind-the-meter issue, “We’re seeing a growing number of data center developers turn to behind-the-meter power projects, particularly in less regulated markets like Texas. Operators know they will likely pay significantly more to generate their own power than they would through a traditional grid connection, but they can bring capacity online years earlier. Waiting five to seven years for an interconnection queue is an eternity in AI, where new models are released every few months and the major tech companies simply cannot afford to fall behind their competitors.”

China’s grid advantage thus has direct implications for AI competition. Chinese data centers benefit from a transmission network that can deliver bulk power over vast distances with two-year construction timelines. US data centers by contrast face interconnection queues measured in years, transmission constraints that limit where they can site, and a fragmented planning process that cannot coordinate the simultaneous buildout of generation and transmission that large-scale AI infrastructure requires. China will not “win” the AI race on grid infrastructure alone. Advantages in the space compound though, and cheaper energy provides one we would rather not divvy away.

There are many other inputs to AI development, and energy’s contributions are highly complex. But this does mean that the US is playing with an infrastructure handicap that will compound over time if left unaddressed. It would be quite ironic for the US to lose a strategic race on energy given its massive renewable and fossil energy resources and the original development of these industries in DOE labs. In the words of Otto Von Bismarck, “God has a special providence for fools, drunkards, and the United States of America.” However, even Bismarck would agree that luck cannot make up for consistency, planning, and design — even if it can allow us to find massive deposits of lithium in Oklahoma or keep the chinooks from going down over Caracas.

The parallels to the late 1990s telecommunications buildout are instructive, though imperfect. In the tech-bubble era, speculative overbuilding of fiber-optic networks created enormous excess capacity that ultimately enabled the internet economy. The buildout was chaotic, driven by irrational exuberance, and financially ruinous for many of the companies involved, but the infrastructure it left behind proved transformative.

Our special American providence may once again hold as America’s electricity infrastructure potentially undergoes a similarly rapid, if messy, expansion with tech firms contributing for energy expansion and AI creating political will. It may even be the case that AI fuels energy investments and then becomes remarkably efficient, leaving behind a better grid for the rest of us. The political economy is certainly different. Transmission lines cannot be laid by upstart companies the way fiber could. However, the underlying logic is the same: build the infrastructure first. Watch as infrastructure is paid for and demand collapses with the improved capital investments intact....

Does It Matter?

Does it matter? There’s a version of the argument that says no. The US doesn’t need to replicate China’s approach. Grid-enhancing technologies such as dynamic line ratings, advanced power flow controllers, and topology optimization can extract more capacity from existing infrastructure. Implementation of many new technologies has often been slow and overly focused on technical details rather than operations. Nonetheless, smarter grids are moving forward. Distributed energy resources and storage can reduce the need for long-distance transmission. Regional solutions may be sufficient.

The truth is the United States needs to do all of the above and also make massive investments in grid expansion. New energy and distributed resource technologies are complements to transmission, not substitutes for it. The physics of moving bulk power across thousands of miles have not changed. Every serious modeling exercise that looks at deep decarbonization, massive electrification, and new demand from data centers and AI reaches the same conclusion: the US needs dramatically more interregional transmission capacity. Further, any politically palatable shift to renewable energy will need to come alongside plentiful good jobs to replace fossil fuel construction work. Transmission will be a massive source of fiscal investment and job creation.

The deeper concern is strategic. China’s grid buildout has created a vertically integrated industrial ecosystem from mining to manufacturing to deployment in power electronics and HVDC systems. This gives China not just cheaper domestic infrastructure but export capabilities. The robustness of the Chinese grid also makes it significantly more resilient to faults and cascading failures.

SGCC has already built UHVDC lines in Brazil, invested in grid assets in the Philippines, Australia, and Portugal, and positioned UHVDC as a key technology for the Belt and Road Initiative. The US, by contrast, is a technology consumer in this space, dependent on a thin base of domestic capability supplemented by European and increasingly Chinese suppliers.

Can the US grid modernize fast enough to support electrification, integrate renewables, maintain reliability, and avoid falling further behind on industrial capability in power electronics? That’s the important question. And the solution will not come from replicating China’s centralized model. Rather, the key will be finding an institutional architecture that can achieve scale, speed, and coordination through means compatible with grid decentralization and American governance. A good blueprint for Federal action can be found in the proposed Big Wires Act introduced by Senator Hickenlooper (D-CO) and Representative Peters (D-CA) with the below proposed interregional grid expansions:

{kind=link}

That architecture for massive grid buildout and major investments in interregional transmission doesn’t exist yet. Building it may be the most important engineering infrastructure challenge of the next decade. It may be a significantly harder challenge, though, to muster the political will for grid expansion. Xi Jinping certainly does not have such problems.

The value of democracy and capitalism is that, in the long run, they make the best decisions on average. In the short-run, it may be of use to defenestrate the head of a top ISO for poor grid performance or arrest the head of Constellation for corrupting the youth by extracting excessively high profits. However, in the long run, this hollows out experience bases and leads to poorer decisions on average. For this particular problem, it may behoove us to get to those long-run average best decisions a little faster and with a lower variance.

Outstanding work... very much enjoyed reading your essay

Whatever I had planned to do this morning was delayed as I worked my way through this remarkable post. Incredibly helpful.

How does the U.S. education system factor into the current challenges (and future opportunities)? You mention how many expert engineers and academics (professors/grad students) China dedicated to the UHVDC build-out. Are we in good shape here, or is this another looming problem?